Key Highlights

- ETFs have absorbed $142 billion (7% of BTC supply) and slashed volatility by 55%, turning Bitcoin into “sovereign-grade collateral.”

- A massive “Honeypot Risk” has emerged. Coinbase Custody now holds ~85% of US ETF assets, recentralizing a decentralized asset class.

- The 2025 GENIUS Act has effectively banned non-banks from paying yield, handing the “digital dollar” market to traditional banks like JPMorgan.

As we start the year 2026, the question regarding institutional capital in cryptocurrency has shifted from “if” to “how much.” The approval and subsequent explosion of spot cryptocurrency Exchange Traded Funds (ETFs) in the United States have catalyzed a structural transformation within the digital asset market without precedent. As of January 2026, spot Bitcoin ETFs alone have attracted over $142 billion in assets under management (AUM), according to Dune Analytics, absorbing nearly 7% of the total circulating Bitcoin supply.

This influx of capital has done more than just push prices upward; it has fundamentally rewired the market’s plumbing. The narrative of the “Wild West” is fading, replaced by a regulated, high-speed, and heavily surveilled financial layer that looks less like the Cypherpunk Dream of 2009 and more like a digitized extension of Wall Street. With Morgan Stanley filing just this week to launch proprietary Bitcoin and Solana ETFs, the integration is deepening.

However, this maturation comes at a cost. While traditional finance’s (TradFi’s) entry has provided liquidity and legitimacy, it has also introduced systemic centralization risks and altered the governance dynamics of decentralized networks. For the crypto purist, the landscape of 2026 presents a paradox: the technology is winning, but are the ethos surviving?

The ETF tsunami: From access to “yield”

The trajectory of crypto ETFs has evolved rapidly from simple price exposure to complex yield-bearing instruments. The initial wave of Bitcoin ETFs in 2024 established the regulatory beachhead, but the developments during 2025, especially after Donald Trump’s presidency in the U.S., ushered in the era of “total return” products.

Bitcoin as sovereign-grade collateral

The “digital gold” thesis has been empirically validated by the sheer scale of ETF inflows. Analysts liken the current trajectory to the “Year Three” acceleration of the Gold ETF (GLD) post-2004. With major wirehouses—including Wells Fargo, Merrill, and now actively Morgan Stanley—incorporating Bitcoin into discretionary portfolios, the asset has cleared the due diligence windows required by pension funds and endowments.

The impact is measurable in the dampening of volatility. In the pre-ETF era (2020 to 2023), Bitcoin’s average daily volatility hovered around 4.2%. By 2025, that figure dropped to 1.8%. The persistent bid from passive flows and model-driven rebalancing acts as a shock absorber, smoothing out the violent drawdowns that once defined the asset class. Bitcoin is behaving less like a tech stock and more like sovereign-grade collateral.

The Institutionalization Trajectory (2026 Outlook)

| Metric | Current Status (Jan 2026) | Projected Status (Year-End 2026) | Primary Driver |

| Total ETF AUM | ~$142 Billion | $180 – $220 Billion | Model portfolio inclusion by major wirehouses |

| Bitcoin Supply Held | ~7.0% | >10.0% | Net inflows outpacing new issuance and exchange withdrawals |

| Institutional Adoption | ~60% of surveyed firms | >80% planning allocation | Hedging currency devaluation and portfolio diversification |

| Distribution Access | Major Wirehouses (Morgan Stanley, Merrill) | Pension Funds & Sovereigns | Regulatory clarity and “Year 3” due diligence clearance |

The yield revolution: Ethereum and Solana

While Bitcoin ETFs trade on scarcity, the frontier for 2026 is yield. The initial Ethereum ETFs launched in 2025 underperformed relative to Bitcoin. This was largely because they forced investors to hold a non-yielding derivative of a yielding asset. That friction is now disappearing.

BlackRock’s recent filing for the iShares Staked Ethereum Trust ETF signals the start of the “Yield Era.” By incorporating staking—where the underlying ETH is bonded to the network to secure consensus—these ETFs transform into digital bonds.

Simultaneously, Solana has emerged as the third pillar of the ETF market, with assets surpassing $1 billion in January 2026. Bitwise has captured a dominant 67% market share in this vertical specifically by offering staking rewards, proving that institutional investors prefer products that capture the full economic value of the underlying network.

Structural Market Changes (Pre- vs. Post-ETF)

| Metric | Pre-ETF Era (2020-2023) | Post-ETF Era (2024-2025) | Structural Implication |

| Average Daily Volatility | 4.2% | 1.8% | Reduced speculative premium; higher Sharpe ratio potential. |

| Maximum Drawdown | -77% | -25% | Presence of steady “buy-the-dip” passive flows. |

| Extreme Price Swings (>20% in 24h) | Common | Rare | Deeper order books absorb liquidation cascades. |

| Trading Volume Share (US Hours) | 41.4% | 57.3% | Market activity aligns with NYSE/Nasdaq sessions. |

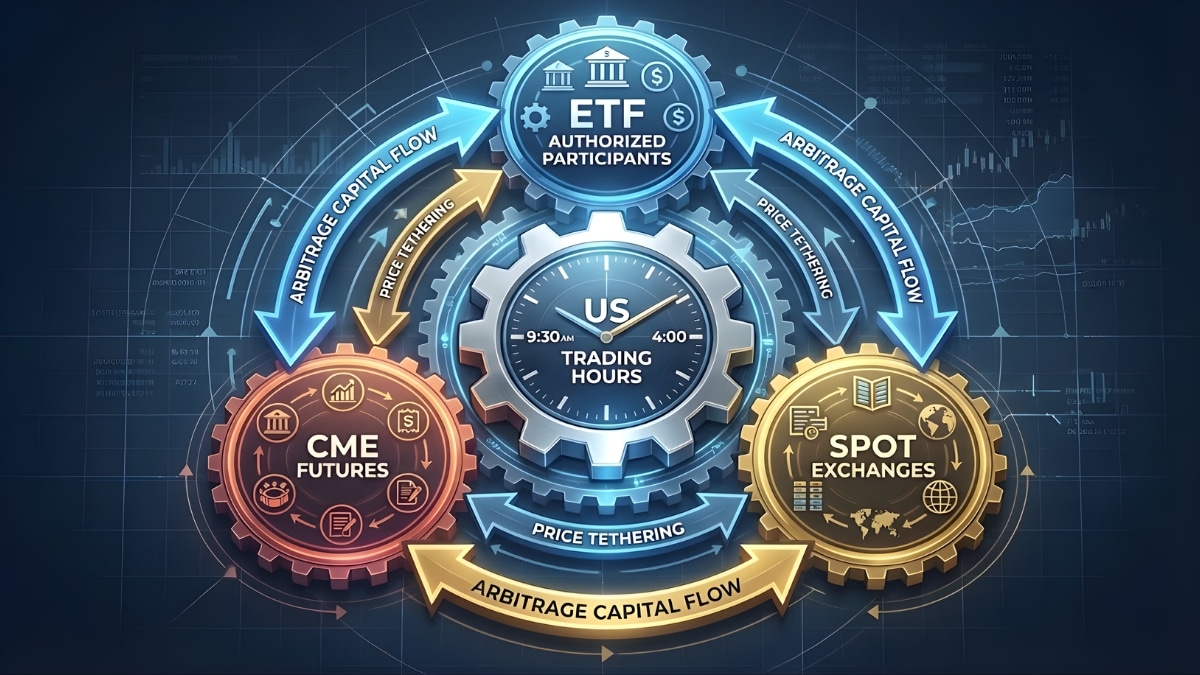

Market structure: The liquidity flywheel vs. The honeypot

TradFi has revolutionized the backend plumbing of crypto markets. The fragmented, opaque liquidity of offshore exchanges is being replaced by a sophisticated “liquidity flywheel” connecting ETFs, futures markets, and regulated custodians.

The basis trade and price anchoring

The ETF boom has cemented the “basis trade”—selling futures while buying the spot asset to capture the spread—as a primary strategy for hedge funds. Because most ETFs and CME futures settle to the same reference rates, the risk of price divergence is minimal. This has driven massive volumes into CME Bitcoin Futures, tethering spot prices to the regulated futures market.

Consequently, price discovery has shifted time zones. In 2021, trading volume was evenly split between Asian, European, and US hours. As noted by Chronicle Journal, US market hours (9:30 AM–4:00 PM EST) accounted for 57.3% of global Bitcoin trading volume in 2025. The marginal buyer is no longer a retail trader in Seoul, but an algorithm in New York executing a rebalancing order.

The Coinbase dilemma

This efficiency hides a glaring systemic risk: custody concentration. Coinbase Custody currently safeguards approximately 85% of all ETF-held Bitcoin in the US, which was once over 90% as reported by The Crypto Times in February 2024. While the firm employs institutional-grade security, this creates a “honeypot” risk of unprecedented magnitude.

European regulators, particularly the European Systemic Risk Board (ESRB), have flagged this as a critical financial stability risk. A single operational failure or regulatory action against Coinbase could paralyze the majority of US institutional crypto wealth. Unlike the decentralized ideal where risk is distributed across thousands of private keys, the ETF era has re-centralized risk into a handful of regulated vaults.

The custody landscape evolution

| Custody Model | Key Players | Risk Profile | Target Client |

| Crypto-Native Monoline | Coinbase, BitGo, Anchorage | Tech-forward, high concentration risk | Early institutional adopters, ETFs |

| Global Custodian Bank | BNY Mellon, State Street, Zand | Regulatory armor, capital inefficient (pre-SAB 121 repeal) | Pensions, Sovereigns, Conservative wealth |

| Self-Custody (Multi-Sig) | Unchained, Casa | Operational complexity, sovereign control | High net worth individuals, Family offices |

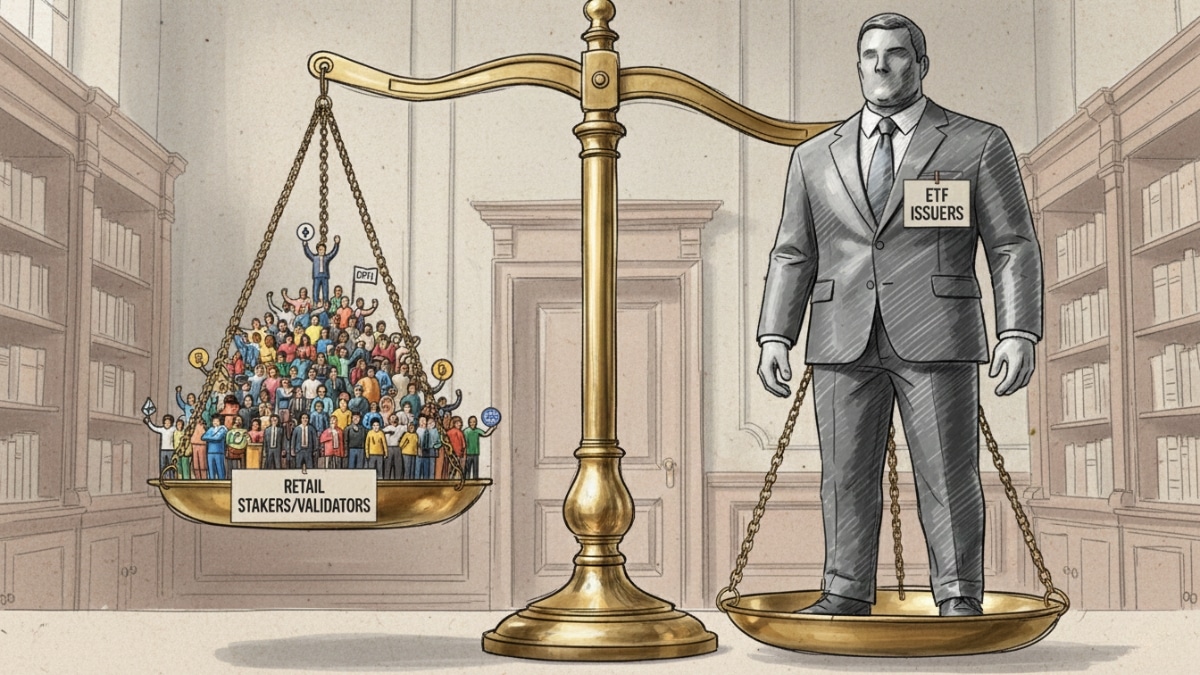

The governance paradox: Passive giants in active protocols

Perhaps the most insidious impact of the ETF-era is the transfer of governance power. In Proof-of-Stake (PoS) blockchain networks like Ethereum and Solana, token ownership equates to voting rights. As ETFs amass huge stockpiles of tokens, voting power is effectively centralized in the hands of issuers who are structurally disincentivized to use it.

The silent takeover

Asset managers like BlackRock generally adhere to a policy of “non-intervention” regarding protocol governance. Prospectuses often state that issuers will “permanently and irrevocably abandon” incidental rights, such as those arising from forks or airdrops.

In a governance-weighted system, abstention is a form of action. It leaves networks vulnerable to minority rule, where a small coalition of active voters can pass proposals because the massive voting bloc of ETF-held tokens remains dormant. If these giants do decide to vote, they become de facto regulators of the protocol.

Validator centralization and censorship

The mechanics of staking ETFs exacerbate this issue. Issuers do not run their own validators; they contract with third-party providers like Coinbase or Anchorage. This concentrates the network’s validation power into a few regulated US entities.

If a US regulator were to order these custodians to censor transactions from sanctioned addresses at the validator level, a significant percentage of the Ethereum network would be legally compelled to comply. This “spillover risk” threatens the censorship resistance that gives public blockchains their value proposition. The network effectively becomes a permissioned environment during US trading hours.

The GENIUS Act and the battle for the digital dollar

While ETFs reshape investing, the Guiding and Establishing National Innovation for U.S. Stablecoins Act (GENIUS Act), signed into law in July 2025, is reshaping payments. This legislation has ended the “move fast and break things” era for stablecoins, ushering in a federally supervised digital monetary system.

Banks vs. Non-banks

A cornerstone of the GENIUS Act is the prohibition on non-bank stablecoin issuers paying interest to end-users. This clause was a victory for the banking lobby, designed to prevent stablecoins like USDC or PayPal’s PYUSD from competing directly with interest-bearing bank deposits.

This has created a two-tiered system. Banks can issue “tokenized deposits” that pay yield, while fintechs are relegated to issuing “digital cash.” In response, banks like JPMorgan and Citi are aggressively expanding their programmable money capabilities, aiming to capture high-value institutional settlement flows.

The “TradeFi” evolution

This regulatory clarity has given rise to “TradeFi”—decentralized trade finance. Tether, for example, has pivoted toward financing commodity trading (oil, copper) using USDT, bypassing traditional banking rails entirely. Meanwhile, PayPal’s PYUSD is integrating deeply into merchant networks, competing on velocity rather than yield.

However, the legal moat around the banking system remains strong. The denial of a Fed Master Account to Custodia Bank, upheld by courts in 2025, signaled that while crypto assets are welcome, they must live inside the existing banking oligopoly, not alongside it in novel reserve-banking models.

Real World Assets (RWAs): Wall Street moving on-chain

If ETFs bring crypto to Wall Street, then Real World Asset (RWA) tokenization brings Wall Street to crypto. This sector that grew to a $33 billion market by mid-2025, is largely driven by the demand for on-chain yield derived from US Treasuries, which now sits near $20 billion, excluding stablecoins.

BlackRock’s BUIDL: The new standard

The BlackRock USD Institutional Digital Liquidity Fund (BUIDL) has become the bellwether for this sector. By tokenizing shares of a fund holding cash and Treasuries, BlackRock created a product that offers the safety of sovereign debt with the composability of a crypto token. BUIDL is now widely used as collateral in trading and treasury management for crypto-native firms.

The bifurcation of DeFi

Crucially, BUIDL represents a “permissioned” pivot. Unlike DAI or USDT, BUIDL tokens can only be held by whitelisted wallets that have passed strict know-your-customer (KYC) checks. This is driving a “great bifurcation” in decentralized finance (DeFi).

One tier is “Institutional DeFi”—compliant, permissioned, and liquid, dominated by products like BUIDL and Franklin Templeton’s BENJI. The other is “Permissionless DeFi”—the original, anonymous ecosystem. As institutional capital migrates to the regulated tier, the permissionless sector risks becoming liquidity-starved and marginalized.

To sum up

Is TradFi really helping crypto? The answer depends on the metric of success.

If the metric is price appreciation, liquidity, and stability, the answer is an unequivocal yes. The ETF tsunami has unlocked hundreds of billions in capital, dampened volatility, and integrated digital assets into standard global portfolios. The GENIUS Act provided the legal certainty required for mass adoption, and RWA tokenization is unlocking trillions in illiquid value.

However, if the metric is decentralization, censorship resistance, and financial sovereignty, the verdict is far more ominous. Custody has centralized into a “honeypot” of regulated entities. Governance rights are drifting toward passive asset managers. Innovation is bifurcating into “white market” permissioned zones and “grey market” permissionless zones.

TradFi has not killed crypto; it has domesticated it. The chaotic, revolutionary potential of the asset class is being paved over by the safety and surveillance of regulated finance. In 2026, crypto is no longer an alternative to the financial system; it is rapidly becoming the new operating system for it. The challenge for the industry moving forward will be preserving the core ethos of decentralization within a market increasingly owned by the very intermediaries it was built to disintermediate.

The 2026 landscape at a glance

| Category | Key Metric/Status |

| Bitcoin ETF AUM | ~$142 Billion (Jan 2026) |

| Ethereum ETF Flows | ~$18 Billion ( Jan 2025) |

| Solana ETF AUM | ~$1.1 Billion (Jan 2026) |

| Market Volatility | Down 55% (Pre- vs Post-ETF) |

| Custody Concentration | Coinbase holds ~85% of ETF assets |

| RWA Market Size | ~$20 Billion ( Jan 2026) |

| Stablecoin Regulation | GENIUS Act prohibits interest to end-users |

| Correlation (BTC/S&P) | 0.4 (Medium) |

Disclaimer:

The Crypto Times publishes news, analysis, and educational content for informational purposes only. We do not offer financial, investment, legal, or trading advice of any kind. All content on our website is intended to be neutral and fact-based. Readers should always do their own research, consult with licensed professionals, and evaluate risks independently.

The Crypto Times does not endorse or recommend any specific cryptocurrencies, tokens, projects, financial products, or investment strategies. We do not accept legal liability for any financial losses incurred as a result of reliance on information published by us.