Sit down. Pour yourself something. And keep it legal, none of that pending FDA approvals. Because what happened on Friday morning is the most honest thing anyone in this entire CLARITY Act circus has done in eighteen months, and almost nobody caught it.

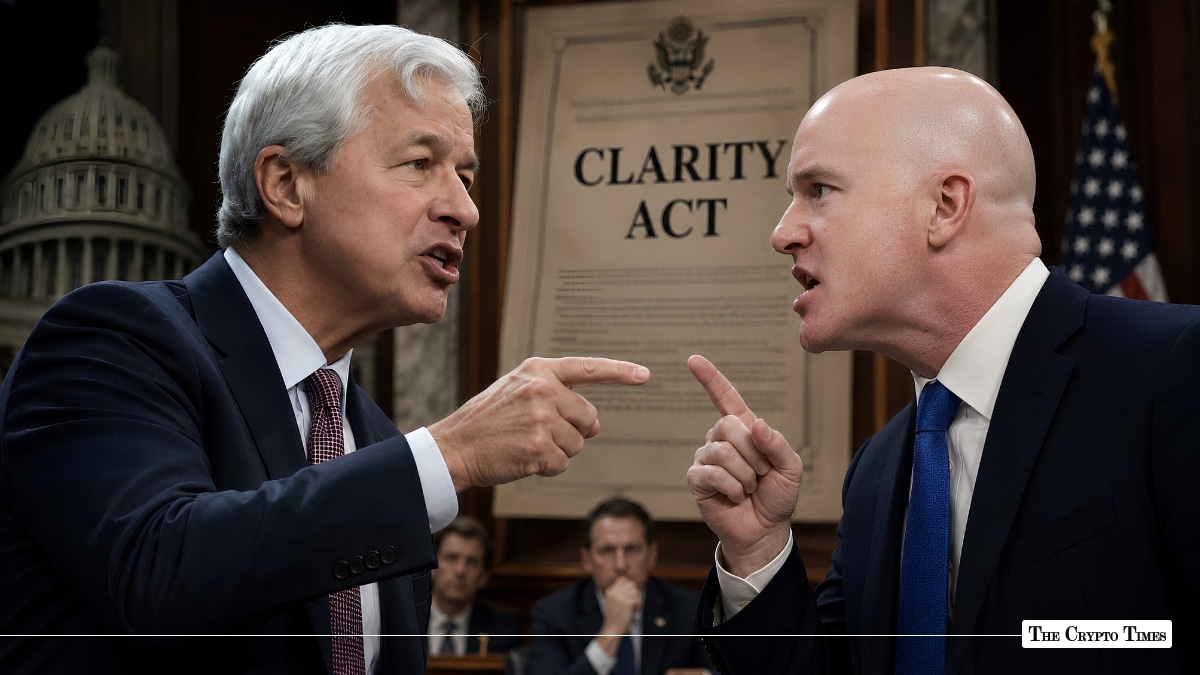

Jamie Dimon — the chairman, the CEO, the last of the Wall Street kings, the guy who runs the biggest bank this country has ever built — sat down on Maria Bartiromo’s couch on a Friday in late May and did two things in the same conversation.

First, he said he wasn’t worried.

Then he declared war.

And if you can hold both of those in your head at the same time — I’m not worried and we will fight this to the death — then congratulations, you finally understand what the CLARITY Act has actually been about this whole time. It was never about clarity. We said that in January, we said it in April, and it’s still true today. It was always about who gets to skim the float when America’s money stops moving.

On Friday, the man with the most float to skim stopped pretending otherwise.

The Couch, The Quote, The Tell

Let me paint you the scene, because the scene matters.

It’s Friday, May 29. “Mornings with Maria.” Dimon’s on Fox Business, and the conversation turns to the CLARITY Act — the crypto market-structure bill that, just two weeks earlier, cleared the Senate Banking Committee on a 15-9 vote and started its march toward the Senate floor. Thirteen Republicans, two Democrats, a bill that four months ago looked dead in the water. Momentum. Real momentum.

And Maria asks Jamie the question. Are you good with this thing?

And Dimon — God love him, because at least he doesn’t lie to your face the way the politicians do — Dimon says no. He says the bill lets crypto companies effectively pay interest on deposits, stablecoins or something like that, without the protection that they should have. And then he lands it. “So, no, the banks will not accept it that way,” he says.

The banks will not accept it.

Not “we have concerns.” Not “we’d like to see amendments.” The banks will not accept it. That’s not a comment. That’s a threat with a tie on.

And then Maria pushes — what about the progress, Jamie, the thing already passed committee — and Dimon doesn’t blink. “We’ll fight it. If we lose, we lose, and we’ll live,” he says.

We’ll fight it. If we lose, we lose, and we’ll live.

You hear that? That’s a man telling you he’s going to war and he’s already pre-grieved the possibility of losing. That’s not a guy who’s relaxed about an industry. That’s a guy who’s done the math, doesn’t love the answer, and is going to swing anyway.

But here’s the part nobody clipped for the highlight reel. Somewhere in that same interview, asked about stablecoins directly, Dimon said he was “not that worried” about them. He pointed out JPMorgan already has its own deposit coins. Cross-border payments, small-dollar transfers, person-to-person — sure, useful, fine, whatever.

Not worried.

Not worried about the thing he just promised to fight to the last man.

Folks, that is the tell. That is the entire poker game in one sentence. When the guy across the table tells you he’s holding nothing and then shoves all his chips in, you don’t believe the words. You believe the chips. And Jamie Dimon just shoved every chip he had into a pot for a hand he claims doesn’t scare him.

So which is it, Jamie? Because it can’t be both.

“Full Of Sh-t” — A Love Story

Now. Let’s talk about the part everyone did clip.

Because in the middle of all this, Dimon went after Brian Armstrong personally. He brought up the hundreds of millions Coinbase and the crypto industry have poured into Washington — and then, on live television, the CEO of America’s largest bank looked into the camera and called the CEO of America’s largest crypto exchange “full of sh-t.” “No one is going to bow down to this guy,” he added, for flavor.

And if that line sounds familiar, it should. Because this isn’t the first time Jamie said it. Back in January, at Davos — the ski-resort summit where billionaires go to network and pretend it’s work — Dimon ran into Armstrong and reportedly told him, to his face, “You are full of s—.”

Same insult. Same target. Five months apart. One whispered in the Alps, one broadcast to the world.

That’s not a guy who lost his temper. That’s a guy with a theme.

And look — I’m not here to defend Brian Armstrong. We’ve spent four pieces in this series watching Armstrong play both sides of this thing like a concert pianist. He’s the guy who pulled support for this bill in January the night before the markup, tanked the whole thing, sat on his hands for four months, and then posted two words — “Mark it up” the second the language went his way. Armstrong didn’t get religion. Armstrong got the compromise he wanted and called it a “true compromise” because that’s what you call the deal when you won.

So no, this isn’t the good guys versus the bad guys. There are no good guys. There’s a casino, and there are two men fighting over who runs the cage.

But here’s why Dimon keeps saying it. Here’s why “full of sh-t” is the only weapon he’s got. Because Dimon can’t win the argument on the merits in a room full of crypto bros, so he wins it the only way a king wins it — by refusing to acknowledge the other guy is a peer. No one is going to bow down to this guy. Translation: I am the institution, and you are a man with an app. That’s the energy. That’s the whole posture. It’s not regulation. It’s status.

What He’s Actually Selling You

Okay, let’s be fair to Jamie for a second, because the man does have a real argument buried under all the insults, and it’s worth pulling out into the light.

Dimon’s pitch is “fair and equal.” It goes like this: I have to build branches in low-income neighborhoods. I have capital requirements. I have liquidity requirements. I have — and this is a real number he likes to throw around — something like 84 regulators all over us. AML. Bank Secrecy Act. KYC. The whole alphabet. If Coinbase wants to pay you a yield on a dollar token that sits in your account and feels exactly like a savings account, then Coinbase should carry the same anchor I carry. Otherwise I’m running a marathon in lead boots while the other guy’s in track spikes.

And here’s the uncomfortable thing: he’s not wrong about the mechanics. He’s just wildly self-interested about why he cares.

Because the actual fear — the thing under the thing — is deposit flight. U.S. banks fund roughly 80% of their lending with your deposits. That’s the float. That’s the engine. You park your money, they pay you basically nothing, they lend it out at a fat spread, and the difference is the empire. Now imagine a stablecoin that pays you three-and-a-half percent to hold it. One study — and the banks know this number cold — warned that as much as half a trillion dollars in deposits could walk out of the banking system and into stablecoins by 2028.

Half a trillion dollars.

That’s the thing Dimon is “not worried” about. Half a trillion dollars in float, draining out of the cage, into a product he doesn’t control. And he sat there on Friday morning and told America he’s relaxed about it.

Sure he is. He’s so relaxed he’s going to war.

The Tillis-Alsobrooks Hand-Job (The Polite Kind)

Now here’s where it gets good, because the bill the banks “will not accept” was already written to give them almost everything they asked for.

The compromise — the Tillis-Alsobrooks language that broke the four-month logjam — does the thing Dimon claims to want. It bans the passive stuff. You can’t just hold a stablecoin and collect interest that’s the “economic or functional equivalent” of a bank deposit. That’s prohibited. Dead. Gone.

What it allows is rewards tied to actual activity — transactions, real participation on the platform. They shifted the model from “buy and hold” to “buy and use.” It’s a threading-the-needle deal. The senators who wrote it spent months on it. Armstrong signed off. Circle signed off.

And the banks looked at the needle that had been threaded specifically to accommodate them and said: not good enough. Five major banking trade groups came out swinging the week before the markup. And now Dimon, the heaviest hitter of them all, goes on television and says the banks won’t accept it.

You want to know why? Because “fair and equal” was never the actual ask. “Fair and equal” is the press-release version. The real ask is no yield, ever, in any form, full stop — because every dollar of yield a stablecoin pays is a dollar of float that doesn’t sit in a bank for free. The activity-based carve-out is still a door. And Dimon doesn’t want a door. He wants a wall.

That’s why a compromise built to satisfy the banks didn’t satisfy the banks. You can’t compromise with a guy whose actual position is “you shouldn’t exist.”

So Who’s Bluffing?

Here’s where I land, and you can tell me I’m wrong in the comments.

I don’t think Jamie Dimon is going to kill this bill. I think Jamie Dimon knows he’s probably going to lose this one — that’s the whole “if we lose, we lose, and we’ll live” energy. That’s a man managing expectations downward in public. That’s pre-grief.

But I don’t think that’s the point of Friday.

The point of Friday was the record. The point was for the most respected banker in America to stand up, on the most-watched business channel in the country, and put it on the permanent record that the banks fought this. He told you the bill doesn’t go far enough on AML, on the Bank Secrecy Act, on the consumer protections that are supposed to sit underneath anything that smells like a deposit. He told you it would, in his words, “eventually blow up.” And he said all of it on tape.

That’s not an argument. That’s an insurance policy.

Because here’s what Jamie Dimon is really building on that couch. He’s building the “I told you so.” He is positioning himself, right now, in May 2026, to be the first man at the microphone the day this thing goes wrong. And in a market this young, with a product this new, something always eventually goes wrong — a stablecoin wobbles, a platform freezes withdrawals, a few hundred thousand regular people find out the hard way that “rewards” came with no FDIC sticker on the back. When that day comes — and it’s a when, not an if, in any market that runs hot enough — Dimon doesn’t have to scramble. He’s already on the record. He gets to walk to the nearest camera and say: I warned you. I went live on camera in May and I told you this bill didn’t protect anybody. You didn’t listen. Now look.

That’s the genius of Friday, and it’s also the cynicism of it. He’s not just fighting the bill. He’s pre-writing the post-mortem. He wants to be the guy holding the receipt when the bill it’s printed on goes up in smoke.

He’s not playing to win the vote. He’s playing for the eulogy. And he’s making sure his name is on it.

And the “not worried” line? That’s the part that gives him away. A man who’s actually not worried doesn’t show up. He doesn’t curse out a competitor on television twice in five months. He doesn’t promise a war. The performance of being relaxed is the most stressed thing a powerful man can do, because the genuinely relaxed don’t perform at all.

Jamie Dimon is worried. He’s worried about the float. He’s been worried about the float since the day a dollar token started paying better than a savings account. The whole CLARITY Act fight, from Armstrong’s January walkout to Friday’s couch, has been one long argument about the float and who gets to skim it.

It was never about clarity.

It was always about who gets to skim the float when America’s money stops moving.

And on Friday, for about ninety seconds on live TV, the king said the quiet part out loud — and then told you he wasn’t worried about a single word of it.

Don’t believe the words. Believe the chips.