On a humid June morning in 2026, an Ahmedabad-based software engineer sits in a co-working space and watches two numbers refuse to agree. The global USD/INR mid-market rate is sitting at roughly ₹95 that week; the rupee has just touched a five-week high. Yet when he opens an instant-buy interface to convert rupees into USDC, the effective price flashes back somewhere north of ₹101. On a calmer regulated venue it reads about ₹98. Either way, he is paying more for a token engineered to be worth exactly one dollar than the dollar itself costs.

Think of it as the airport currency counter, the booth where nobody in their right mind changes money because the rate is daylight robbery. Now imagine that booth is the only door into the building. That is the position every Indian crypto buyer is in, and most of them never notice, because the app shows one clean number with the markup already folded inside, the way “taxes and fees” disappear into a flight price you can’t itemise.

That gap, anywhere from 2% on the cleanest venues to 7–8% on the convenience rails, and historically spiking into double digits during bull runs, is not a glitch, not an exchange scam, and not the buyer’s fault. It is a charge the system collects quietly, and it traces back to three deliberate policy choices: FEMA capital controls, a 1% tax on every transaction, and a 30% flat tax on gains with no loss offset.

But the engineer’s few hundred rupees of overpayment is only the visible edge of something far larger. The same wall of friction that taxes him at the on-ramp has driven the bulk of India’s crypto economy out of the country entirely.

By the exchanges’ own data, presented to Parliament in May 2026, close to 90% of Indian virtual-digital-asset trading volume now happens offshore, beyond the reach of the tax authority that the policy was built to feed. The small daily overcharge and the great offshore exodus are the same wound seen from two sides: the state priced its own market so high and starved it of liquidity so completely that anyone sharp enough to notice simply left, leaving the people who never properly read or understood the fine print to absorb the markup at home.

1. Proving it exists: The mechanics, the math, and the two premiums

How an INR trade actually works

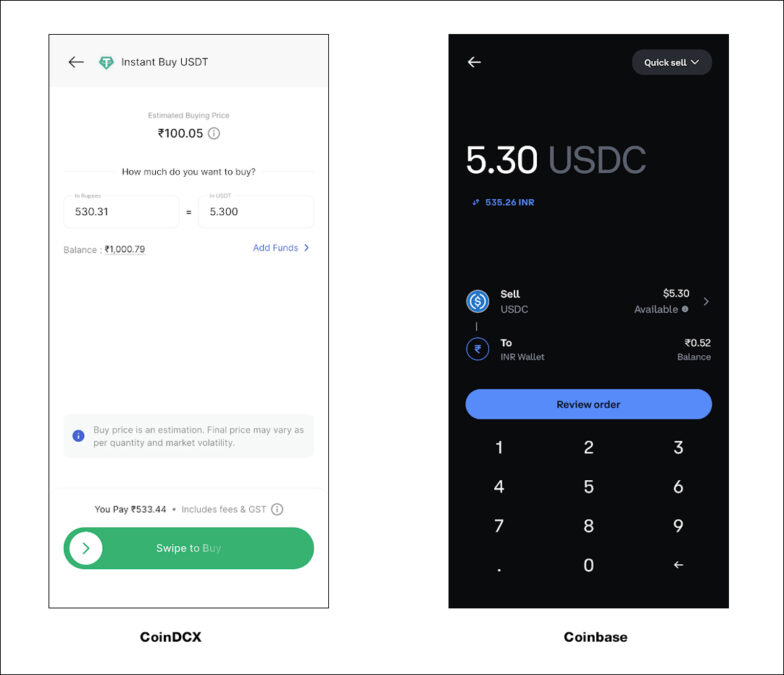

On a frank note, Indian users almost never buy Bitcoin or Ethereum directly with rupees in any seamless global sense. The journey starts with local INR pairs, but the real chokepoint is the stablecoin gateway, USDT-INR or USDC-INR. These pairs are the bridge from the regulated rupee world into the global, dollar-pegged crypto economy. Without liquid stablecoin on-ramps, trading on global platforms would stall.

In practice: a user logs into WazirX, CoinDCX, CoinSwitch, ZebPay, or Coinbase’s localised India interface and deposits rupees over UPI, IMPS, or bank transfer. From there they enter either the spot stablecoin market or, more often, the peer-to-peer (P2P) section that carries the bulk of volume—scrolling live offers from individuals and trading firms, picking one, sending a transfer, and waiting for the seller to release the coins. When everything aligns it takes minutes; a KYC re-check or a payment dispute can stretch it to hours.

Once the stablecoin is in hand (unless they opt for direct purchase of crypto using INR pairs, which is also of course at a premium), the user reaches the global market, where Bitcoin trades almost at the same price as a desk in New York, London, Singapore, or Dubai. But the local premium is now permanently baked into the investor’s cost basis from the moment of entry, meaning they are already behind before they have bought a thing.

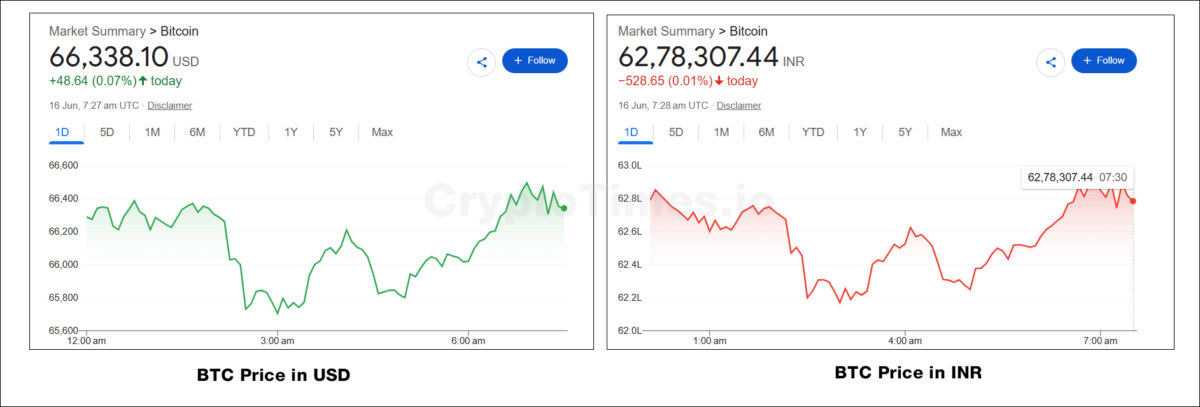

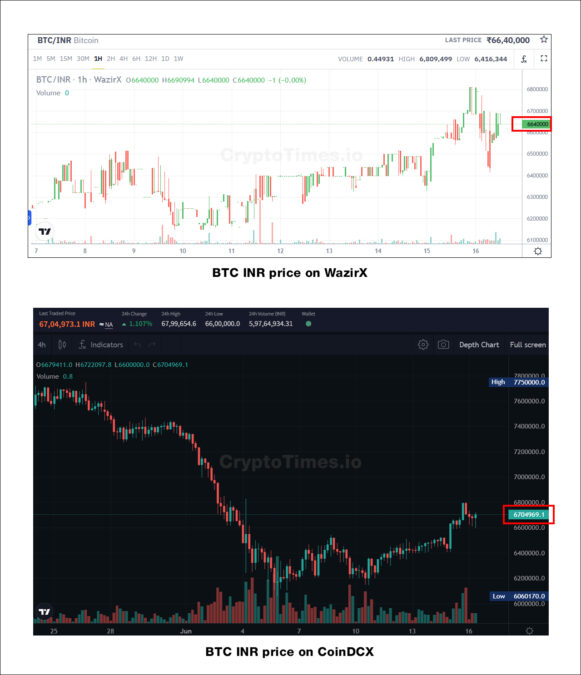

At the time of writing, BTC is priced at $66,338—which amounts to approximately ₹62,78,307 at the prevailing USD price of 94.5 in INR.

Distinctively, on two of the largest Indian crypto exchanges, BTC is trading at ₹66,40,000 and ₹67,04,973—on WazirX and CoinDCX, respectively. This marks a roughly 5-6% premium compared to the global BTC-INR price.

Even on Coinbase, which recently made its grand entry into India, BTC-INR is trading at ₹66,12,738—which is at a 5.33% premium.

The trap is one-directional. On the way out, users sell crypto for stablecoins at global prices, then convert back to rupees locally, where the premium is thinner and sometimes even slightly negative during heavy selling. So you pay the toll to get in, but you don’t get it back on the way out. That asymmetry quietly nudges Indian traders to treat crypto as a quick speculative bet rather than a long-term holding, and turns a simple purchase into a daily chore of hunting across apps to shave off a few paise.

The mathematics

Let’s examine the correct premium percentage:

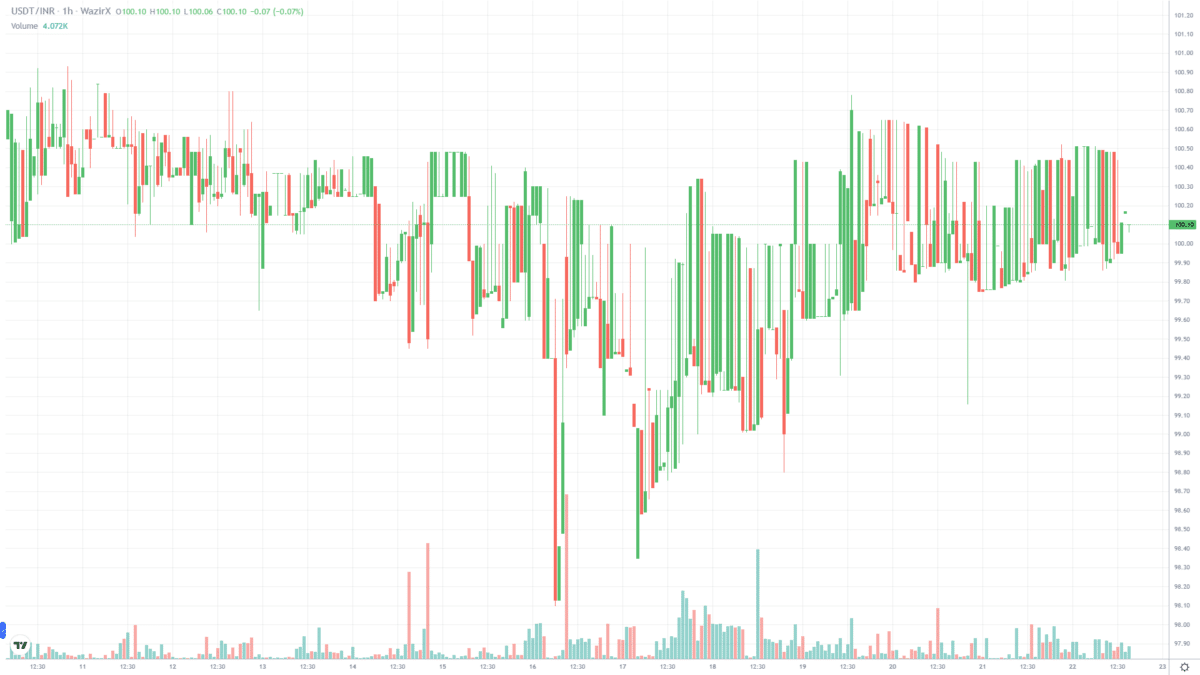

- S = spot USD/INR mid-market rate (mid-June 2026: ₹94.5)

- P = local buy price for USDT/USDC (currently trading near ~₹100.5)

- Premium (%) = ((P − S) / S) × 100

- Using the current snapshot of P = ₹100.50 against S = ₹94.50

- Premium = ((100.50 − 94.50) / 94.50) × 100 ≈ 6.35%

For a retail user converting ₹5,00,000 at that rate, the shortfall versus the theoretical spot rate is roughly 316 USDC, about ₹31,700 gone before a single trading fee or any slippage.

Let’s dive a little deeper into what it actually costs at every size of wallet taking the spot rate in around mid-June 2026 of roughly ₹95 per dollar, and the local buy price (from near-parity on quiet venues to ₹101-plus on instant-buy screens). At a mid-June instant-buy price of ₹101.85 against a ₹95 spot, that is a premium of about 7.2%.

Now watch what that does to real people:

- The college student in Indore who puts in ₹10,000 of saved-up pocket money loses about ₹700 the instant the trade clears, before the price has moved a single cent. It is as if he bought a ₹10,000 phone and was charged a ₹700 “entry fee” he can never get back, win or lose.

- The freelance designer in Pune moving ₹50,000 hands over ₹3,500, roughly a week’s grocery bill, for the privilege of holding digital dollars.

- A retail user converting ₹5,00,000 is short about ₹34,000 versus the true rate, gone before a single fee or any slippage.

Scale it up and it stops being pocket change. At a global price of $66,000, one Bitcoin costs about ₹62,00,000 at the real exchange rate, but ~₹67,00,000 at the 7.2% premium. That is more than ₹4,00,000 in pure overpayment on a single coin, enough to buy a small car, vanishing into a markup the buyer never agreed to line by line.

Even a 0.5 BTC position carries an extra burden above ~₹2 lakhs. For active traders running multiple entries a month, or HNIs and institutions building real positions, the annual drag compounds into lakhs or crores. The cruelty of it is the invisibility: an Indian needs the price to climb several percent further than a foreigner does just to break even, and almost none of them know that’s the deal they took.

The single most important move: There are two premiums, not one

Most coverage tangles every cause together and quotes one scary number. The truth is that the premium is really two charges stitched into one, and they could not be more different in character.

- The honest part (~2–4%). This is the genuine, unavoidable cost of operating behind India’s capital-control wall. Dollars can’t freely flow in to compete the gap away, so a baseline markup sticks. This part is a defensible price of monetary sovereignty, even a perfect tax regime wouldn’t erase it. It is the part India chose, with eyes open.

- The self-inflicted part (everything above that, and the blow-outs during stress). This is the extra widening caused by the 1% transaction tax, which drove out the professional traders who would otherwise compete the spread back down. It is a pure own-goal, and it is completely reversible, which means most of what the Indore student and the Pune designer overpay is not the price of sovereignty at all. It is the price of a mistake nobody has fixed.

Pulling these two apart is the whole game. The first is the cost of a wall India built on purpose. The second is a hole India shot in its own foot, and then taxed the bleeding.

2. Why it persists: Capital controls, then a self-inflicted liquidity drought

The premium is not a fee an exchange sets. It grows out of plain supply and demand in a heavily constrained environment. Sellers list stablecoins above parity because local buyers will pay for speed and near-instant UPI settlement; exchanges merely match orders and pocket a small fee on the inflated total.

The reason the gap never closes is the wall itself: India’s capital-control regime under the Foreign Exchange Management Act (FEMA) of 1999, policed by the Reserve Bank of India (RBI). The RBI’s job is to defend the rupee, guard foreign-exchange reserves, and stop money fleeing the country. Crypto platforms are registered as digital-asset service providers but are not licensed foreign-exchange dealers, so they can’t legally convert rupees into dollars at scale.

Even the official route for sending money abroad comes wrapped in paperwork, a 20% tax collected upfront on larger sums, and banks that freeze accounts showing heavy crypto activity.

The result is a market where demand for digital dollars surges every bull run, but cheap real dollars simply cannot get in to cool the price down. The door only opens one way.

The liquidity drought, and the tax that engineered it

The least-discussed driver is the chronic thinness of INR liquidity. Platforms display BTC/INR, ETH/INR, and SOL/INR books, but depth behind them is shallow versus their USDT counterparts.

A modest order can move an INR pair several percent in seconds. So serious traders follow a two-step path: buy USDT despite the premium, then trade on deep global USDT books where the BTC/USDT order book shows tens or hundreds of millions of dollars within 1–2% of mid-price.

Thus, premium becomes the accepted toll for institutional-grade liquidity, and because so many users rush the stablecoin gateway to reach those pools, demand stays elevated and the premium self-reinforces.

Moreover, USDT/USDC demand in India shows both patterns. During bull runs, demand surges sharply as retail investors rush in to capture Bitcoin and altcoin rallies, often pushing the premium into double digits. However, even between cycles, baseline demand continues to climb steadily with broader crypto adoption as more users onboarding, more institutions testing allocations, rising awareness of dollar-pegged assets as a hedge against rupee volatility, and increasing use of stablecoins. This secular uptrend means the premium has become semi-permanent rather than purely cyclical.

The market the tax killed on purpose

Here is the part that turns a structural quirk into a scandal. In any healthy market, professional traders, market makers, make their living by stepping in whenever a price drifts too far from fair value, buying low, selling high, and dragging it back. They are the reason a litre of petrol costs the same at two pumps across the road. They are exactly the people who would have competed India’s premium down to almost nothing.

The 1% transaction tax wiped them out. And you don’t need a think-tank to see why, it’s arithmetic a shopkeeper would recognise. Picture a sabzi-seller taxed 1% not on his profit but on the full value of the produce every time it changes hands. He buys at ₹100, sells at ₹100.50, a wafer-thin honest margin, and the taxman still takes ₹1 on the ₹100. He has lost money on a winning sale.

That is precisely what the levy does to a market maker earning a tenth of a percent per trade: it hands them a 1% bill on the entire sum that moves, so they are underwater before they start. Independent estimates put the working-capital wipeout at over 90% within a single quarter, with the withheld cash locked up for months awaiting a refund. The tax didn’t just discourage these traders. It made their entire business mathematically impossible, and with them gone, there is nobody left to close the gap. The premium isn’t a market failure. It’s a market the policy deliberately emptied.

This is also why INR order books are so thin. An INR market is like a small-town local market: try to buy in any size and you clear out the stalls and shove the price up against yourself. The global dollar market is the wholesale yard, deep enough to swallow your order without blinking. So serious traders buy stablecoins despite the premium and immediately move to the deep global pools, which keeps demand for stablecoins permanently high, which keeps the premium high. The trap feeds itself.

Punished for being careful

The headline tax numbers — 30% on gains, 1% on transfers — understate the bite. Under Section 115BBH, the 30% applies no matter your income or how long you held, and, most punishingly, a loss on one coin cannot be set against a gain on another.

Here is what that means in plain terms. Imagine betting on two cricket matches. You win ₹10,000 on one and lose ₹10,000 on the other, you walk away exactly even, not a rupee richer. But the taxman counts only the match you won, and demands ₹3,000. You are taxed on a year in which you made nothing. That is the no-offset rule, and it falls hardest on careful investors who spread their bets: the very behaviour every financial adviser preaches.

Add in fees and costs that can’t be deducted, and on a mixed portfolio the real tax burden routinely tops 50%. The system doesn’t just tax success. It taxes prudence, and quietly shows the door to anyone sophisticated enough to do the sum.

The platforms respond: “Not a premium we set”

Asked to account for the gap, the exchanges pointed The Crypto Times in the same direction: away from themselves and toward policy. It is a telling convergence: the firms accused of overcharging and the case against the regime broadly agree on the cause.

A Coinbase spokesperson said the markup is structural rather than platform-imposed, and that its pricing is fully disclosed before a trade clears:

“Coinbase displays the final INR price for any USDC purchase on the order confirmation screen before a transaction is completed (including spread details), so users can see exactly what they will pay prior to executing a trade. The pricing differences being referenced are not unique to Coinbase and are broadly observed across Indian crypto platforms. They reflect local market conditions, particularly the impact of the 1% TDS, which increases costs for users and reduces liquidity. Any price differences are therefore a reflection of local supply and demand dynamics, the withholding tax imposed by the government which impacts liquidity, and local order books due to capital constraints, not a platform-imposed premium. We take pride in our transparent pricing practices.”

Ashish Singhal, Co-Founder of CoinSwitch, made the same core argument, that a stablecoin’s rupee price and the USD-INR rate are two different markets, and any premium reflects local demand rather than a platform decision:

“The price of USDT or USDC on an exchange is determined by market dynamics rather than being manually set by the platform. Like any actively traded asset, the price reflects real-time demand and supply conditions among buyers and sellers in the market. When comparing the USDT/USDC-INR price to the USD-INR exchange rate, it is important to recognize that these are two different markets. Any premium or discount that may emerge is largely driven by market structure and participant activity rather than a platform-determined pricing decision.”

Whether the buyer can actually see the cost, Singhal insisted disclosure is complete: “Before completing any transaction, users are shown the live buy and sell prices of the asset, along with the quantity they will receive and the total transaction value. He added, “At CoinSwitch, as a platform we only make through our brokerage cuts and there are no over and above or undisclosed fees.”

And pressed on why Indians pay more for a coin than for the dollar it tracks, he attributed it to demand outrunning supply, “While stablecoins such as USDT and USDC are designed to track the US dollar, their market price on an exchange can fluctuate based on regional demand and supply conditions. India has historically seen strong demand for dollar-linked digital assets… At times, demand can outpace available liquidity, resulting in a temporary premium. This is not unique to India and has been observed across fiat and stablecoin pairs.”

CoinDCX, one of India’s largest exchanges by volume, was approached for comment but did not respond by the time of publication.

Two things are worth drawing out of these replies. First, the exchanges’ own explanation, the 1% TDS, thin liquidity, capital constraints, local supply and demand, is, almost word for word, the argument of this piece: even the accused name policy, not themselves, as the culprit.

Second, on transparency there is a real gap the responses don’t quite close. Showing a final, all-in rupee figure on a confirmation screen is genuine disclosure, and both firms are entitled to the claim. But it is not the same thing as a buyer grasping that the number in front of them sits several percent above the dollar’s true value.

The price is shown; the premium, for most users, still hides in plain sight, which is exactly why the reform that matters is not “show a number” but “show the spread against mid-market.”

3. Cheaper to buy actual dollars-

To see how strange the premium is, let’s compare it with what regulated channels charge for actual dollars. India’s big banks, such as SBI, HDFC, ICICI, apply a forex markup of roughly 1.5–3.5% over interbank, plus 18% GST on the markup, working out to about ₹1.50–₹3.50 per dollar. Fintech remittance services like Wise run tighter, at 0.5–1.5% over mid-market.

So a crypto premium of 6–10% means Indians are paying two to four times the worst bank rate, to buy a token built to be worth exactly one dollar. It dwarfs South Korea’s famous “Kimchi premium,” which historically sat near 1.6%.

Even crisis economies make India’s premium look odd: Argentina’s stablecoin premium averaged around 7% in 2025, but it had hyperinflation and hard dollar caps. Nigeria’s fell from 6% to 2% after currency reform. India sustains a comparable markup despite a relatively stable rupee and no such caps. Indians, in short, pay a crisis-economy premium without a crisis.

On tax, India is an outlier among peers. The United States lets you offset losses and even deduct some against ordinary income. Germany drops the rate to zero on assets held over a year. Indonesia runs a light ~0.1% transaction levy that keeps the market liquid while still collecting. Italy taxes at a flat 26% but spares small transactions. Against that field, India’s regime looks less like a tool to raise money and more like a tool to choke the activity it pretends to tax.

The Great Exodus

In the months after the 1% TDS took effect, domestic exchanges lost the overwhelming majority of their volumes. Esya’s four-month post-TDS measurement put the drop at around 81%, with later cuts of the data running as high as 97% and an estimated 3 to 5 million users decamped to foreign platforms.

An FY25 analysis by compliance platform KoinX, covering more than 670,000 users, found that roughly 72% of Indian crypto volume had shifted offshore, that is, the proportion that moved. Separately, the exchanges’ own data presented to Parliament in May 2026 put the current offshore share of the Indian spot market near 90%. The trend keeps compounding: by industry estimates Indians traded on the order of ₹4.9 lakh crore (~$56–57 billion) on offshore platforms in the year to October 2025, a sharp year-on-year jump, and the government’s January 2024 move to block nine foreign exchanges backfired, traffic to the blocked venues reportedly rose as users switched on VPNs.

Now the irony that should make a finance ministry wince. A tax built to widen the net and create a paper trail has produced near-total blindness instead. A late-2025 academic estimate put the uncollected tax from offshore trading at roughly ₹11,000 crore — implying offshore turnover of around ₹11 lakh crore, squaring neatly with that 90% figure. On top of that sits an estimated capital-gains shortfall that pushes total foregone revenue into the tens of thousands of crores (that broader number is a derived estimate, and should be flagged as such rather than reported as hard fact). Meanwhile, the hobbled domestic exchanges remitted just about ₹158 crore and ₹180 crore in two recent years. One widely cited five-year projection, from the policy think-tank Esya Centre, puts uncollected tax on current trends at around ₹17,700 crore.

Read it back slowly: a policy sold as a way to tax crypto has instead lost track of nine-tenths of it, surrendered tens of thousands of crores, and left the small retail buyer at home — the one who couldn’t or wouldn’t flee — quietly eating the premium. The state didn’t catch the whales. It only managed to tax the minnows who stayed.

Parliament is now asking the same question

This stopped being abstract in May 2026, when Parliament’s Standing Committee on Finance, chaired by BJP MP Bhartruhari Mahtab, under the banner “A Study on Virtual Digital Assets and the Way Forward,” summoned ZebPay, Binance, and WazirX to testify on virtual digital assets and “the way forward.”

It was one of the most formal sit-downs between India’s lawmakers and the crypto industry yet. The exchanges came armed with their own trading data, showing that the 30%-plus-1% regime had pushed over 90% of Indian retail volume onto unregulated offshore venues, and made the blunt point that the tax never stopped Indians from trading crypto; it only changed where they do it. The people who built the policy are now, on the record, being asked why it did the opposite of what it promised.

The RBI’s stance, and why its own logic turns against it

It would be lazy to indict the regulator without granting its real concerns, which are serious. The RBI fears that letting private dollar-stablecoins run wild could quietly “dollarise” the economy, drain reserves, and blunt its control over the rupee. Its push for an official digital rupee reflects a genuine preference for sovereign money over private global tokens. Opening the capital account fully really does carry risk.

But here is the twist that should stop a policymaker mid-sentence: the tax fails on the RBI’s own terms. The 1% levy did not reduce Indians’ appetite for dollars, it shoved that entire appetite onto offshore stablecoin rails where the RBI can see nothing and control nothing. A demand it could once watch and regulate at home has been converted into an invisible river flowing through foreign apps.

If the fear was dollarisation, the policy may have made it worse, not better: it has handed away the very control it was built to protect.

4. The alternates for users

There’s no clean, legal, zero-premium route under today’s rules, but disciplined buyers can shrink the gap. Treat the box below as a survival guide for the small user, not the moral of the story; in a piece about a state failing its citizens, “here’s how you personally tunnel under the wall” can’t be the headline.

Survival tactics for Indian users

- Compare on-ramps relentlessly. Third-party ramps such as Ramp Network, Transak, MoonPay, Banxa, and Paybis often yield effective rates in the ₹97–100 band for UPI/bank transfers, especially on larger tickets.

- Use the LRS for large flows. For amounts above ₹10–20 lakh, a formal bank remittance abroad followed by purchase on a global platform can deliver closer-to-spot economics, at the cost of paperwork and TCS.

- Time and split. Buy during low-volatility windows, spread orders across multiple ramps, and route directly to a non-custodial wallet.

- Keep clear, meticulous records for tax compliance.

- Treat the structural ~2–4% as a fixed cost of operating from India rather than chasing illusory zero-premium routes.

But the offshore escape hatch is closing fast. Under the OECD’s Crypto-Asset Reporting Framework (CARF), which India is set to implement from April 2027, foreign exchanges will be required to automatically share user transaction data with Indian authorities, stripping offshore trading of the anonymity that made it attractive.

Millions who migrated to dodge the 1% TDS could face retroactive demands for unpaid 30% capital-gains tax, accumulated interest, and penalties of 50–200% under Section 270A. The window in which offshore activity stays invisible is short. That makes rationalising the tax code before the deadline a matter of urgency rather than ideology, both for the users exposed to back-demands and for a state that would rather collect on a regulated onshore market than chase millions of small offenders.

What policy made, policy can unmake

As of June 2026, the premium shows no sign of disappearing absent real regulatory evolution, clearer stablecoin licensing, deeper banking integration, or calibrated easing of capital-flow rules for digital assets. But the remedy is not mysterious, and analysts are close to unanimous on it.

Cut the 1% transaction tax to 0.01%, the same rate equities already pay, and the professional traders come back, liquidity returns, and the self-inflicted half of the premium collapses. Modelling suggests around 82% of users would return to compliant Indian platforms, plausibly handing the government ₹9,000–18,000 crore over five years by simply recapturing what it currently can’t see. Let losses on one coin offset gains on another, and force the “instant buy” screens to show the spread they currently bury, and you fix the resentment and the opacity in one move.

Strip it all back and the two halves snap together. The honest premium is the price of a wall India chose to build. The exodus, the dead liquidity, and the tens of thousands of crores left on the table are the price of a hole India shot in its own foot, and never patched. The overcharge on a student’s ₹10,000 and the billions vanishing offshore are the same policy, seen from opposite ends. With CARF and a live parliamentary inquiry both bearing down on 2027, the question is no longer whether India revisits this regime, but whether it moves before the bill comes due.

For the ordinary buyer, the advice is unglamorous: compare relentlessly, route big sums formally, and treat the honest slice of the premium as the cost of operating inside India’s walls. For the people who write the rules, the lesson is sharper. A tax built to capture crypto has instead lost most of it, and may have bargained away the very monetary control it was meant to defend. India isn’t failing to tax a borderless market. It is paying to chase that market out the door, and charging its own citizens for the privilege of watching it leave.