Bitcoin’s options market has stopped panicking, but it is not betting on a bounce. With BTC trading around $62,630, deep below its 100- and 200-day moving averages and testing the February lows that mark its most important support, Glassnode’s latest options data shows fear gauges cooling even as traders keep one hand on the exits.

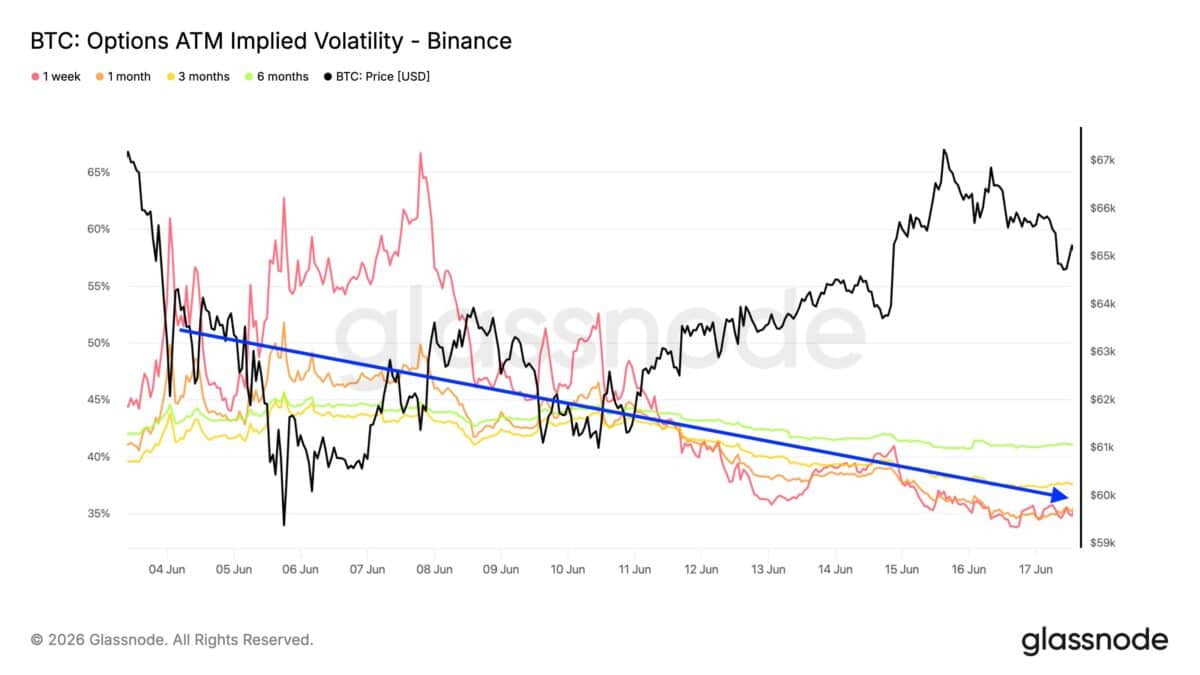

According to Glassnode’s BTC Options Weekly, implied volatility has eased sharply despite price probing the lows. One-week implied volatility has fallen from 60% to 35%, with the rest of the term structure drifting lower, the market is pricing meaningfully less uncertainty than it was two weeks ago.

Demand for downside protection has normalized in step. The one-week 25-delta skew, a gauge of how much more traders are paying for puts over calls, has retreated from the roughly 30% extreme reached during the June selloff back to about 15%. In Glassnode’s reading, the scramble for crash insurance that defined the recent drop has largely subsided.

But the Tape Stays Defensive

Calmer is not the same as bullish. The data notes that the flow remains tilted toward protection: over the past seven days, put buying led taker activity at 28.1% of premium traded, ahead of call buying at 24.1%. Its skew index ratio, which weighs upside against downside pricing, shows near-term options still favoring downside exposure, with calls continuing to lose ground.

In other words, the market has settled into caution rather than confidence. The acute fear has drained out, but positioning still leans toward further weakness rather than a recovery off support.

The $62,000 Gamma Trap

The sharpest risk Glassnode flags is structural, and Bitcoin has just walked into it. The largest cluster of negative, or short, gamma sits at $62,000, where about $1.8 billion is concentrated, and with the spot now around $62,630, the price is sitting directly on that shelf. Short-gamma positioning forces dealers to hedge in the same direction as the move, selling into falling prices, which can amplify a decline rather than cushion it.

That makes the current level a potential accelerant rather than a floor. Glassnode warns that a move lower could speed up a retest of $60,000, the February low and a key psychological level, where a small pocket of long gamma may finally help contain volatility. With the price already at the cluster and well below its 100-day EMA near $76,900, the $60,000 mark is the one to watch for whether a slide becomes orderly or disorderly.

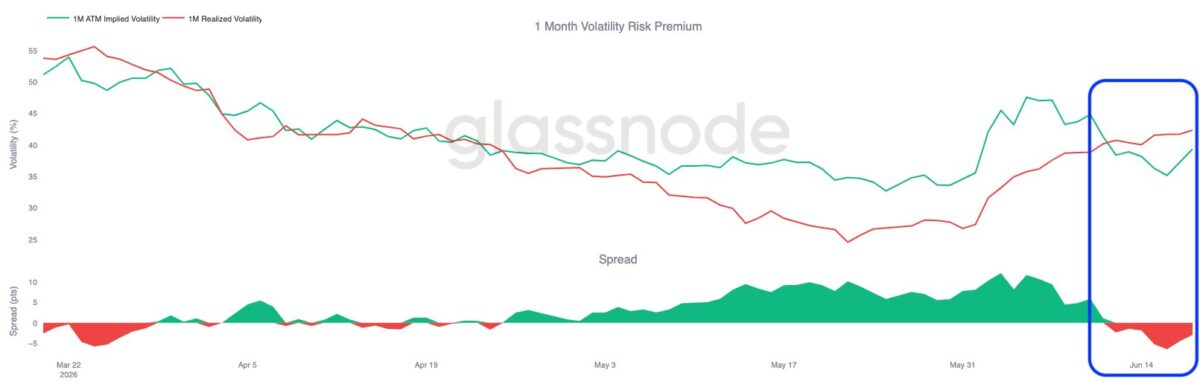

Options Are Underpricing the Swings

A subtler signal sits underneath: the volatility risk premium has turned negative. One-month implied volatility, near 39%, has dropped below realized volatility, which has climbed above 42%. Bitcoin’s actual price swings are now exceeding what the options market is pricing for them.

That inversion is unusual and cuts two ways. It suggests hedges are relatively cheap versus how much the asset is actually moving, and historically such gaps can precede a repricing higher in implied volatility if the market is caught underprepared for the next move.

A Macro Vise

The defensive tilt is hard to separate from the backdrop. Bitcoin is sitting on support at the same moment the rate-cut hopes underpinning risk assets have evaporated. The Federal Reserve’s hawkish first meeting under Kevin Warsh removed its easing bias and pushed expected cuts into 2027, and Bitcoin slid toward $60,000 in the aftermath as a firmer dollar and higher yields sapped appetite for non-yielding assets.

That macro pressure is precisely what the options positioning reflects: traders are not pricing a panic, but they are unwilling to fade the downside while the Fed offers no relief. The confluence, i.e. technical support at the February lows, a short-gamma shelf at $62,000, and a no-cuts macro overhang, leaves Bitcoin balanced on a narrow ledge.

Glassnode’s summary captures it bluntly: defensive positioning persists near key support. Whether that support holds may come down to which gives way first: the macro or the gamma.