On June 30, 2026, the digital asset market experienced a sudden wave of panic. An independent entity named Open Standard announced Open USD (OUSD), a new dollar-backed stablecoin. This wasn’t just another minor token unveiling. The project claimed the backing of a massive alliance of more than 140 global companies, spanning payments, banking, asset management, tech, and crypto infrastructure.

The list of reported members included heavyweights like Google, BlackRock, Coinbase, Stripe, Visa, and Mastercard. The market’s reaction was immediate and dramatic. Shares of Circle Internet Group tumbled by roughly 16% in a single session as investors worried that this new, corporate-backed stablecoin would erode the market share of USD Coin (USDC).

One crucial detail was lost in the noise: OUSD is not live. What launched on June 30 was the consortium and its operating company. The token itself is slated to go live only later in 2026, starting on Solana. In other words, the market repriced Circle on the announcement of a coin that does not yet exist and has zero circulating supply.

On social media and financial blogs, a popular narrative quickly formed: an alliance of 140 global giants with billions of existing users would easily crush the current stablecoin duopoly held by Tether (USDT) and Circle (USDC).

The panic seemed justified on the surface. Open USD promised a revolutionary business model designed to attack the core profitability of the incumbents. But within days, the hype began to face harsh realities.

While a massive corporate alliance makes for excellent headlines, it ignores how stablecoins actually work. Stablecoins are not consumer retail apps won through marketing campaigns and press releases. They are foundational financial infrastructure. In this arena, market share is protected by deep liquidity, long-standing user habits, order book density, and a structural fear among institutions of breaking systems that already work perfectly.

Despite its impressive corporate roster, Open USD faces an incredibly steep uphill battle. The entrenched “liquidity moat” enjoyed by Tether and Circle is far wider and deeper than the market’s initial reaction implied. For the unversed, a liquidity moat (or network effect moat) occurs when a market, exchange, or platform becomes the dominant trading venue because it naturally attracts the highest volume of buyers and sellers.

What is Open USD? The zero-fee gambit and revenue-sharing promise

To understand why the market panicked, it helps to look at what Open USD is trying to achieve. The project is led by founding CEO Zach Abrams, a well-known fintech operator who previously co-founded Bridge, the stablecoin infrastructure firm that Stripe acquired for $1.1 billion.

Open USD is pitched as a fix for a complaint that corporate enterprises have voiced for years about traditional stablecoins.

The traditional model vs. The shared model

In the models run by Tether and Circle, the issuing company keeps essentially all of the interest income generated by the reserves backing the coin. When a user hands over one dollar to mint USDT or USDC, that dollar is invested in safe, yield-bearing assets like short-term U.S. Treasury bills.

With interest rates meaningful, Tether and Circle generate billions of dollars a year in reserve income from what is essentially free user capital. Meanwhile, the platforms, wallets, and payment processors that actually distribute the stablecoin to users receive comparatively little.

Open USD aims to invert this dynamic through two core ideas:

The Zero-Fee Gambit: Participating businesses are promised the ability to mint and redeem Open USD with zero fees and no transaction volume caps.

The Revenue-Sharing Framework: Instead of retaining the interest income, the operating company (Open Standard) plans to keep only a small management fee to cover operational costs. The remaining reserve earnings are passed back to the platforms, businesses, and protocols that hold and distribute the token.

On paper, this sounds like a deal any corporation would sign immediately. It positions Open USD not as a proprietary corporate product, but as an open, low-cost utility whose economic rewards are shared with everyone who helps it grow. The announcement was a direct shot at the profit margins of Tether and Circle, prompting Tether’s CEO Paolo Ardoino to comment publicly, “Welcome OUSD. Player 2 has entered the game.”

The hype deflates: The corporate roster controversy

The narrative surrounding Open USD’s unstoppable rise relied on the assumption that its 140-plus partners were all fully committed to replacing their current stablecoin usage with OUSD. However, just three days after the announcement, on July 3, 2026, serious cracks appeared.

A series of public clarifications from major South Korean tech and financial giants, first surfaced by a Chosun Biz report, revealed that Open Standard’s partner list was far more aspirational than the launch suggested.

The Korean retractions

Samsung Electronics, South Korea’s dominant technology conglomerate, said it had held no formal consultations with Open Standard and did not even know what role it was supposed to play. Dunamu, the parent company of Upbit, South Korea’s largest digital asset exchange, then clarified that it was not participating in the actual issuance or launch of Open USD. It said it had merely indicated a willingness to consider joining the ecosystem at some point in the future.

Other named entities, including K Bank and Shinhan Financial Group, confirmed to local media that they had received only initial inquiries or basic pitches, were still reviewing the proposals internally, and had never authorized the public use of their corporate logos. At least one representative admitted the company learned it was included in the “alliance” only by reading the news.

The governance problem

This gap between Open Standard’s public roster and the reality of corporate commitment exposed real questions behind the hype.

The Transparency Gap: If a project counts casual email replies and introductory pitches as signed corporate alliances, the foundation of the ecosystem is fragile.

Compounding the issue, South Korea’s stablecoin rules remain unfinished, which has continued to delay firm commitments from local companies weighing foreign stablecoin projects. Open Standard’s decision to publish a large, unverified list created a temporary marketing splash, but it damaged the institutional trust required to challenge entrenched giants.

The myth of the logo: Understanding true stablecoin network effects

As Lorenzo Valente, ARK Invest’s Director of Research for Crypto, pointed out in his analysis, many observers are overestimating Open USD because they misunderstand how stablecoin network effects function.

Those effects are not created by a long list of corporate logos on a website. They are forged through daily user habits, deep integration into trading systems, collateral acceptance across automated protocols, market depth, and an institutional reluctance to break financial plumbing that already works.

When an investor or market maker looks at a stablecoin, they are not looking at who sponsors it. They care about one thing: liquidity.

If an institutional trader needs to exit a large position during a sudden market crash, they cannot wait for a new stablecoin to build up its order books. They need immediate execution with minimal price slippage. They will default to the asset with the deepest pools of capital, the tightest spreads, and the most reliable track record.

Tether and Circle have spent over a decade embedding their tokens into the global digital economy. USDT is the dominant asset across the offshore trading complex, while USDC has become a primary asset for regulated onshore applications and decentralized finance (DeFi).

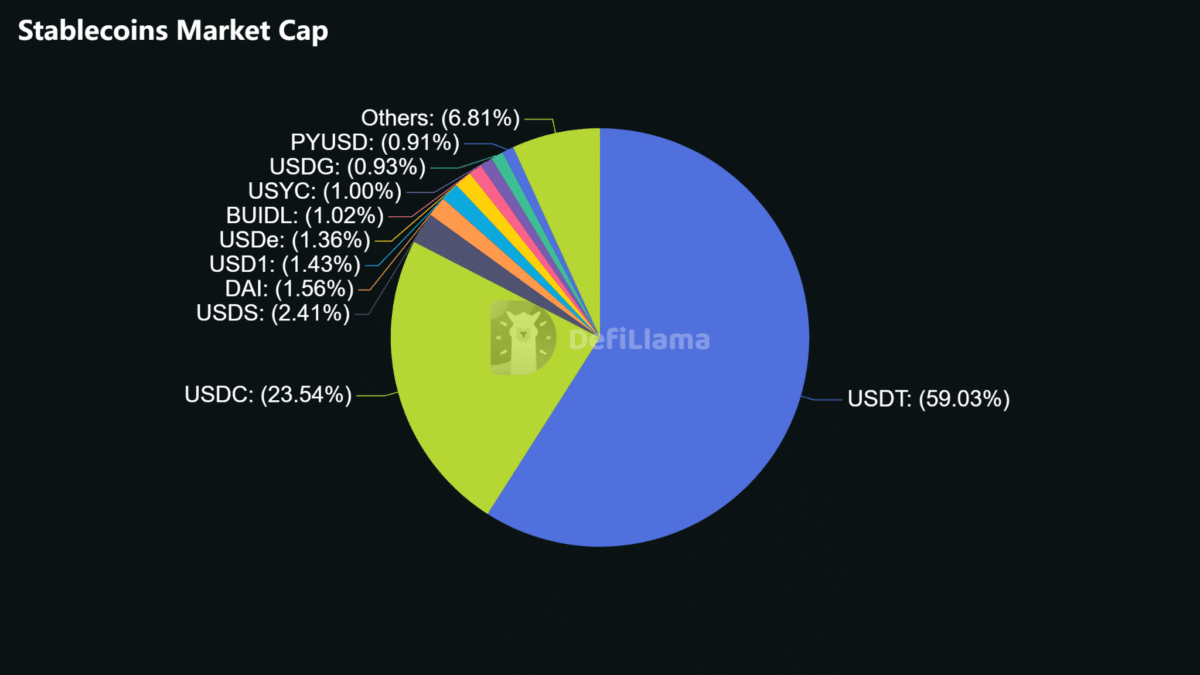

As of July 2026, USDT held roughly 59% of the stablecoin market and USDC about 23.5%, per DefiLlama. OUSD is targeting a duopoly from a standing start of zero supply. Breaking these deeply ingrained habits requires much more than offering a shared yield.

Why an exchange won’t torch its own liquidity

The most compelling argument for why Open USD will struggle to unseat the incumbents comes down to corporate self-interest. Proponents argue that major exchanges will push users toward OUSD to capture shared interest yield on customer balances. The largest exchanges are exactly where this logic breaks.

For a high-volume trading platform, a stablecoin is not idle cash sitting on a balance sheet. It is the quote asset, the cross-margin collateral base, the risk-management instrument, and the basic unit of account for millions of active traders. On the biggest venues, the overwhelming majority of stablecoin balances sit in USDT, and the platform’s core revenue engine, trading fees on enormous daily volume, dwarfs the interest income it could earn by capturing reserve yield.

That asymmetry is decisive. If an exchange forced its users off USDT to chase interest income, it would introduce structural friction: professional market makers would reallocate capital, bid-ask spreads would widen, and high-frequency traders and whales would migrate to offshore competitors where deep, instant USDT liquidity is still guaranteed.

Even a modest drop in core trading volume from thinned order books would wipe out far more high-margin fee revenue than the entire shared yield an OUSD-style model could provide. Risking a multibillion-dollar trading franchise to chase a smaller, variable interest float is a trade no rational executive makes. The underlying stablecoin liquidity is the glue holding the whole castle together.

The failure of subsidies: The Circle-Binance example

This isn’t theoretical. The strategy of buying stablecoin market share with cash incentives has already been tried, and it underwhelmed.

In December 2024, Circle struck a high-profile partnership with Binance to expand USDC. Circle’s own IPO filing later disclosed the terms: a one-time upfront fee of roughly $60 million, plus ongoing monthly incentives tied to the USDC balance Binance held, with Binance committing to hold billions in USDC.

The goal was simple: use direct financial rewards to scale USDC usage on the world’s largest exchange. Yet USDC’s footprint on Binance remained modest relative to USDT despite the outlay. The organic user base, global over-the-counter desks, and cross-border settlement systems simply kept defaulting to Tether, because that is where the rest of the world’s trading volume lives.

If a focused, well-capitalized company like Circle struggled to shift entrenched habits even with direct cash subsidies, a newly formed consortium starting from zero circulating supply faces a far steeper climb.

The consortium trap: Mismatched corporate incentives

Open USD’s central marketing pitch is strength in numbers, the idea that 140 companies together are stronger than a single issuer. But in the history of financial technology, large corporate coalitions are rarely agile.

More often, they suffer from governance friction and conflicting business goals. Even Christian Catalini, an economist who worked on Facebook’s ill-fated Libra project and wrote favorably about OUSD’s design, cautioned that coordinating governance “when parties need to collaborate first and then compete fiercely is not easy.”

The core vulnerability is a fundamental split in how the members make money.

The asset-under-management model

These are companies whose profitability relies on holding customer balances and capturing long-term float: digital wallets, neobanks, lending protocols, and institutional custodians. For them, the volume of OUSD sitting inside their applications is the key metric. They want users to lock capital up so the platform can clip the shared interest margin.

The turnover monetization model

This group includes global payment processors, card networks, and remittance companies such as Stripe, Visa, and Mastercard. They do not scale by hoarding idle cash; they make money on transaction velocity, processing fees, and currency conversion. To them, a stablecoin is a cheap, high-speed rail: OUSD should enter at point A, settle a transaction at point B, and convert back to fiat within seconds.

The tragedy of the commons

This split creates a structural flaw. The turnover-driven giants will do the heavy lifting of integrating OUSD into real-world checkout and settlement flows, generating volume, but because their model moves money out quickly, they create almost no permanent float.

Meanwhile, the passive holders will sit on the circulating supply without driving real-world usage, yet reap the majority of the distributed interest. The members driving adoption capture a fraction of the benefit while passive savers take the lion’s share. Over time, that imbalance strains the alignment the consortium depends on.

Compliance bottlenecks and capital starvation

Beyond internal friction, Open USD’s economics may starve its own operating company of the capital needed to fight a market war. Because OUSD is designed to be compliant and to route nearly all yield back to partners, keeping only a small management fee, Open Standard leaves itself financially thin.

Running a dominant stablecoin infrastructure is expensive: defending the peg through volatility, funding integration incentives across many blockchains, and maintaining large legal and compliance teams across jurisdictions all cost real money, the kind of sustained spending incumbents already fund from the reserve income they retain.

By giving away nearly all of its economics to keep partners happy, OUSD risks under-resourcing the very engine required to seed liquidity, incentivize market makers, and defend the peg when it matters most. Valente flagged exactly this: a thin fee model may leave the network underfunded compared with its multibillion-dollar rivals.

Why the duopoly remains safe

The launch of Open Standard is undoubtedly an important moment in the evolution of digital cash. It proves that traditional finance and major payment networks now treat stablecoins as essential infrastructure for global internet commerce.

But the initial belief that Open USD represents an immediate, existential threat to Tether and Circle looks overstated, especially for a token that has not yet gone live.

Stablecoins are the ultimate expression of liquidity network effects. They are sticky systems where utility compounds with market depth and long-standing trust. Open USD’s revenue-sharing framework is highly attractive on a slide deck, but it has to survive financial execution. It sacrifices operational simplicity, thins the resources of its own central entity, invites internal corporate conflict, and, before a single token has circulated, has already shown brittle partner commitments.

For a global exchange, a payment processor, or an institutional market maker, the primary question will never be, “How much extra interest income can I squeeze from my stablecoin provider?” It will be, “If I integrate this asset, does it guarantee deep, instant execution for my users, or does it introduce systemic liquidity risk into my core revenue engine?”

In most cases, the answer is clear. The value of uninhibited trading execution, paper-thin spreads, and a decade of proven survival means the market will keep defaulting to the deep, trusted channels of USDC and USDT. Open USD may well find a comfortable niche as a settlement asset within closed corporate payment networks. But the reigning duopoly remains well protected inside its liquidity moat.

Also Read: CLARITY, MiCA, GENIUS & UK’s Cap: How H1 2026 Rules Reshaped the Crypto Market