Key Highlights

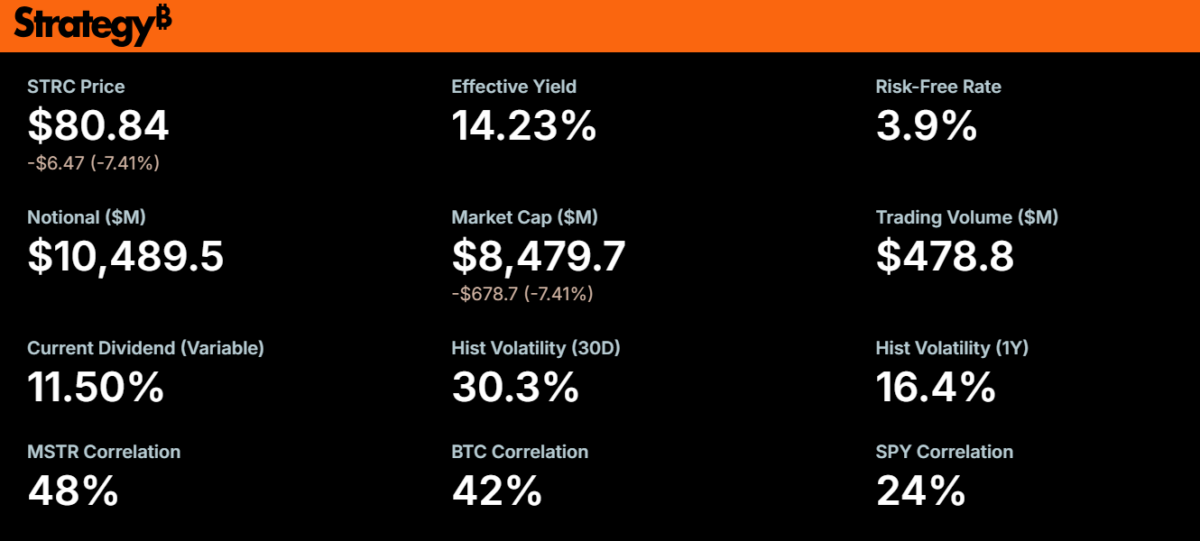

- STRC fell to nearly $80.84 on June 24, 2026, almost 19% below its $100 par target.

- The selloff pushed STRC’s effective yield to roughly 14.2%, despite its stated annualized dividend rate of 11.50%.

- Strategy marketed STRC as a product designed to trade around par and help reduce price volatility.

- The company’s SEC filings also warned that STRC could be volatile, dividends were not guaranteed, and the dividend rate could be reduced.

- Peter Schiff argues the drop exposes a structural flaw in Strategy’s Bitcoin-backed capital model.

- The bigger issue is whether Strategy’s preferred-stock machine can keep funding Bitcoin purchases when its own yield instruments trade below par.

Strategy Inc.’s most ambitious Bitcoin-linked income product is no longer trading like a low-volatility credit instrument. It is trading like a warning sign inside the capital structure of the world’s largest corporate Bitcoin holder.

The company’s Variable Rate Series A Perpetual Stretch Preferred Stock, ticker STRC, closed at $80.84 on June 24, 2026, down 7.41% in a single session, according to market data. The same data shows STRC touched an intraday low of $79.85, extending a slide that had already pushed the security to a recent low of $82.53 on June 18.

For a product designed around a $100 par value, that is not a minor technical deviation. It is a near-20% break from the level around which the preferred stock was publicly framed. With STRC currently paying an 11.50% annualized dividend rate on its $100 stated amount, the effective yield for new buyers around $80–$81 rises to roughly 14.23%.

Per Strategy’s own STRC page, the notional outstanding now stands at approximately $10.49 billion, the scale of the financing instrument that is now trading well below par.

That yield is the market’s real-time verdict. A higher yield may look attractive on the surface, but in preferred-stock markets it often reflects rising skepticism about price stability, dividend sustainability, issuer credit quality, or all three.

Adding to the pressure: Strive’s recently launched SATA preferred stock is offering a 13% annualized dividend with daily payouts, attracting trading volume that hit ~1.65 million on Friday versus a 243K average, actively competing with STRC for the same income-seeking Bitcoin-treasury capital base.

The selloff also gave new force to Peter Schiff’s long-running criticism of Michael Saylor’s Bitcoin treasury model. On June 24, Schiff accused Saylor of promoting STRC to conservative investors as a lower-volatility product. Schiff argued that STRC had been marketed to “risk-averse retirees” on the basis that volatility had been stripped away, even as the stock fell more than 17% below levels where many recent buyers entered.

Schiff’s allegations have escalated over the past several weeks. He has called STRC a “classic centralized Ponzi run by MSTR,” accused Saylor of “clear SEC violations” in his marketing of the security, and floated potential investor lawsuits. In the June 24 post, he also claimed, “Almost two years of dividends gone. Saylor clearly made material misrepresentations.”

The legal picture is more complex than Schiff’s social-media critique. Strategy’s filings were not silent about risk. The company’s SEC prospectus warned that STRC’s price could be significantly volatile, that the company could reduce the dividend rate, and that cash dividends were not guaranteed.

But securities are not sold only through prospectuses. They are also sold through narratives. STRC’s narrative was unusually bold: a Bitcoin-adjacent yield product engineered to trade around par and help strip away volatility. The June correction has exposed the difference between a marketing framework and the harsher mechanics of capital markets.

What Exactly Is STRC?

STRC is Strategy’s Variable Rate Series A Perpetual Stretch Preferred Stock, a perpetual preferred instrument listed on Nasdaq. It is not common stock, not a bond, not a Bitcoin ETF, and not a bank-like deposit product.

Strategy launched STRC in late July 2025 through one of the largest U.S. IPOs of the year. In its official July 29, 2025 closing announcement, the company said it sold 28,011,111 shares at $90 per share, raising approximately $2.521 billion in gross proceeds.

The proceeds were not raised for ordinary corporate operations. Strategy said it used the net proceeds to acquire 21,021 Bitcoin at an average purchase price of approximately $117,256 per BTC, bringing its total holdings at the time to approximately 628,791 BTC. Saylor publicly called the STRC launch the company’s “iPhone moment.”

As of June 21, 2026, per Strategy’s most recent 8-K filing, the company holds 847,363 BTC in total, worth approximately $54.8 billion at current prices, acquired at an average price of $75,651 per coin for a total cost of roughly $64.10 billion. The treasury has grown by approximately 218,572 BTC since the STRC IPO, with much of that growth financed through preferred stock and common equity issuance.

That made STRC more than a preferred-stock offering. It became another funding engine for Strategy’s Bitcoin accumulation strategy, part of what Saylor now publicly brands as Strategy’s “Digital Credit” complex, alongside STRD, STRF, and STRK preferred series.

From a capital-stack perspective, STRC sits above MSTR common equity but below more senior obligations. The SEC prospectus states that STRC ranks junior to Strategy’s existing and future indebtedness and to senior preferred stock such as STRF. It is also structurally junior to liabilities at subsidiaries.

The most important point for investors is that STRC is not directly collateralized by Bitcoin. Strategy’s own STRC information page says its preferred securities are not collateralized by the company’s Bitcoin holdings, and only have a preferred claim on the residual assets of the company.

That distinction is central. STRC is often discussed as Bitcoin-backed income, but holders do not have a secured claim on a specific Bitcoin pool. They own a preferred equity claim issued by a company whose treasury is dominated by Bitcoin and whose capital markets access is critical to sustaining the broader structure.

The Marketing Blueprint: Volatility-Stripped Bitcoin Yield

The appeal of STRC was straightforward. It offered income, a major public-market ticker, association with Michael Saylor’s Bitcoin treasury strategy, and a mechanism designed to stabilize the share price near $100.

Strategy’s own STRC page describes Stretch as a perpetual preferred stock that currently pays 11.50% annual dividends, payable semi-monthly in cash. The same page says STRC’s dividend rate is adjusted monthly to encourage trading around STRC’s $100 par value and to help “strip away price volatility.”

That phrase is now the center of the controversy.

For Strategy, it describes a mechanism. If STRC trades below $100, the company can adjust the dividend rate to make the security more attractive to income buyers. If STRC trades above $100, the company can reduce the rate to cool demand and pull the price back toward par.

For many investors, however, “strip away price volatility” can sound like a broader promise: that STRC would avoid the kind of drawdowns associated with Bitcoin, MSTR common stock, or other high-beta crypto assets.

That difference matters. The official mechanism was about managing price behavior. The market appears to have interpreted the product as a more stable yield vehicle.

Strategy doubled down on the product’s design in June 2026. On June 8, the company announced that shareholders approved a move from monthly to semi-monthly dividend payments. Strategy said paying dividends twice a month was designed to stabilize price, dampen cyclicality, drive liquidity, and grow demand.

The market did not respond as intended. STRC moved further away from par.

How the Variable-Rate Mechanism Was Supposed to Work

STRC’s design is based on an equilibrium idea: the dividend rate is a lever that can influence market price.

When STRC trades below $100, Strategy can raise the dividend rate. A higher payout should attract buyers, increasing demand and pushing the price toward par. When STRC trades above $100, the company can lower the rate, reducing demand and preventing the stock from trading too far above its stated value.

In theory, STRC shifts volatility away from price and into the dividend rate. The security is not supposed to trade like MSTR common stock. It is supposed to act like a preferred income product whose yield adjusts enough to keep the price relatively stable.

The June selloff tested that theory. The dividend rate started at 9.00% at launch in August 2025 and climbed every month for seven straight months to reach 11.50% by March 2026. It has now held at 11.50% for four consecutive months, through June. Strategy maintained the rate after STRC’s monthly volume-weighted average price (VWAP) reached $99.62, allowing the company to keep shares “close enough” to the $100 target without raising the rate further. That stability has since collapsed.

As of June 2026, Strategy’s official STRC page lists the variable annualized dividend rate at 11.50%, while also warning that the current rate is not indicative of future rates, that the rate may be significantly lower, and that the cash dividend is not guaranteed.

Those disclaimers are important. The SEC prospectus goes further, warning that Strategy may be unsuccessful in maintaining STRC near $100 and that even if the company increases the dividend rate when STRC trades below par, the price may remain below $100.

That is exactly the problem now facing STRC holders. The rate is already elevated. The effective yield is above 14%. Yet the share price remains far below par.

The mechanism has not failed legally. It may still be operating as disclosed. But the market is challenging whether it can work economically during a Bitcoin-led stress cycle.

Data Deep-Dive: Marketing vs. Reality

| Milestone | Market Price | Premium / Discount to $100 Par | Effective Annualized Yield | Observable Market Link to Bitcoin |

|---|---|---|---|---|

| Launch: July 2025 | $90 IPO price | 10% below par | Approx. 10.0% using initial 9.00% rate | Indirect, via Strategy’s Bitcoin treasury model |

| Peak: January 2026 | Around $100+ | Near / slightly above par | Lower near par | Moderate; product appeared stabilized |

| Recent Low: June 18, 2026 | $82.53 intraday low | Approx. 17.5% below par | Above 13% | High during Bitcoin and MSTR weakness |

| Current State: June 24, 2026 | $80.84 close / $79.85 intraday low | Approx. 19% below par | Approx. 14.2% | Very high during market stress |

The data shows why STRC has become a credibility test for Strategy’s capital engineering.

For much of early 2026, the instrument appeared to behave close to its intended design. It traded near $100, paid a large dividend, and gave income-focused investors a way to participate in Strategy’s Bitcoin-linked credit story without owning MSTR common stock.

June changed the market signal. STRC’s discount widened even though the dividend rate stood at 11.50%. On June 18, StockAnalysis data shows STRC hit an intraday low of $82.53 on unusually heavy volume of more than 10.6 million shares.

Strive CEO Matt Cole called June 18 “the most difficult day in the history of digital credit,” as both STRC ($82.53 intraday low, $88.59 close) and Strive’s own SATA ($92.88 intraday low, $97.71 close) sold off sharply. On June 24, it fell again, closing at $80.84.

A higher effective yield did not bring STRC back to par. Instead, the market demanded even more compensation for holding it.

That is the uncomfortable lesson. In healthy preferred markets, a higher yield can attract demand. In stressed preferred markets, a higher yield can signal that investors are pricing in deeper risk.

The ATM Problem: Why STRC Below Par Matters Beyond Holders

STRC’s decline is not only a mark-to-market loss for income investors. It also affects Strategy’s ability to use STRC as a funding tool.

When STRC trades above its $100 par value, Strategy can issue new shares through an at-the-market program and use the proceeds to buy Bitcoin. That is the positive version of the flywheel: preferred-stock demand funds BTC purchases, BTC accumulation supports Strategy’s story, and capital markets remain open for further issuance.

When STRC trades below par, that channel becomes impaired.

STRC’s fall below $100 had paused the above-par share sales Strategy uses to fund Bitcoin purchases. The same report said the decline weakened a major channel the company uses to raise cash for BTC accumulation.

Per Strategy’s June 22 8-K filing, the company still has unused ATM capacity: MSTR $25.4 billion (including a $21 billion expansion announced in March 2026), STRC $17.5 billion, STRD $4.0 billion, and STRK $2.1 billion. Over $25.2 billion in combined preferred stock issuance capacity remains untouched, but issuing STRC at $80 versus $100 means materially worse economics for each dollar raised.

This is where the issue becomes structural. STRC was designed to be a flexible funding instrument. But below par, it becomes more expensive to issue. Selling new preferred shares at a discount can reinforce the market’s concern that investors require higher compensation to take Strategy’s credit risk.

That changes the economics of the Bitcoin accumulation model.

Strategy’s recent ATM activity makes the rebalancing concrete. Between June 15 and June 21, 2026, the company sold about 2.71 million MSTR shares for around $335.5 million, but deployed only around $35 million to purchase 520 BTC at an average price of $67,068. The remaining ~$300 million was retained as cash, pushing the USD Reserve to $1.4 billion. That 10/90 BTC-to-cash deployment ratio is a striking inversion of the prior pattern, signaling that Saylor’s Strategy is now prioritizing credit-quality defense over BTC accumulation.

Strategy can still issue common stock. It can still sell other securities. It can still use cash reserves. But if STRC is no longer an efficient issuance channel, one important layer of the capital machine becomes less useful.

The Symbolism of the 32 BTC Sale

The STRC stress has also forced Strategy into a sensitive position: selling Bitcoin to support preferred-stock obligations.

Strategy disclosed on June 1 that it had sold 32 BTC for about $2.5 million in late May to fund STRC distributions. The sale was tiny compared with Strategy’s overall Bitcoin holdings, but symbolically powerful, and unprecedented within the modern Strategy era. Per The Crypto Times’ reporting, the sale was Strategy’s first Bitcoin disposal since 2022, ending a roughly four-year buy-only streak that had been the cornerstone of Saylor’s public brand.

Saylor’s public brand has long been built around Bitcoin accumulation and the idea of not selling BTC (which he later tried to sell as advice only for retail investors and not meant for Strategy). The 32 BTC sale did not break Strategy’s balance sheet. But it showed that preferred dividends create dollar obligations that Bitcoin itself does not naturally pay.

That is the core tension in Strategy’s model. Bitcoin may appreciate over the long term, but it does not generate cash flow. Preferred dividends require cash.

The sale therefore turned Bitcoin from a treasury asset into a funding source, even if only at the margin.

Peter Schiff’s Criticism: Marketing, Retirees and “Death Spiral” Risk

The bull defense is straightforward: STRC’s drawdown is not proof of structural failure. It is a market dislocation.

Analysts sympathetic to Strategy’s model argue that the late-June selloff was driven by forced liquidations, margin calls and weak-handed retail selling rather than a breakdown in the preferred stock’s architecture. If leveraged holders bought STRC for income, pledged it on margin, and then faced falling collateral values as Bitcoin and MSTR sold off, forced selling could push STRC temporarily below fundamental value.

Under that interpretation, the discount is not the market saying Strategy cannot pay. It is the market clearing out excess leverage.

There is some logic to this defense. Preferred stocks can trade below par during liquidity shocks even when issuers continue paying dividends. Retail-heavy ownership can amplify moves. If the price decline was driven by technical selling, then higher yields may eventually attract buyers who view the low-$80s price as an opportunity rather than a warning.

But Schiff’s counterargument goes beyond the cause of the initial drop. His claim is that once STRC trades far below par, the low price itself becomes a structural problem.

Schiff’s sharpest formulation, which is substantively consistent with his documented X posts, captures the reflexive risk: “The lower price on STRC forces MSTR to raise the dividend if it wants to sell more STRC. Since it can’t it either must sell MSTR at a huge discount, or BTC. That’s the death spiral!”

That quote captures the reflexive risk embedded in the structure.

If STRC trades near $100, Strategy can use it as an efficient funding engine. It can issue preferred stock, raise cash, buy Bitcoin, and continue building the treasury narrative. If STRC trades at $80, that engine becomes less efficient. New issuance at a steep discount is more expensive. To restore demand, Strategy may need to increase the dividend rate. But increasing the dividend rate raises future cash obligations.

Those cash obligations must be funded somehow. Strategy can use cash reserves. It can issue MSTR common stock. It can issue other preferred securities. It can sell Bitcoin. Or it can reduce or suspend dividends, which would likely damage the preferred-stock complex and validate market fears.

Each option has trade-offs.

Issuing common stock when MSTR is under pressure dilutes common shareholders and can weaken the premium-to-Bitcoin-net-asset-value story. MSTR is currently trading near $94.13, down $9.71, meaning common-stock issuance is occurring at depressed multiples. Issuing more preferred stock at higher yields increases the fixed burden on the company. Selling Bitcoin undermines Saylor’s long-standing “never sell” ethos and risks turning a treasury strength into a liquidity source. Cutting dividends would protect cash but damage STRC’s core identity as an income product.

That is why Schiff’s “death spiral” phrase resonates even with investors who reject his broader anti-Bitcoin worldview. It is not about whether Bitcoin is valuable. It is about whether Strategy’s capital structure becomes increasingly expensive to maintain when its own funding instruments trade poorly.

Schiff also argued that recent buyers had seen almost two years of dividend income erased by the price decline. That point is less about insolvency and more about investor experience. A 14% yield sounds compelling until the principal drawdown reaches nearly 20%. For retirees or conservative income investors, the mark-to-market loss can overwhelm the income thesis.

Schiff has gone further than the “death spiral” formulation. He has separately argued that Strategy’s 1,550 BTC purchase for ~$101 million in early June was actively value-destructive for common shareholders, since the company issued more equity than the per-share Bitcoin it added. He called this outcome a negative Bitcoin yield.

He has also accused Saylor of clear SEC violations in marketing STRC to risk-averse retirees, claiming retirees may have an ironclad lawsuit against the company. Strategy’s own internal BTC Yield metric, its measure of Bitcoin per share accretion, stood at 11.8% YTD as of the latest filing, down from 13.3% in late May, suggesting some validity to Schiff’s dilution concern, even if the framing as “negative” remains contested.

The bulls may be right that forced selling caused the shock. Schiff may be right that the shock exposes a structural weakness. Both can be true.

The deeper issue is that STRC is not just a security. It is part of Strategy’s issuance machine. When it trades well, it supports the machine. When it trades badly, it raises the cost of keeping the machine alive.

The Bull Case: Forced Liquidations, Not Structural Failure

Strategy bulls have a different explanation. They argue STRC’s selloff reflects forced liquidations, margin calls and weak retail positioning rather than a breakdown in the instrument itself.

That argument has been articulated by named institutional analysts. Analysts from Benchmark and TD Cowen pushed back against the death-spiral narrative: “The death-spiral story assumes that Strategy is one bad week from selling bitcoins, and it skips several steps to get there.”

That argument has merit. Preferred stocks can trade below par during liquidity events. Retail-heavy ownership can amplify selling pressure. A product bought for income can become vulnerable if investors used leverage or expected near-par stability without fully pricing Bitcoin-linked risk.

Under the bull case, STRC’s fall is not evidence that Strategy cannot pay. It is evidence that the market temporarily mispriced liquidity and leverage.

There is also no evidence that Strategy is near insolvency. The company remains the largest corporate Bitcoin holder, continues to raise capital, and has built a dedicated U.S. dollar reserve. Strategy has repeatedly emphasized that its preferred products are part of a broader digital-credit strategy, not standalone yield promises.

Saylor himself responded to the June 24 stress with a public reaffirmation, posting on X, “Digital Credit is income for investors who believe in Bitcoin. $STRC.” Apart from this, he has also continued his customary Sunday “Working Better” posts; his standard signal that Strategy has bought more Bitcoin.

Still, the bull case does not fully answer Schiff’s structural point. Even if forced selling caused the initial drop, the lower price can still impair future issuance. In corporate finance, technical selling can become fundamental if it raises the issuer’s cost of capital.

That is why STRC’s discount matters. It does not need to prove immediate distress to become a problem. It only needs to make Strategy’s capital-raising machine more expensive.

Cash Reserves and Dividend Coverage Under Scrutiny

Strategy has taken steps to strengthen its liquidity position.

Strategy selling approximately 2.71 million MSTR shares, and bringing cash reserves to approximately $1.4 billion is an important buffer. It gives Strategy room to meet obligations without immediately relying on distressed Bitcoin sales.

The USD Reserve trajectory shows the velocity of the cash build:

- May 31, 2026: $871 million (6.1 months of dividend coverage)

- June 14, 2026: $1.1 billion

- June 21, 2026: $1.4 billion

That represents more than 55% growth in three weeks. Saylor himself has publicly stated that he wants the reserve at above 18 months of coverage, meaning the company is rebuilding aggressively toward a target it has not yet hit.

The drain on the reserve was not gradual. In May 2026, Strategy used approximately $1.38 billion to repurchase $1.5 billion of 2029 convertible notes at an 8% discount to par, cutting its convertible debt load from $8.2 billion to $6.7 billion. The buyback was funded through a combination of cash reserves, a $2 billion STRC issuance, and $84 million in common stock sales. The transaction was financially rational, buying back debt at a discount, but left the dividend buffer thin.

Annualized dividend obligations tied to Strategy’s preferred-stock products had climbed to roughly $1.2 billion, and cash reserve coverage had fallen from more than seven years to about 14 months, and that restoring coverage to 24 months would require roughly $2.8 billion in cash.

Those numbers do not mean Strategy is out of cash. They do show why institutional investors are now focused on liquidity, not just Bitcoin holdings.

A company can be asset-rich and still face funding pressure if its liquid cash reserves do not fully reassure preferred-stock investors. Bitcoin may support balance-sheet value, but preferred dividends are paid in dollars.

The Fine Print Was Clear, But Was the Message?

Strategy’s legal disclosures were extensive.

The SEC prospectus warned investors that Strategy could reduce STRC’s dividend rate, that the trading price could decline significantly, that the company may not have sufficient funds to pay dividends in cash, and that the board may choose not to pay accumulated dividends for any reason.

The prospectus also warned that even if Strategy adjusts the dividend rate to maintain STRC near $100, those adjustments may fail. It said market expectations around dividend-rate changes could themselves affect STRC’s price.

Strategy’s own STRC page also states that there is no guarantee of returns, liquidity, or future performance. It says STRC is not a bank deposit, not FDIC insured, and not regulated like bank accounts, money market funds, Treasuries, or similar instruments.

That is the legal shield.

But investor experience is shaped by more than legal text. STRC was marketed around stability, innovation and volatility reduction. The public narrative emphasized the mechanism designed to keep the product near par. The prospectus emphasized that the mechanism might not work.

June forced the market to confront both truths at once.

Broader Implications for Bitcoin Treasury Companies

STRC’s selloff matters because it is a stress test for a broader model now spreading across public markets: the Bitcoin treasury company.

The model works best when three conditions hold:

- Bitcoin rises or remains strong.

- Equity and preferred securities trade at healthy premiums or near target values.

- Capital markets remain willing to fund additional Bitcoin purchases.

When those conditions are present, Strategy’s machine looks elegant. The company issues securities, buys Bitcoin, increases its BTC holdings, and reinforces investor demand for its capital instruments.

When conditions reverse, the machine becomes more fragile. Preferred holders worry about dividend coverage. Common shareholders worry about dilution. Credit investors demand higher yields. Bitcoin sales become politically and narratively sensitive.

That is the key lesson from STRC. Financial engineering can redistribute Bitcoin volatility across different securities, but it cannot fully eliminate the underlying exposure. STRC holders do not own Bitcoin directly, but their security is still tied to Bitcoin through Strategy’s treasury value, investor sentiment, capital markets access, and the credibility of Saylor’s accumulation strategy.

In bull markets, that structure looks like innovation. In drawdowns, it looks like leverage wearing a different label.

Was Peter Schiff Right?

On the narrow question, Schiff has a point.

STRC has not behaved like a product with volatility stripped away. A fall from near par to roughly $80 is real volatility. For recent buyers, the mark-to-market loss can overwhelm multiple months of dividend income. The fact that STRC still trades far below par despite an 11.50% dividend rate shows that the market is demanding more compensation for risk.

On the broader claim, more caution is needed.

Calling STRC a Ponzi or alleging fraud is a much higher bar. Strategy disclosed many of the relevant risks in regulatory filings. The product’s dividend was never guaranteed. The company warned that the stock could be volatile and that the par-maintenance mechanism could fail.

The fair conclusion is more nuanced: Schiff is stronger on the marketing-versus-reality argument than on the legal argument.

The filings said risk remained. The marketing emphasized volatility reduction. The market is now deciding which message investors actually heard.

What Investors Should Watch Next

The next phase of the STRC story depends on five indicators.

1. Dividend Rate Resets

If Strategy raises STRC’s dividend rate again, the move may support price temporarily. But it also increases cash obligations. If the company does not raise the rate enough, the market may view that as a sign that Strategy is unwilling or unable to defend par. The pressure from Strive’s competing SATA at 13% is now an additional input; Strategy may have to match or exceed that yield to keep STRC competitive in the income-buyer segment.

2. Cash Reserve Coverage

Strategy’s U.S. dollar reserve is now a central part of the credit story. Investors will watch whether the company continues rebuilding reserves or prioritizes new Bitcoin purchases. The shift to a 90/10 cash-to-Bitcoin allocation in the June 15-21 ATM cycle is the metric to track in subsequent 8-Ks. A return to a more aggressive Bitcoin-accumulation ratio would signal renewed confidence; a continued tilt toward cash would confirm the credit-defense thesis.

3. STRC’s Distance From Par

A move back toward $100 would support Strategy’s claim that the mechanism can work through stress. A prolonged discount in the $80s would weaken confidence in the structure.

4. ATM Issuance Capacity

If STRC remains below par, Strategy’s ability to issue new STRC shares efficiently stays limited. That could shift more burden to common-stock issuance or other funding tools. MSTR’s price near two-year lows means the alternative, i.e. common-stock issuance, is also impaired.

5. Bitcoin Sales

The 32 BTC sale was small in comparison to its treasury and accumulations. But, repeated Bitcoin sales to fund preferred dividends would be much more important. That would suggest the preferred-stock structure is beginning to pull liquidity from the treasury asset itself.

Conclusion: The Fine Print Reckoning

STRC was designed to solve a difficult problem: convert Strategy’s Bitcoin treasury strategy into an income product that could trade near par while reducing price volatility for holders.

For several months, that design appeared to work. Then June 2026 arrived.

The shares broke sharply below par. The effective yield rose above 14%. Peter Schiff’s criticism went viral. Strategy’s preferred-stock machine suddenly looked less like volatility-stripped Bitcoin yield and more like a credit instrument exposed to Bitcoin volatility, liquidity pressure and capital-market confidence.

The ultimate answer is not binary. Schiff’s warnings about structural reflexivity carry weight. A below-par STRC price can raise Strategy’s cost of capital, weaken ATM issuance, increase pressure to lift dividends, and force harder choices between dilution, reserve building and Bitcoin sales.

At the same time, Strategy’s legal disclosures were explicit. The company warned investors that STRC could be volatile, that dividends were not guaranteed, and that the par-targeting mechanism could fail.

That is the fine print reckoning.

STRC may still recover if Strategy rebuilds liquidity, stabilizes the dividend path and restores confidence in the $100 par mechanism. But the June selloff has already changed the debate. Investors are no longer asking only how much Bitcoin Strategy owns. They are asking whether Bitcoin-backed financial engineering can fund dollar-denominated obligations through a full market cycle without turning the treasury asset into a liquidity source.

The product was marketed around volatility reduction. The market is now pricing the volatility that remains.

Also Read: MicroStrategy Stock Mirrors Bitcoin’s Wildest Swings: 7 Times BTC Moved MSTR