Key Highlights

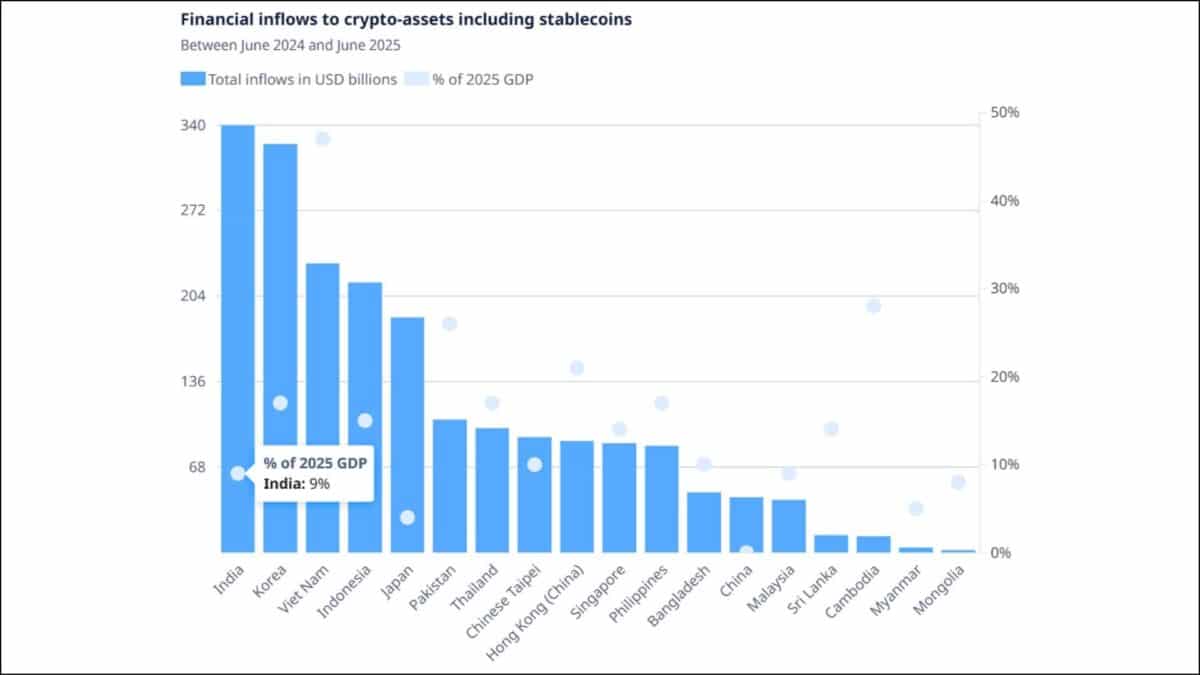

- OECD says India’s crypto activity reached nearly $340 billion in one year, equivalent to 9% of GDP, making it Asia’s largest crypto market by inflows.

- Despite a 30% crypto tax and 1% TDS, India still lacks a dedicated crypto law, while around 90% of VDA trading now takes place on offshore platforms.

- The report highlights major regulatory shifts ahead, including CARF reporting from April 2027, alongside growing stablecoin adoption, rising cybercrime risks, and Asia’s 69% crypto market growth.

The Organisation for Economic Co-operation and Development (OECD) released its Asia Capital Markets Report 2026 in June 2026, and the findings on crypto are hard to ignore. Among the most striking data points is the revelation that India’s crypto-asset transaction value over 12 months has reached the equivalent of approximately 9% of its gross domestic product (GDP).

For a country where crypto-assets are still not formally regulated by any dedicated legislation, that number carries significant weight. India’s nominal GDP stood at approximately $4.15 trillion in 2025, according to the International Monetary Fund (IMF).

A 9% share translates to approximately $340 billion in crypto-asset inflows over a single 12-month period, according to the OECD’s data sourced from Chainalysis.

However, context matters when reading that number. Sudhakar Lakshmanaraja, Founder at Digital South Trust, notes that Chainalysis “inflows” measure crypto received by blockchain addresses geolocated to India, including buying, trading, payments, wallet transfers, and DeFi activity. This reflects crypto activity volume attributed to Indian users, not balance of payments or cross-border capital flows.

As Lakshmanaraja explains, “it does not prove that rupees left India or foreign money entered India,” as much of the activity could simply be domestic, such as an Indian user buying crypto and moving it to a personal wallet. He adds that India needs clear crypto regulation aligned with the Foreign Exchange Management Act (FEMA), the Liberalised Remittance Scheme (LRS), taxation, investor protection, exchange accountability, custody, DeFi, cybercrime, and systemic risk safeguards, consistent with its role in G20, FATF, and OECD/G20 Inclusive Framework discussions.

This article breaks down every relevant finding from the report, starting with India and then expanding to the broader Asian crypto landscape, to help readers understand what the OECD is actually saying and what it means for Indian crypto users, traders, and policymakers.

India: The largest crypto market in Asia by absolute inflows

The OECD report draws on data from Chainalysis, the blockchain analytics firm, to measure blockchain-based crypto-asset inflows across jurisdictions. According to the report, India and Korea recorded the largest crypto inflows in all of Asia in absolute dollar terms during the 12 months ending June 2025.

India’s position at the top is not a surprise for those tracking the market closely. The Chainalysis 2025 Global Crypto Adoption Index ranked India first globally for crypto adoption, ahead of the United States, for the third consecutive year. But the OECD’s framing puts this in a macroeconomic context that adoption indices alone do not capture.

When the total value of crypto-asset transactions is measured against the size of the economy, 9% of GDP is a figure that places crypto firmly within the scope of macroeconomic policy discussions.

For comparison, India’s entire corporate bond market stands at just 3.4% of GDP, according to the same OECD report. In other words, the value flowing through crypto channels now significantly exceeds the size of India’s formal corporate debt market.

India ranks among top 5 crypto-adopting nations driving Asia’s growth

The OECD identifies five countries as the primary drivers behind Asia’s explosive crypto growth: India, Indonesia, Vietnam, the Philippines, and Pakistan. All five feature among the top 10 crypto-adopting nations globally, according to Chainalysis data cited in the report.

The common factors the OECD highlights across these markets include high internet penetration rates, large young and tech-savvy populations, and growing demand for digital financial services. India checks every one of those boxes, with over 750 million internet users and a median age of 28.

Industry estimates peg the Indian crypto user base at approximately 107 million, making it one of the largest in the world by sheer participant count.

No formal crypto regulation despite leading adoption

Perhaps the most consequential observation the OECD makes about India is a regulatory one. The report explicitly states that crypto-assets in India are “currently not formally regulated” and that the government has only “taken measures to address risks while signalling a restrictive stance.”

This is a significant statement coming from a 38-nation intergovernmental policy body.

India is the largest crypto market in Asia by absolute inflows, one of the top five adoption markets globally, yet it operates without a dedicated crypto regulatory framework. No comprehensive crypto legislation has been introduced in Parliament as of June 2026.

What India does have is a tax regime. Since 2022, the government has imposed a flat 30% tax on all crypto gains with no provision for loss set-off or carry-forward, along with a 1% tax deducted at source (TDS) on every transaction.

Budget 2026 further tightened compliance by introducing daily penalties of Rs 200 for late reporting and Rs 50,000 for incorrect filings, effective April 1, 2026.

The OECD report also notes that the Financial Action Task Force (FATF) classifies India as only “partially compliant” with Recommendation 15, which deals with the regulation of virtual asset service providers (VASPs). Only Singapore in Asia has achieved full compliance, while India sits alongside Mongolia, Bangladesh, Pakistan, and Sri Lanka in the partially compliant category.

The 90% offshore problem and CARF deadline

The tax framework has had a measurable effect on trading patterns. According to data presented to the Indian Parliament in May 2026, approximately 90% of India’s virtual digital asset (VDA) trading volume now takes place on offshore platforms, beyond the immediate reach of domestic regulators.

This offshore migration is set to collide with a global transparency mechanism. India has committed to implementing the OECD’s Crypto-Asset Reporting Framework (CARF) by April 1, 2027.

Under CARF, crypto-asset service providers in over 50 participating jurisdictions will be required to automatically report Indian users’ transaction data, including crypto-to-fiat conversions, crypto-to-crypto trades, wallet transfers, and high-value payments above $50,000, to Indian tax authorities.

As The Crypto Times reported in May 2026, the Reserve Bank of India (RBI) is building a complementary domestic reporting infrastructure. The central bank mandated Unique Transaction Identifiers (UTIs) for all over-the-counter (OTC) derivative transactions effective April 2026, and the data from CARF and domestic trade repositories will eventually sit side by side, giving regulators a composite view of how money moves between the banking system, the derivatives market, and the crypto ecosystem.

Stablecoins and capital controls: The US dollar exposure question

The OECD report raises a broader concern that is directly relevant to India: the use of stablecoins to gain synthetic dollar exposure outside traditional banking channels. The report notes that stablecoin use cases are “emerging in remittances and currency exchange, especially in jurisdictions with tighter capital controls.”

India fits that description precisely. Under the Liberalised Remittance Scheme (LRS), Indian residents can remit up to $250,000 per financial year. But purchasing Tether (USDT) or USD Coin (USDC) with rupees through peer-to-peer (P2P) platforms effectively converts rupees into dollar-denominated exposure without triggering LRS reporting.

A March 2026 working paper co-authored by the Bank for International Settlements (BIS) and the IMF confirmed that stablecoin-based dollar exposure shows larger “parity deviations” compared to traditional forex in economies with capital controls.

The Crypto Times detailed this dynamic in its analysis of the 7% premium that Indian buyers pay for USDC compared to the real USD exchange rate.

The global stablecoin market now sits at approximately $320 billion, with 98% denominated in US dollars. The top five stablecoins alone reached nearly $300 billion in market capitalization as of March 2026, growing 48% in a single year, according to the OECD report.

Asia’s crypto landscape: 69% growth, the fastest in the world

Moving beyond India, the OECD report maps a broader transformation across the Asian crypto landscape. The region recorded a 69% year-on-year growth rate in blockchain-based crypto-asset transactions between June 2024 and June 2025, the highest growth rate among all global regions.

Asia now accounts for a substantial share of global crypto activity. The region’s total crypto transaction volume in the Asia-Pacific grew from $1.4 trillion to $2.36 trillion over this period, according to Chainalysis data referenced in the report.

Vietnam: Crypto inflows worth 55% of GDP

While India leads in absolute inflow volume, Vietnam holds the record for crypto penetration relative to its economy. The OECD report states that Vietnam recorded crypto-asset inflows equivalent to 55% of its GDP in the same 12-month period.

Several structural factors explain this. Vietnam has high internet penetration at 84%, relatively limited domestic investment alternatives, and a population that has long relied on digital channels and foreign currencies for transactions. Vietnam formally legalized crypto-assets when its Digital Technology Industry Law took effect on January 1, 2026, becoming the 46th country worldwide to do so.

The OECD also notes that stablecoins, particularly USDT, have become a functional replacement for traditional remittance channels across the Association of Southeast Asian Nations (ASEAN), reducing transfer costs in high-cost corridors connecting Vietnam, the Philippines, and Indonesia.

Pakistan and Cambodia: Crypto filling gaps left by banks

The report identifies another interesting pattern among Asian markets. In Pakistan and Cambodia, the OECD explicitly connects crypto adoption to “reliance on foreign currencies, digital channels for remittances, and limitations in conventional financial systems.”

In both countries, outstanding non-financial corporate bonds account for close to 0% of GDP, indicating a near-total absence of formal capital market financing for businesses. In this context, crypto is not primarily a speculative instrument. It functions as a workaround for populations that traditional banking infrastructure does not adequately serve.

Pakistan and Indonesia also feature among the top 10 crypto-adopting countries globally, driven by young populations and rapidly expanding mobile internet access.

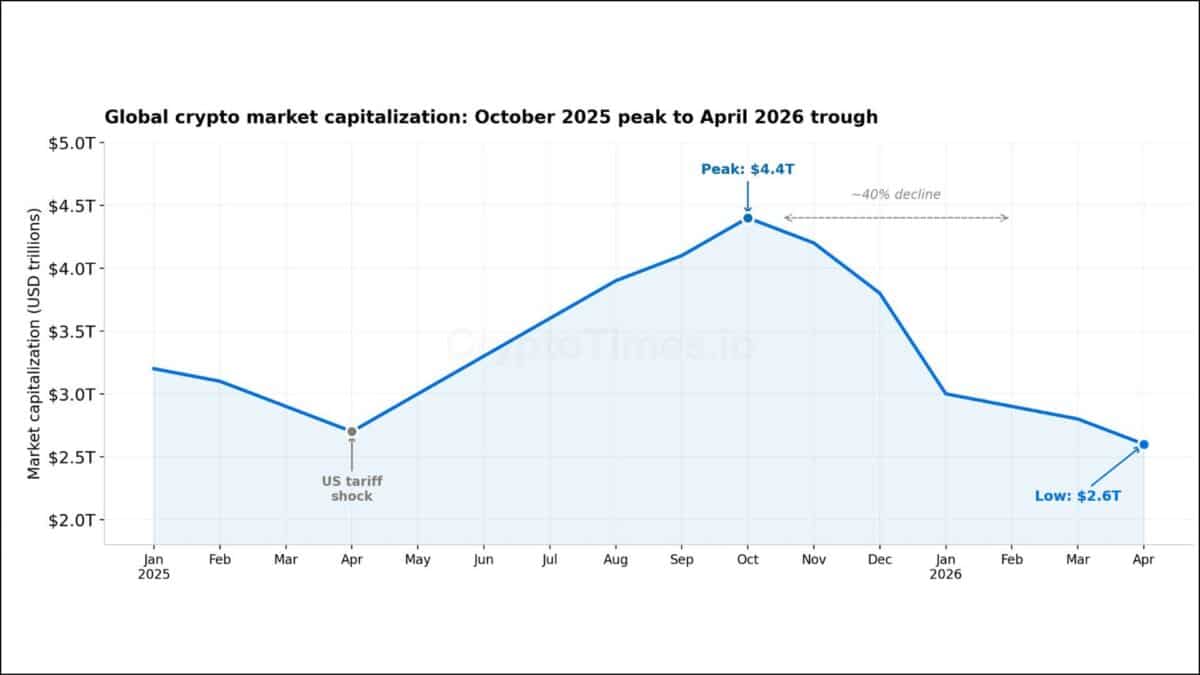

The $4.4 trillion to $2.6 trillion crash

The OECD report provides a useful timeline of global crypto market movements. Total crypto market capitalization peaked at $4.4 trillion in October 2025, then gradually declined through the end of 2025 to reach $3 trillion at the start of 2026. By April 2026, it had dropped further to $2.6 trillion, a decline of approximately 40% from the peak.

The report attributes this decline to a combination of tighter monetary conditions, tariff-related uncertainty following US trade policy announcements in April 2025, and rising geopolitical tensions in the Middle East in early 2026. Asian equity markets experienced parallel volatility during this period, with several economies, including India, seeing net foreign capital withdrawals between January and April 2025.

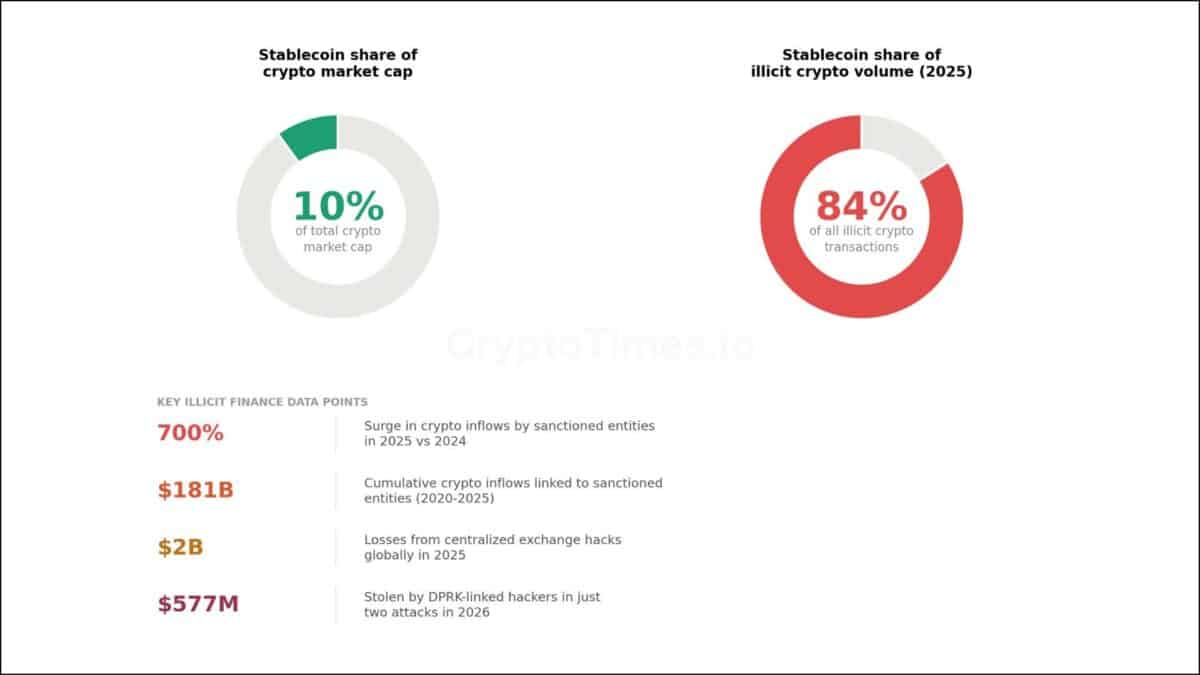

Stablecoins: 10% of market cap, 84% of illicit flows

One of the most significant sections of the OECD report deals with the dual nature of stablecoins: their growing legitimate utility, and their dominance in illicit financial activity.

Stablecoins represent only about 10% of the overall crypto market capitalization, but their functional importance far exceeds that share. They are increasingly being used for trading, lending, borrowing, liquidity provision in decentralized finance (DeFi), cross-border remittances, and currency exchange.

Sanctions evasion surged 700% in 2025

On the illicit side, the numbers are alarmingly stark. The OECD report, citing data from Chainalysis, states that financial inflows into crypto-assets by sanctioned entities and jurisdictions surged nearly 700% in 2025 compared to 2024. Between 2020 and 2025, the cumulative value of crypto inflows linked to sanctioned entities is estimated at $181 billion.

Stablecoins accounted for 84% of all illicit crypto-asset financing in 2025. The OECD specifically notes that some sanctioned financial entities have gone beyond merely using existing stablecoins. They have “issued stablecoins to evade sanctions and make cross-border payments that circumvent traditional payment rails.”

The Chainalysis 2026 Crypto Crime Report identified Russia’s ruble-backed A7A5 stablecoin as a prominent example. It processed $93.3 billion in transactions within less than a year, functioning as a dedicated settlement system for sanctioned Russian businesses and entities.

North Korea’s crypto theft operation

Exchange security is another risk the OECD highlights specifically for Asia. In 2025, centralized exchanges globally faced losses of approximately $2 billion from hacking attacks, while decentralized exchanges lost $424 million. The most prominent attack was the February 2025 ByBit hack, attributed to actors linked to the Democratic People’s Republic of Korea (DPRK).

In 2026, DPRK-linked hackers escalated further. Just two attacks resulted in the theft of $577 million, representing more than three-quarters of total hacking losses for the year to date. The OECD report notes a specific operational pattern: stolen crypto-assets are converted into stablecoins across multiple blockchain networks to launder the funds before converting to fiat currency.

This operational detail matters for Indian users on global exchanges. The Crypto Times reported on the US Treasury’s coordinated sanctions against Southeast Asian scam networks in June 2026, a development that reinforces the OECD’s warning about growing interconnectedness between crypto crime and traditional financial systems.

Malaysia’s $1 billion crypto mining power theft

Tucked inside the OECD report is also that a national utility company in Malaysia reported losses of $1 billion between 2020 and August 2025, linked to illegal electricity usage by crypto-asset miners. Nearly 14,000 suspected illegal mining sites were identified across the country.

The OECD flags this as part of a broader category of illicit finance risks associated with unauthorized crypto mining. These operations carry both economic costs, through stolen electricity and infrastructure strain, and environmental costs, depending on the consensus mechanism used by the mined crypto-asset.

This is a data point that puts a tangible economic cost on the physical footprint of crypto activity in Asia, moving the discussion beyond price charts and regulatory debates into infrastructure-level impact.

Regulatory fragmentation across Asia

The OECD report maps a wide spectrum of regulatory approaches across Asian jurisdictions, and the variation is significant.

China continues to maintain a complete ban on crypto trading and related activities. A February 2026 notice reiterating this stance confirmed that the country’s restrictive position remains unchanged.

Japan is moving in the opposite direction. The country is expected to cut crypto taxes from 55% to 20% in 2026, aligning crypto taxation with traditional capital gains rates, as per a report by TRM Labs.

The Japan Financial Services Agency (JFSA) has been actively licensing stablecoin issuers, including approving Ripple’s RLUSD stablecoin for distribution via SBI VC Trade in June 2026.

Singapore remains the only Asian jurisdiction with full FATF compliance on virtual asset regulation. Hong Kong has expanded its licensing framework for virtual asset platforms and is developing a stablecoin licensing regime.

India sits in between. There is no comprehensive legislation, no dedicated regulator, and no clear timeline for either. The Securities and Exchange Board of India (SEBI) has proposed a multi-regulator model where it would oversee exchanges and security-like tokens, while the RBI handles cross-border flows.

But the RBI has historically opposed legitimizing the sector, and a policy discussion paper expected in early 2026 was reportedly blocked by the central bank.

What this means for Indian crypto users

For Indian users, the OECD report crystallizes several realities that will shape the market over the next 12 to 18 months.

First, the scale of Indian crypto activity is now large enough to attract serious policy attention from international bodies. A 9% GDP equivalent is not a fringe market. It is a macroeconomic variable.

Second, the CARF deadline of April 2027 is approaching. Offshore wallets, exchange accounts on foreign platforms, and cross-border stablecoin transfers will become visible to Indian tax authorities through automated data sharing. The window of practical anonymity for offshore trading is narrowing.

Third, the global regulatory direction is toward integration, not isolation. Japan is cutting taxes. Singapore is building institutional infrastructure. Vietnam has legalized crypto. India’s current approach of high taxes, no regulation, and partial FATF compliance risks pushing more activity offshore, exactly the outcome the government says it wants to prevent.

The OECD report does not prescribe policy for India. But the data it presents, $340 billion-plus in annual crypto transaction value, the largest absolute inflows in Asia, 90% offshore trading, partial FATF compliance, and no formal regulation, paints a picture that is increasingly difficult for policymakers to leave unaddressed.

Also Read: India’s Parliament Finance Committee to Hear RBI & ICAI on VDAs on July 2