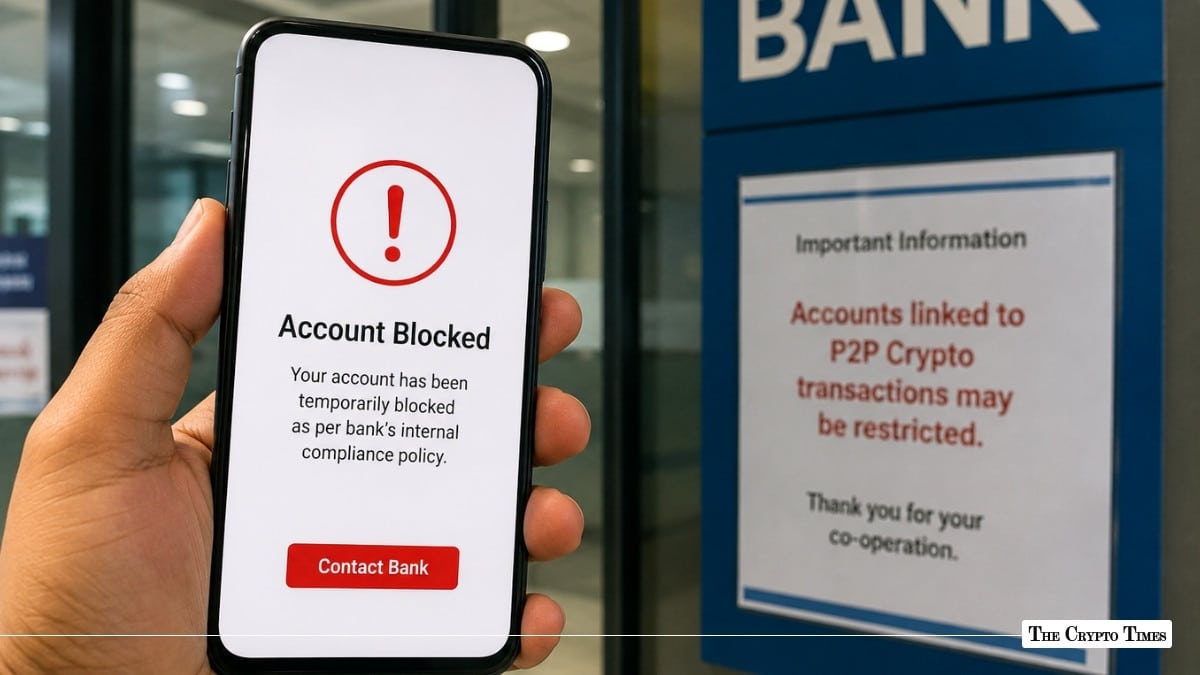

Indian crypto users continue to encounter sudden bank account freezes linked to Peer-to-Peer (P2P) transactions, even as the sector contributes significantly to government revenues through taxation.

Banks routinely freeze accounts and direct users to branches for resolution, treating many P2P inflows—particularly from international platforms—as high-risk under anti-money laundering (AML) and cyber fraud protocols. This occurs despite the 30% flat tax on virtual digital asset (VDA) gains (plus surcharge and cess) and 1% Tax Deducted at Source (TDS) on qualifying transfers, measures introduced in 2022 to bring the sector into the formal economy.

The taxation framework signals partial acceptance, yet banking practices lag. Banks file Suspicious Transaction Reports (STRs) to the Financial Intelligence Unit (FIU-IND) and impose liens under BNSS provisions (formerly CrPC Sections 91/102) based on police directives.

What is more concerning is that banks are locking entire balances, not just disputed sums, disrupting salaries, savings, and daily expenses for innocent traders.

Recent incidents highlight the scale. A recent case shared on X by user Coco_Airdrop illustrates the issue. An April 2025 Binance P2P UPI transfer of ₹22,500 triggered a debit freeze tied to a minor disputed amount of ₹3,010 in a cybercrime complaint, potentially requiring travel to Ludhiana for resolution with Punjab police.

This case is far from isolated. In early 2025, an SBI user reported their account frozen after three P2P trades of around ₹2 lakh each; funds traced to scams in Bihar and Madhya Pradesh led to multi-state cyber cell involvement, with partial release only after months.

Another trader saw ₹47,000 frozen across accounts in 2025-2026 due to links to Punjab and Chhattisgarh cases from November 2024 trades. In West Bengal, Nikhil’s HDFC account faced a freeze over a ₹3,115 lien, while Michael in Kerala dealt with an ₹8 lakh hold tied to multiple fraud flows.

These cases are few and far between what users have been sharing with The Crypto Times and asking for help since the past couple of years.

Community forums like Reddit’s r/CryptoIndia and Binance Square posts document dozens of similar complaints in 2025 and early 2026, with users reporting freezes from transactions as small as ₹600–₹1,700. Many involve verified merchants, yet upstream fraud traces back through UPI chains.

High courts, including rulings from Kerala and Madras, have criticized blanket freezes and ordered partial releases of non-disputed funds, but enforcement remains patchy and inconsistent across states.

Regulatory Disconnect and User Burden

This persistence raises critical questions about policy coherence between the government’s taxation regime and the banking system’s risk-averse stance. Why levy substantial taxes and TDS—mechanisms presupposing legitimate activity—while banks and enforcement agencies treat crypto P2P as inherently suspicious? The hybrid approach burdens compliant users without providing full operational legitimacy or safeguards.

P2P trading thrives due to liquidity on platforms like Binance, especially for retail users facing higher fees or liquidity constraints on fully compliant domestic exchanges. Scammers exploit these channels to layer illicit funds, but intermediaries bear disproportionate consequences.

The Reserve Bank of India (RBI) and Ministry of Finance push digital payments like UPI, yet crypto-linked flows trigger automated flags and investigations via the National Cyber Crime Reporting Portal (NCRP) and NCRB.

New Ministry of Home Affairs (MHA) guidelines seek timelines for resolution and partial unfreezes, but ground-level delays persist. Users must compile extensive documentation—transaction histories, chat logs, KYC proofs—and engage cyber cells, often requiring lawyers and potential interstate travel.

The economic fallout includes chilled participation, capital flight to unregulated avenues, and eroded trust. While domestic FIU-registered exchanges report transactions diligently, offshore P2P volumes endure.

Urgent Need for Systemic Reforms

Experts and affected users have long-questioned whether the current framework adequately balances fraud prevention with individual rights and economic innovation. Overbroad freezes for trace amounts disproportionately impact small traders and freelancers, many of whom pay taxes diligently on gains.

Calls for reform target clearer RBI guidelines for crypto inflows, proportional lien limits, a centralized verification database for faster genuine-user clearances, and expanded domestic on-ramps with investor protections. AML sandboxes and better inter-agency coordination could also minimize risks without stifling growth.

Until reforms materialize, the signal remains mixed: engage with crypto, pay your taxes, but operate at your own peril in a system not fully aligned. This pattern of incidents in recent months underscores deeper tensions in India’s digital finance ecosystem.

As UPI transforms payments and crypto gains global traction, harmonizing taxation, banking operations, and law enforcement is vital. Without it, more users will face disruptions, undermining the very revenue and innovation goals the government pursues.

Also read: Telegram Ban in India: Crypto, TON & Durov’s Attack on Reliance