The stablecoin market, long dominated by Tether’s USDT and Circle’s USDC, faces a significant new entrant. On June 30, 2026, Open Standard, a consortium backed by over 140 companies including Stripe, Visa, Mastercard, BlackRock, Coinbase, and others, announced Open USD (OUSD). This dollar-pegged stablecoin is designed for global payments and settlement, with most reserve yields returned to participants rather than captured solely by an issuer.

This development has sparked debate about whether OUSD could erode USDC’s position or even threaten the broader duopoly. Crypto investor and Dragonfly General Partner Rob Hadick offered a nuanced analysis in a detailed thread, arguing that while OUSD introduces real competition—particularly for USDC’s issuer Circle—it is unlikely to deliver a “death knell” for established players. Instead, it accelerates fragmentation in an expanding market.

The Birth of OUSD: A Consortium-Driven Model

OUSD stands apart from traditional stablecoins through its structure. Partners in the Open Standard ecosystem are positioned to share most of the interest earned on reserves (minus a small management fee). Minting and redemption are planned to be fee-free with no volume limits, addressing pain points businesses have cited with existing options like high costs at scale and limited influence over roadmap or economics.

Stripe has signaled it will make OUSD the default stablecoin for businesses on its platform. The token is expected to launch later in 2026 across multiple blockchains, with Solana among the confirmed or likely networks.

Zach Abrams, interim CEO of Open Standard and co-founder of Bridge (acquired by Stripe), emphasized building infrastructure “designed by the businesses growing it” for the internet economy.

The consortium’s breadth—spanning payments giants (Visa, Mastercard), asset managers (BlackRock), banks (BNY Mellon, Standard Chartered), tech firms (Google, Samsung), and crypto platforms (Coinbase, Ripple)—gives it impressive distribution potential. However, as Hadick noted, consortiums historically struggle with competing priorities among members, raising questions about unified push for adoption and liquidity bootstrapping.

Circle’s stock dropped sharply (around 15-17%) on the news, reflecting immediate market concerns about revenue pressure and partner shifts.

Tether (USDT): Gradual Decline in Dominance but Still the Undisputed Leader

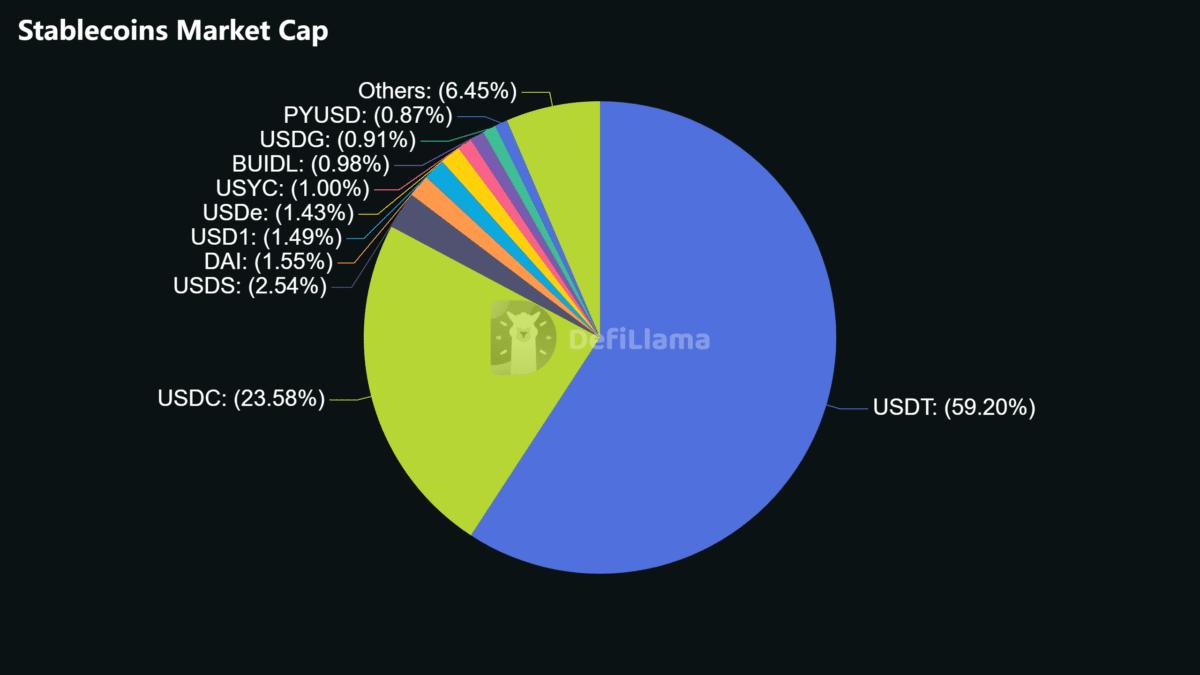

Tether’s USDT remains the dominant stablecoin by a wide margin, though its share of the overall market has been eroding gradually amid sector growth and new competition. As of early July 2026, the total stablecoin market capitalization stands at approximately $311.5 billion. USDT holds roughly $184.4 billion, translating to about 59.2% dominance. USDC follows at around $73.4 billion (roughly 23-25%).

USDT’s dominance has dipped below 60% at times in recent periods—the lowest levels since early 2023 in some snapshots—driven by the broader market’s expansion and gains by alternatives in specific segments.

Earlier in the cycle, USDT commanded higher shares (often 60-70%+ depending on the exact metric and timeframe). This gradual decline reflects diversification: USDC has gained ground in institutional and DeFi contexts, while other tokens and emerging options nibble at edges.

Despite the relative erosion, USDT’s absolute size and usage remain formidable. It excels in retail adoption, emerging markets, high-volume trading on centralized exchanges, and regions with capital controls or limited banking access. Daily trading volumes for USDT have historically dwarfed those of USDC by multiples in many periods. Tether continues to focus on distribution channels that major fintech and payment players may under-serve, positioning it as resilient.

Hadick echoed this resilience, stating that OUSD “is not their core market anyways” for Tether. The issuer will likely continue prioritizing areas outside Stripe’s and Circle’s primary focus, remaining “fine” even as overall market share trends downward in a growing pie.

USDT’s scale provides network effects that are hard to displace quickly, particularly where liquidity and acceptance matter most for traders and users in volatile or frontier environments.

Interestingly, Paolo Ardoino, Tether CEO, welcomed the launch of Open USD by calling it “Player 2” in the stablecoin market, positioning USDT as the dominant Player 1 while subtly downplaying USDC’s standing.

Circle’s USDC: Direct Exposure to OUSD Competition

USDC faces more immediate and nuanced pressure from OUSD. Stripe’s planned default status and the consortium’s payment-focused partners could shift usage among merchants, developers, and ecosystems previously favoring USDC. Yield-sharing mechanics in OUSD directly challenge the revenue models that have supported Circle, especially as redemption/mint fees face downward pressure industry-wide.

Hadick highlighted several counterbalancing factors for Circle. A potential restructuring or end to its longstanding Coinbase distribution deal could nearly double net revenue in the near term by removing revenue-sharing obligations, unshackling Circle to compete more aggressively.

Circle also benefits from deep existing liquidity, integrations, and a head start that creates switching costs for builders already using its APIs. Not every payments company or non-payments use case will automatically prefer OUSD, competing incentives among consortium members and greenfield opportunities play roles.

Regulatory and credit considerations also add complexity. If OUSD operates primarily through a bridge entity, it may not fully resolve enterprise penetration challenges that USDC has faced, as tokens ultimately represent credit to the issuer (and Open Standard/Bridge entities lack investment-grade status today). Moreover, global licensing and compliance remain hurdles for any new entrant.

Broader Market Fragmentation and Shifting Economics

Hadick has long argued that stablecoin fragmentation will worsen, with complexities abstracted away so the technology functions more as settlement infrastructure than a consumer-facing product.

OUSD represents another step in this direction: a harbinger of issuance economics trending toward zero, where value accrues to value-added products, licensing, bank networks, and applications built on top.

The total stablecoin market has grown substantially, with projections pointing toward $1 trillion or more in coming years as adoption expands in payments, DeFi, remittances, and tokenization. USDT and USDC together still control the vast majority (around 80-85% in recent data), but their combined dominance has softened slightly as the pie enlarges and specialized or consortium-backed options emerge.

This environment favors entities that control distribution and build superior tooling. Stripe’s strengths in product, engineering, and cross-selling give OUSD credible momentum in payments, though Hadick cautions that scaling liquidity to serve large end customers will require deep partner commitment amid competing priorities.

Challenges and Risks for OUSD

Despite its backers, OUSD is not guaranteed swift success. Bootstrapping sufficient liquidity and depth across chains will take time—consortium announcements have historically outpaced actual usage in stablecoins. Coordinating among fiercely competing partners (e.g., multiple payment networks and crypto platforms) risks diluted focus or internal friction.

Additionally, regulatory readiness, especially around compliance and potential parental guarantees, remains an open item. Other tokenized bank products and established players will continue competing aggressively. Analysts have noted that while the yield-sharing model is attractive, real-world adoption hinges on seamless integration, trust, and proven reliability at scale.

Outlook: Competition Intensifies, But Replacement Is Unlikely

According to Hadick, OUSD is unlikely to “replace” USDC outright in the near term. It will intensify competition, particularly pressuring yields and prompting faster innovation from incumbents. USDT’s position appears more insulated due to its different user base and channels. The bigger story is the maturation of stablecoins into shared infrastructure, with winners determined by who builds the most compelling layers on top.

For businesses and users, greater choice could mean lower costs and better-aligned incentives over time. For the ecosystem, it signals continued growth and professionalization. Hadick gives credit to Stripe’s forward-thinking leadership while emphasizing that scaling new liquidity and overcoming coordination challenges will prove harder and slower than many expect.

The stablecoin race is evolving from a two-horse contest into a more crowded, infrastructure-oriented field. OUSD adds a formidable contender, but USDT and USDC retain strong moats shaped by years of usage, liquidity, and specialization.

The ultimate outcome will depend on execution, regulatory clarity, and how effectively new and old players adapt to a fragmenting yet expanding market.

Also read: Circle CEO Picks Apart Open USD’s Pitch After Stock Falls 16%