The year 2026 marks a monumental paradigm shift for the cryptocurrency industry, and no digital asset exemplifies this transformation quite like XRP. After years of operating under a cloud of regulatory uncertainty, Ripple and the broader XRP ecosystem have transitioned from speculative retail investments into fully integrated, institutional-grade financial infrastructure.

Today, the conversation surrounding XRP is no longer dominated by courtroom dramas. Instead, the focus has shifted to national bank charters, enterprise-grade stablecoins, real-world asset (RWA) tokenization, and the dawn of artificial intelligence-driven commerce.

What Is XRP and Why Does It Matter in 2026?

Before diving into the details, here is a quick primer for those new to XRP.

XRP is a digital currency created by Ripple Labs, a U.S.-based financial technology company. Unlike Bitcoin, which was designed as a decentralized store of value, XRP was built specifically to move money across borders quickly and cheaply. Think of it as a digital bridge currency—a tool that allows banks and payment companies to transfer value between different currencies in seconds, rather than the days it can take through traditional banking systems.

Ripple Labs created XRP and continues to develop the infrastructure around it, though XRP itself trades freely on public markets and is held by millions of individual and institutional investors worldwide.

2026 is a significant year for XRP for one central reason: after five years of legal uncertainty, regulatory clarity has finally arrived. The outcome has unlocked access for banks, pension funds, and major financial institutions that were previously unable to touch the asset. This guide breaks down what that means for the price, the technology, and the future of XRP.

Price Prediction and Market Dynamics in 2026

Despite profound fundamental improvements across the Ripple ecosystem, the spot price of XRP in March 2026 has remained heavily constrained by macroeconomic headwinds.

As of early April 2026, XRP is trading in a highly reactive, sentiment-driven range between $1.30 and $1.36. This is 65% retracement from its all-time high of $3.84, marked in January 2018, and notably lower than its secondary peak of $2.42 achieved in January 2026.

Why is the price lower than many expected?

The answer lies primarily in macroeconomic conditions outside of crypto.

In March 2026, the broader cryptocurrency market experienced significant capital flight triggered by global geopolitical tensions, escalating military pressure in the Middle East, and sweeping new trade tariffs introduced by the Donald Trump administration.

These events triggered a broad “risk-off” environment—meaning investors across stocks, crypto, and other assets pulled back from anything perceived as volatile and moved into safer holdings like cash and government bonds.

The Crypto Fear & Greed Index, a widely followed sentiment gauge that measures investor mood on a scale of 0 (extreme fear) to 100 (extreme greed), fell to just 13, indicating extreme fear. This kind of market-wide pessimism suppresses prices across all cryptocurrencies, including XRP, regardless of their underlying fundamentals.

One of the asset’s pricing challenges is also the massive concentration of overhead supply, meaning there are a large number of investors who bought XRP at those levels and may sell when the price returns there, creating resistance to upward movement. Market analysts note that approximately 4 billion XRP is currently compressed into a narrow 40-cent price band, creating massive resistance zones between $1.78 and $2.30. Breaking through these levels will require sustained institutional participation rather than retail momentum alone.

XRP ETFs: A New Way to Invest

One of the most significant developments of 2026 is the availability of XRP Exchange-Traded Funds (ETFs). These are investment products that track XRP’s price and can be bought and sold on traditional stock exchanges, just like shares in a company. This allows investors to gain exposure to XRP without needing to set up a crypto wallet or use a crypto exchange.

XRP ETFs crossed the $1 billion Assets Under Management (AUM) milestone earlier in 2026. However, following the market downturn in late March, it began experiencing muted activity and net outflows. On certain days in late March, all five available XRP ETF products posted zero daily inflows, reflecting the broader risk-off sentiment.

Despite these short-term flows, massive institutional players have already established their baseline positions. Goldman Sachs, for example, emerged as the single largest disclosed institutional holder, building a massive $153.8 million position across four different XRP ETFs.

2026 XRP Price Forecasts

Market strategists remain divided on the timeline for XRP’s next major breakout. While the fundamental foundation of the asset is demonstrably stronger than it was in previous years, future price appreciation depends heavily on global liquidity conditions and the sustained adoption of Ripple’s payment infrastructure.

| Originating Entity | 2026 Price Target | Underlying Catalyst and Analytical Rationale |

|---|---|---|

| Finance Magnates | $0.80 – $2.00 | Represents an indicative trading range under stable, moderate macroeconomic conditions. |

| Standard Chartered | $2.80 | Downward revision from a previous $8.00 call; relies heavily on sustained ETF adoption. |

| LVRG Research | $4.00 – $5.00 | Base outcome driven by structural narratives, legal clarity, and enterprise adoption. |

| Motley Fool | $10.00 | Relies on ETF inflows creating a permanent demand base that isolates the asset from retail volatility. |

Regulatory Renaissance: SEC Lawsuit End and Commodity Status

In December 2020, the U.S. Securities and Exchange Commission (SEC) — the federal agency that regulates financial markets — sued Ripple Labs, alleging that XRP was an unregistered security.

In simple terms, the SEC argued that buying XRP was similar to buying a share in a company, which requires strict regulatory compliance.

This lawsuit created enormous uncertainty for XRP. Consequently, many U.S. exchanges delisted the token, institutional investors avoided it, and its price significantly underperformed compared to Bitcoin and Ethereum for years.

That legal cloud has now fully lifted.

The Conclusion of the SEC Lawsuit

The multi-year legal battle between Ripple Labs and the SEC formally concluded in August 2025. The final resolution required Ripple to pay a $125 million civil penalty and accept an injunction against future unregistered institutional sales.

Most importantly for the market, the settlement firmly upheld the ruling that XRP is not a security when sold to retail investors on public cryptocurrency exchanges. While rumors occasionally circulate regarding prolonged appeals extending into late 2026, the consensus among legal experts and institutional investors is that the core regulatory risk has been successfully eliminated.

XRP Officially Classified as a Digital Commodity

The regulatory progress did not stop there. Following the lawsuit’s conclusion, federal regulators took historic steps to clarify the legal taxonomy of digital assets. On March 17, 2026, the SEC and the Commodity Futures Trading Commission (CFTC)—the federal agency that oversees commodity markets like oil, gold, and now certain cryptocurrencies—issued a landmark comprehensive joint interpretive framework. This framework officially classified XRP, alongside 15 other tokens, including Bitcoin and Ether, as a digital commodity.

What does “digital commodity” mean in practice?

It means XRP is now treated similarly to gold or oil in legal terms — an asset that can be freely bought, sold, and held by institutions without triggering securities law compliance requirements.

This single classification change paved the way for sovereign wealth funds, pension portfolios, and major banks to hold and interact with the token without violating internal compliance mandates.

The GENIUS Act and the CLARITY Act

Two major pieces of legislation have defined the 2026 crypto landscape.

First, the GENIUS Act (Guiding and Establishing National Innovation for U.S. Stablecoins), signed into law in July 2025. It created the first federal rulebook for stablecoins—digital currencies pegged to the value of a real-world asset like the U.S. dollar. This gave companies like Ripple a clear legal pathway to operate dollar-backed digital currencies.

Second, the CLARITY Act (Digital Asset Market Clarity Act) passed the House of Representatives 294-134 in July 2025 with strong bipartisan support and cleared the Senate Agriculture Committee in January 2026. This law draws the boundary between which digital assets are regulated by the SEC and which fall under the CFTC. For XRP, its passage cemented its status as a CFTC-regulated digital commodity rather than an SEC-regulated security.

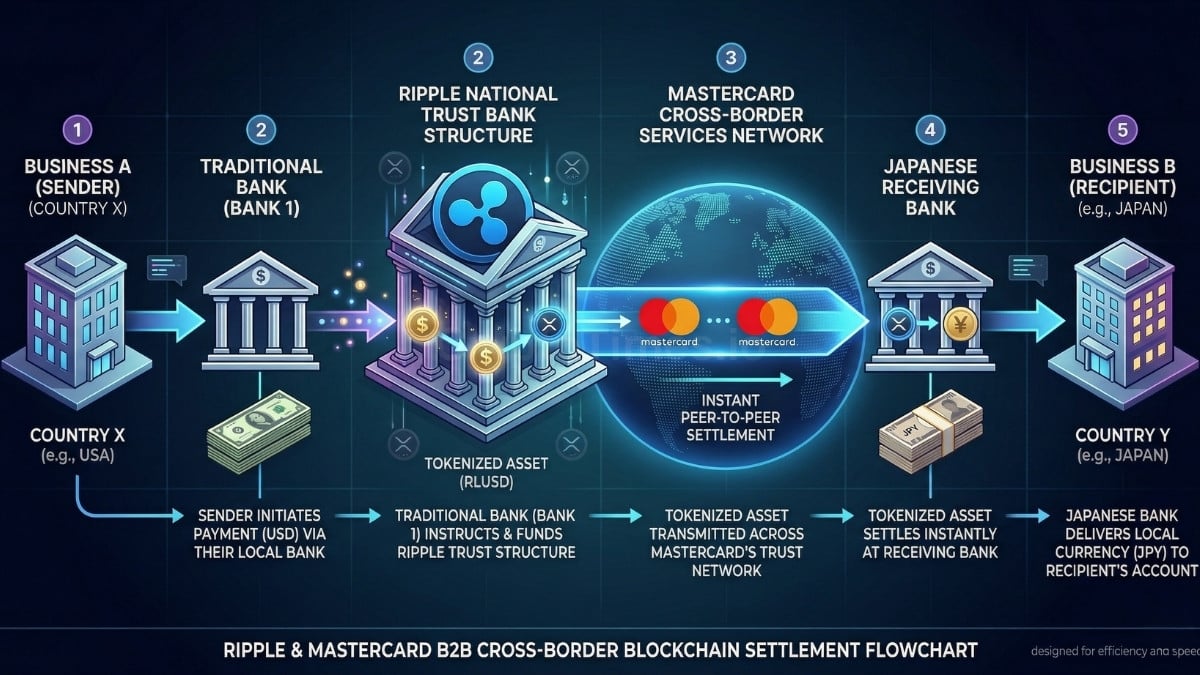

Institutional Adoption and the Ripple National Trust Bank

With regulatory barriers removed, 2026 has witnessed unprecedented integration between Ripple’s infrastructure and the traditional banking system.

The OCC National Trust Bank Charter

A trust bank is a federally regulated financial institution that can hold and manage assets on behalf of clients. Receiving a national trust bank charter from the U.S. government means Ripple is no longer just a software company — it is now a regulated financial intermediary, similar in legal standing to a traditional bank.

In December 2025, the Office of the Comptroller of the Currency (OCC)—the federal agency that charters and supervises national banks—granted conditional approval for the creation of the Ripple National Trust Bank (RNTB). Ripple was one of several major crypto firms, including Circle, BitGo, Fidelity and Paxos, to receive this approval.

This federal charter allows Ripple to operate as an uninsured national trust bank across all fifty states under a single federal regulator, bypassing the highly fragmented state-by-state money transmitter licensing process.

Through this charter, the Ripple National Trust Bank can provide enterprise-grade digital asset custody, execute institutional payment settlements, and manage the underlying fiat reserves for its stablecoin operations. Ripple operates under a dual regulatory structure—overseen at the state level by the New York Department of Financial Services (NYDFS) and at the federal level by the OCC.

The Mastercard Crypto Partner Program

Ripple’s institutional momentum was further validated on March 11, 2026, when Mastercard officially launched its global Crypto Partner Program. Ripple joined this elite initiative alongside over 85 digital asset firms, including Binance, Circle, and Paxos.

The program is designed to integrate blockchain-based payment tools directly into Mastercard’s massive global infrastructure, which processes over $9 trillion in annual payments across 200 countries. Ripple’s inclusion focuses specifically on utilizing blockchain technology for high-friction enterprise use cases, such as business-to-business (B2B) settlements, global payouts, and cross-border money movement.

The Rise of RLUSD and Its Ecosystem Impact

RLUSD is a compliant, fiat-backed stablecoin issued by Ripple. A stablecoin is a type of cryptocurrency designed to maintain a fixed value—usually pegged 1:1 to the U.S. dollar. Unlike XRP, whose price fluctuates with market conditions, one RLUSD is always worth one U.S. dollar, backed by U.S. Treasury bills and cash equivalents. This makes it attractive for businesses that need predictable value transfer.

Launched to meet enterprise demand for stable, predictable value transfer, RLUSD rapidly surged to a $1.56 billion market capitalization by March 2026. Currently, 82% of the RLUSD supply circulates on the Ethereum network, taking advantage of its massive decentralized finance ecosystem, while 18% operates directly on the native XRP Ledger.

In early 2026, Ripple enhanced this interoperability by integrating Wormhole’s Native Token Transfers (NTT) standard. This advanced architecture allows RLUSD to move natively across different blockchain networks—including high-speed Layer 2 environments like Base and Optimism—without relying on vulnerable wrapped tokens or synthetic assets.

In late March 2026, Ripple burned—permanently destroyed—over 35 million RLUSD tokens, including a 26 million token burn on Ethereum. This is standard treasury management: when enterprise clients redeem their RLUSD for actual U.S. dollars, Ripple destroys the corresponding digital tokens to ensure the total supply always matches the real-world reserves backing it.

The “Utility Gap”: Does RLUSD Compete With XRP?

This is one of the most important questions for anyone considering XRP as an investment in 2026. In March 2026, the XRP Ledger processed a record 19 million weekly transactions. However, the share of those transactions using XRP specifically for cross-border payments declined by 80%. The reason: financial institutions prefer the price stability of RLUSD for moving value across borders rather than using XRP whose price can fluctuate significantly.

This dynamic—where Ripple’s own stablecoin captures much of the payment utility that was originally intended for XRP — is what analysts call the “utility gap.” It does not mean XRP is worthless, but it does mean investors should understand that RLUSD and XRP serve increasingly different roles within the same ecosystem. RLUSD is the tool of choice for enterprise payments; XRP is increasingly positioned as a reserve asset, a DeFi liquidity token, and a settlement layer for real-world asset tokenization.

Real-World Asset (RWA) Tokenization and Privacy Protocols

Real-world asset (RWA) tokenization refers to the process of creating a digital representation of a physical or traditional financial asset — such as a U.S. Treasury bill, a piece of real estate, or a corporate bond — on a blockchain. Instead of holding a paper certificate or relying on intermediaries, investors hold a digital token that represents ownership of the underlying asset, which can be transferred instantly and globally.

Beyond payments, the XRP Ledger has positioned itself as a premier destination for the tokenization of real-world assets (RWAs). By bringing traditional financial instruments like Treasury bills, private credit, and real estate on-chain, Ripple is capturing a significant share of a market projected to reach multiple trillions of dollars.

The XRPL offers institutional-grade features out of the box, eliminating the need to write complex, vulnerable smart contracts. The network supports native compliance checks, automated investor credential verification, and on-chain asset freezing, settling transactions in just 3 to 5 seconds.

Broad data tracking platforms like DeFiLlama estimate the network’s RWA valuation at approximately $61.86 million. However, specialized tokenization trackers like RWA.xyz place the figure much higher, estimating the total tokenized value on the ledger between $461 million and $570 million.

| RWA Platform / Asset | Protocol Function on XRPL | Estimated Value | Market Share Contribution |

|---|---|---|---|

| Ripple USD (RLUSD) | Native Institutional Stablecoin | $317.8 Million | 38.78% |

| Ondo Finance | Tokenized United States Treasuries | $160.5 Million | 19.58% |

| CRX Digital Assets | Digital Asset Portfolio Management | $105.9 Million | 12.92% |

| Braza Crypto | Tokenized Financial Assets | $76.7 Million | 9.36% |

| Zeconomy | Broad RWA Protocol | $75.2 Million | 9.18% |

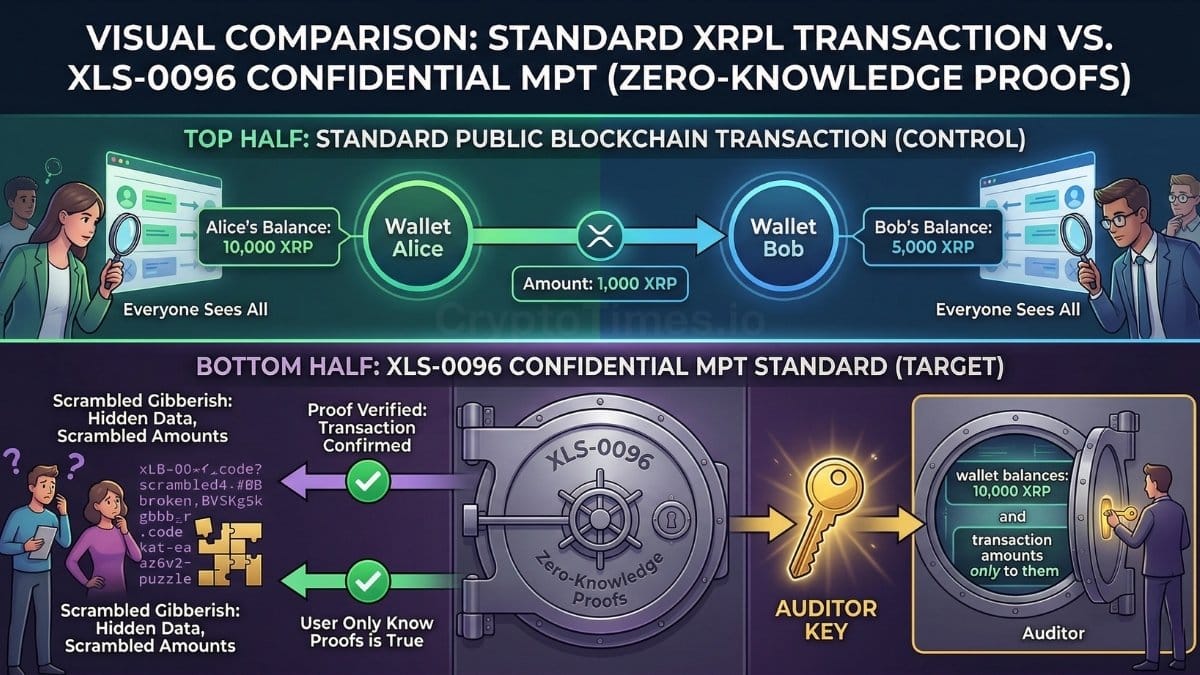

The XLS-0096 Confidential MPT Standard

One of the biggest obstacles to bank adoption of public blockchains has always been transparency. On a public blockchain, anyone can see transaction amounts and wallet balances. For a bank executing a large trade or managing a client’s portfolio, this is unacceptable — it would expose sensitive commercial strategy to competitors.

The most critical technological advancement driving institutional RWA adoption in 2026 is the proposed XLS-0096 standard, which introduces Confidential Multi-Purpose Tokens (MPTs). The XLS-0096 proposal solves this by embedding EC-ElGamal encryption and Zero-Knowledge Proofs (ZKPs) directly into the token standard.

This technology, often referred to as “Privacy for Sharks,” conceals individual wallet balances and transaction transfer amounts from public block explorers. Crucially, it maintains selective disclosure; network validators can still mathematically prove that total circulating supply rules are followed without decrypting the confidential balances, and issuers retain the ability to freeze assets for regulatory compliance.

The Next Frontier: Agentic Commerce and AI Payments

As we move deeper into 2026, the XRP Ledger is evolving to support a fundamentally new type of economic activity: Agentic Commerce. This concept revolves around autonomous artificial intelligence agents negotiating, buying, and settling payments with zero human intervention.

Traditional banking APIs, which rely on manual data entry and human-paced approvals, are entirely incompatible with machine-to-machine (M2M) transactions. Recognizing this shift, Ripple recently invested in t54, an AI infrastructure startup building a “trust layer for the agentic economy” directly on the XRP Ledger.

Through systems like the x402 facilitator, AI agents can utilize the XRPL to discover APIs, negotiate service pricing, construct shopping carts, and execute high-speed, sub-cent micro-transactions natively in XRP or stablecoins. This transitions the XRPL from a simple human-to-human remittance tool into a fully programmable, self-operating digital marketplace.

Conclusion

The story of XRP in 2026 is one of maturation. The resolution of a hostile regulatory climate has unlocked unprecedented institutional access, highlighted by Ripple’s OCC trust bank charter and integration into Mastercard’s global network.

While the native token’s price currently battles macroeconomic headwinds and internal competition from the highly successful RLUSD stablecoin, the underlying infrastructure of the XRP Ledger has never been stronger. With the implementation of advanced privacy protocols for real-world asset tokenization and early investments into AI-driven agentic commerce, XRP remains uniquely positioned at the convergence of traditional finance and next-generation decentralized technology.

Frequently Asked Questions (FAQs)

Why is the price of XRP still low in 2026 despite the lawsuit ending?

Despite achieving legal clarity and massive ecosystem milestones, XRP’s price in early 2026 has been suppressed by severe macroeconomic headwinds. Global geopolitical tensions, tariff shocks, and shifting monetary policies have triggered an institutional risk-off rotation, draining liquidity from altcoin spot markets and capping near-term price momentum.

What is the Ripple National Trust Bank?

In December 2025, the U.S. Office of the Comptroller of the Currency (OCC) granted conditional approval for the Ripple National Trust Bank. This federal charter allows Ripple to operate as an uninsured national trust bank, offering enterprise-grade digital asset custody, fiduciary services, and stablecoin reserve management across all 50 states under a single federal regulator.

What is RLUSD and how does it affect XRP?

RLUSD is Ripple’s institutional-grade stablecoin, pegged 1:1 to the US Dollar and backed by US Treasuries. While it has achieved massive success, reaching a $1.56 billion market cap by March 2026, it presents a “utility gap” challenge. Because institutions prefer the price stability of RLUSD for cross-border settlements, it is currently capturing much of the payment utility originally intended for the native XRP token.

Is XRP classified as a security or a commodity in 2026?

XRP is classified as a digital commodity. Following the conclusion of the SEC lawsuit in August 2025, which determined XRP is not a security when sold to retail investors, the SEC and CFTC issued a joint interpretive framework in March 2026 formally recognizing XRP as a digital commodity, placing it under the regulatory purview of the CFTC.

How does the XRP Ledger provide privacy for banks?

To attract major financial institutions, XRPL developers proposed the XLS-0096 Confidential MPT standard. This upgrade utilizes EC-ElGamal encryption and Zero-Knowledge Proofs to hide wallet balances and specific transaction amounts from public view, allowing banks to protect proprietary trading data while still maintaining full regulatory compliance and supply auditability.

Disclaimer:

Some elements of this content may have been enhanced with the help of our artificial intelligence (AI) assistants for purposes such as basic refinement, review, image generation, and translation to deliver high-quality news in a shorter time frame. However, all AI-assisted content is reviewed and approved by our team to ensure accuracy, fairness, and editorial integrity.