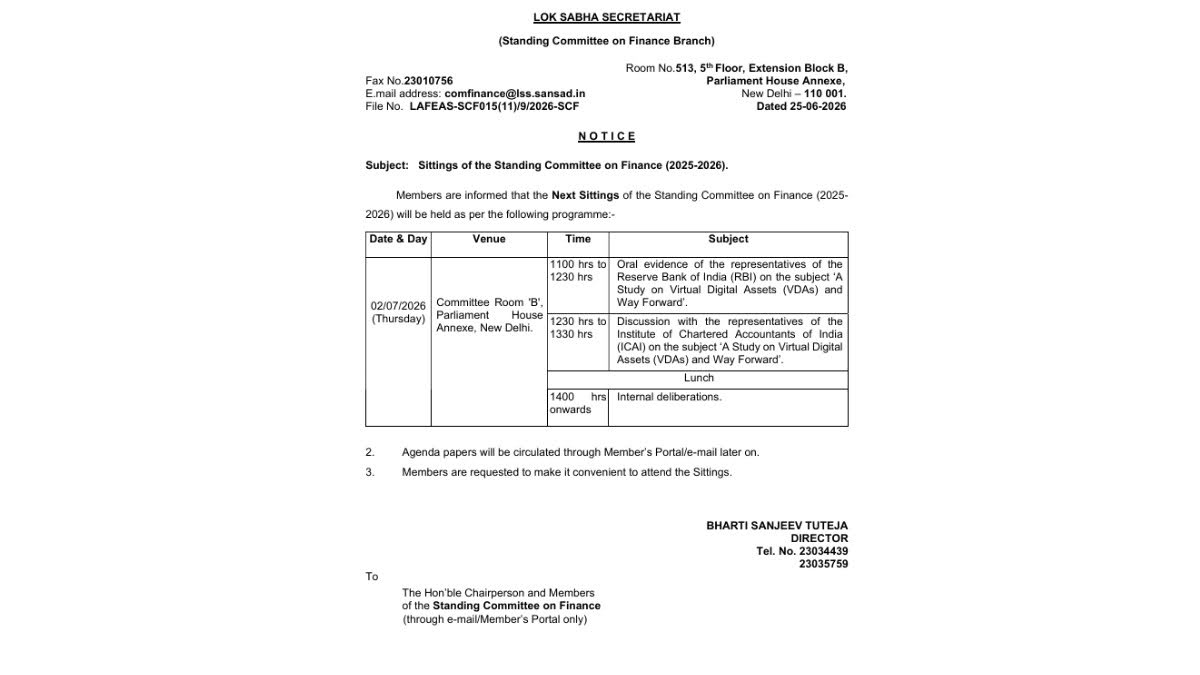

India’s Parliamentary Standing Committee on Finance, chaired by BJP MP Bhartruhari Mahtab, has called representatives of the Reserve Bank of India (RBI) and the Institute of Chartered Accountants of India (ICAI) to appear before it on July 2, 2026, for discussions on the subject “A Study on Virtual Digital Assets (VDAs) and Way Forward.”

A formal notice dated June 25, 2026, issued by Director Bharti Sanjeev Tuteja of the Lok Sabha Secretariat’s Standing Committee on Finance Branch, lays out the day’s programme. The RBI is scheduled to give oral evidence from 11:00 AM to 12:30 PM in Committee Room ‘B’ at Parliament House Annexe, New Delhi.

The ICAI will follow from 12:30 PM to 1:30 PM for a discussion session on the same subject. Internal deliberations among committee members are scheduled for the afternoon, beginning at 2:00 PM after a lunch break.

Why this sitting matters

This marks a significant escalation in Parliament’s ongoing examination of the crypto question. Over the course of seven previous sittings stretching back to late 2025, the committee has heard from crypto exchanges, industry associations, the Financial Intelligence Unit (FIU-IND), the Central Board of Direct Taxes (CBDT), the Revenue Secretary, the Ministry of Corporate Affairs, IFSCA, and platforms including Binance, WazirX, ZebPay, CoinDCX, CoinSwitch, and Coinbase.

But until now, the RBI itself has not appeared before the panel on this subject. And the central bank’s position on virtual digital assets is well established. Committee Chairman Mahtab himself acknowledged it publicly after the panel’s 7th sitting on May 20, telling PTI: the RBI is opposed to any regulation or any permission for VDAs being operated in India.

The central bank has held that line since it first warned the public about virtual currencies in December 2013, and then went further with a banking ban on crypto businesses in April 2018, a ban the Supreme Court struck down in 2020.

Calling the RBI for direct oral evidence before the committee suggests that lawmakers now want the central bank’s objections, concerns, and recommendations entered formally into the record before the panel moves towards drafting its report.

The inclusion of ICAI is equally notable. As the statutory body governing the accounting profession in India, the ICAI’s views on audit standards, disclosure norms, and accounting treatment for digital assets could feed directly into whatever compliance and reporting framework emerges from the committee’s final recommendations.

What may have prompted the timing

The formal agenda for the July 2 sitting does not specify the exact lines of questioning the committee intends to pursue with either the RBI or the ICAI. But the timing invites informed speculation.

On June 17, the Enforcement Directorate’s Bengaluru Zonal Unit conducted searches at six premises linked to cryptocurrency payment and remittance service providers under Section 37 of the Foreign Exchange Management Act (FEMA).

The ED alleged that it had uncovered more than Rs 2,500 crore in unauthorised cross-border money transfers facilitated through virtual digital assets and froze approximately Rs 6 crore in linked bank accounts.

The entities named in the probe include Transak Technology India, Carretx Technologies, Mokshagna Technologies, Buyhatke Internet (operating as Onramp.money), and Abhibha Technologies (operating as Onmeta).

According to the ED, these firms offered on-ramp and off-ramp services that allowed users to convert fiat currency into crypto and back, effectively facilitating cross-border fund movement through digital assets without the authorisation required under India’s foreign exchange regulations.

The ED stated that several of these platforms openly advertised international remittance services through crypto despite lacking RBI approval.

This kind of enforcement action exposes a regulatory gap that the committee may well want to question the RBI about. FIU-IND registration covers anti-money laundering compliance.

But it does not address Liberalised Remittance Scheme (LRS) requirements, FEMA compliance, capital controls, stablecoin regulation, or the broader question of how crypto-enabled cross-border payment flows fit within India’s foreign exchange framework. Those questions fall squarely within the RBI’s domain.

It is plausible, though not confirmed, that the ED’s findings have added urgency to the committee’s decision to hear from the central bank directly. When FIU-registered or crypto-linked firms can enable large rupee-to-USDT conversions and cross-border flows without clear RBI permission, the regulatory conversation moves well beyond taxation and KYC into territory that only the RBI can address with authority.

The road so far

The committee’s study on VDAs, formally titled “A Study on Virtual Digital Assets (VDAs) and Way Forward,” was taken up as a subject for detailed examination during the 2024-25 period, listed as Item No. 3141 in the Lok Sabha Bulletin Part II published on August 14, 2025.

The journey since then has been methodical. In December 2025, the panel heard from domestic exchanges including CoinDCX, Coinbase, and CoinSwitch. On January 7, 2026, representatives of FIU-IND and the CBDT appeared before the committee. The CBDT informed the panel during that sitting that approximately Rs 888.82 crore in undisclosed income related to VDA transactions had been identified and notices had been sent to over 44,000 taxpayers.

The 7th sitting, held on May 20, 2026, brought Binance, WazirX, and ZebPay to Parliament House alongside the Revenue Secretary, representatives of the Income Tax Department, IFSCA, and the Secretary of Corporate Affairs.

It was after this session that Mahtab made his most detailed public comments on the subject, noting that thousands of crores were flowing out of the country through crypto investments and describing the situation as “very alarming.”

He also outlined three categories of global approaches: countries that regulate crypto (the US, the UK, the EU), countries that ban it outright (China), and countries that attempt to govern it through existing laws rather than dedicated legislation (Japan, Brazil). India, he said, was studying all three before deciding its own course.

Government officials at the same sitting classified the VDA ecosystem as “high risk,” flagging connections to money laundering, cyber fraud, terror financing, narcotics trafficking, human trafficking, Ponzi schemes, and illegal cross-border fund movement.

The RBI factor

The Reserve Bank of India’s position on crypto is the single most consequential variable in this entire policy discussion. A crypto regulation discussion paper, reportedly in its final drafting stages as of May 2025 under a working group led by the Department of Economic Affairs, was shelved again by April 2026.

Reporting attributed the delay primarily to the RBI’s persistent opposition. The central bank has consistently argued that legitimising crypto through regulation could allow the sector to become systemic, posing risks to financial stability.

At the same time, the RBI has been pushing its own alternative. The Digital Rupee, India’s central bank digital currency, has crossed 150 million transactions in volume with total value exceeding Rs 34,000 crore.

The RBI has also submitted a proposal to place the linking of CBDCs across BRICS economies on the agenda for the 2026 summit, positioning the e-rupee as a tool for reducing dependence on the US dollar in cross-border trade.

A proposed multi-regulator model currently under discussion would split oversight between three agencies: SEBI for crypto exchanges and security-like tokens, the RBI for cross-border crypto flows and foreign investment links, and the Finance Ministry for policy and taxation. But none of this has been formally adopted.

India still does not have a comprehensive law governing VDAs, no clarity on which single regulator oversees crypto, and no legal definition of whether crypto is a commodity, a security, or a currency.

What the RBI tells the committee on July 2, behind closed doors, could go a long way toward determining whether India moves toward a regulated framework, continues with the current tax-but-don’t-regulate approach, or charts an altogether different path.

What comes next

Industry observers have noted that this sitting could be among the final sessions on the VDA subject before the committee begins drafting its report to Parliament. If that assessment is correct, the RBI’s oral evidence takes on even greater weight.

The committee has now heard from nearly every stakeholder in the ecosystem: crypto exchanges both domestic and global, industry associations, the revenue and tax authorities, corporate affairs, the financial intelligence unit, and IFSCA.

The RBI was the missing piece. And in matters of monetary policy, financial stability, and foreign exchange regulation, the central bank’s word carries a weight that no other institution in India’s regulatory architecture can match. No government, regardless of its policy preferences, moves forward on financial sector regulation without the RBI’s buy-in.

The July 2 sitting will not produce a public transcript or press conference. But whatever the RBI communicates to the committee that morning is likely to shape the contours of India’s crypto policy for years to come. With an estimated 119 million crypto users in the country and India leading the Chainalysis Global Crypto Adoption Index for three consecutive years, the stakes could not be higher.

Also Read: Why Indian Traders Pay Over 10% Premium When Crypto Crashes?