Key Highlights

- Cryptocurrencies are reshaping global finance, helping countries bypass sanctions, build reserves, and explore alternatives to traditional banking systems.

- Central Bank Digital Currencies (CBDCs) are emerging as state-controlled tools, enabling faster payments, reducing reliance on SWIFT, and influencing global trade.

- Crypto risks remain high, from hacks and scams to volatility, but nations continue to explore digital assets for resilience, de-dollarization, and economic strategy.

Cryptocurrencies have evolved from a niche digital experiment into a force shaping global finance and politics. Since Bitcoin’s launch in 2009 by the mysterious Satoshi Nakamoto, it has challenged traditional banks and government-controlled money, offering a truly decentralized alternative.

What began as a tech breakthrough has played a role in world politics, especially during major crises like the COVID-19 pandemic and the Russia-Ukraine war. In these moments, cryptocurrencies became a lifeline: Ukraine raised millions in Bitcoin and Ethereum for defense and aid, while Russia looked to crypto to get around sanctions and keep trading internationally.

The rise in crypto adoption

The rise of crypto adoption by both companies and countries underlines its growing strategic importance. Tesla, Strategy, and El Salvador—which recognized Bitcoin as legal tender in 2021—show how digital assets are entering mainstream finance.

At the same time, central banks are racing to develop Central Bank Digital Currencies (CBDCs), which allow governments to maintain control while embracing digital innovation. This highlights a tension between financial freedom, as championed by Bitcoin, and regulatory oversight.

Geopolitically, Bitcoin also challenges the U.S. dollar’s dominance. Some nations use it to conduct trade, monetize resources, or work around dollar-based sanctions. Iran and North Korea, for example, have reportedly used crypto to keep their economies functioning under international restrictions. Other countries, like Kazakhstan and Pakistan, are exploring crypto mining to turn excess energy into economic opportunities, though environmental concerns persist.

While stablecoins account for most daily trading volume, Bitcoin maintains nearly 59% share in the total crypto market cap. The market briefly reached $4 trillion earlier this year, driven by clearer regulations, institutional investment, and a wave of new financial products.

With this in place, cryptocurrencies are no longer just an alternative investment—they are reshaping global power dynamics, offering nations new ways to gain economic resilience, bypass sanctions, and rethink traditional financial systems.

Crypto as a tool for sanctions evasion and economic resilience

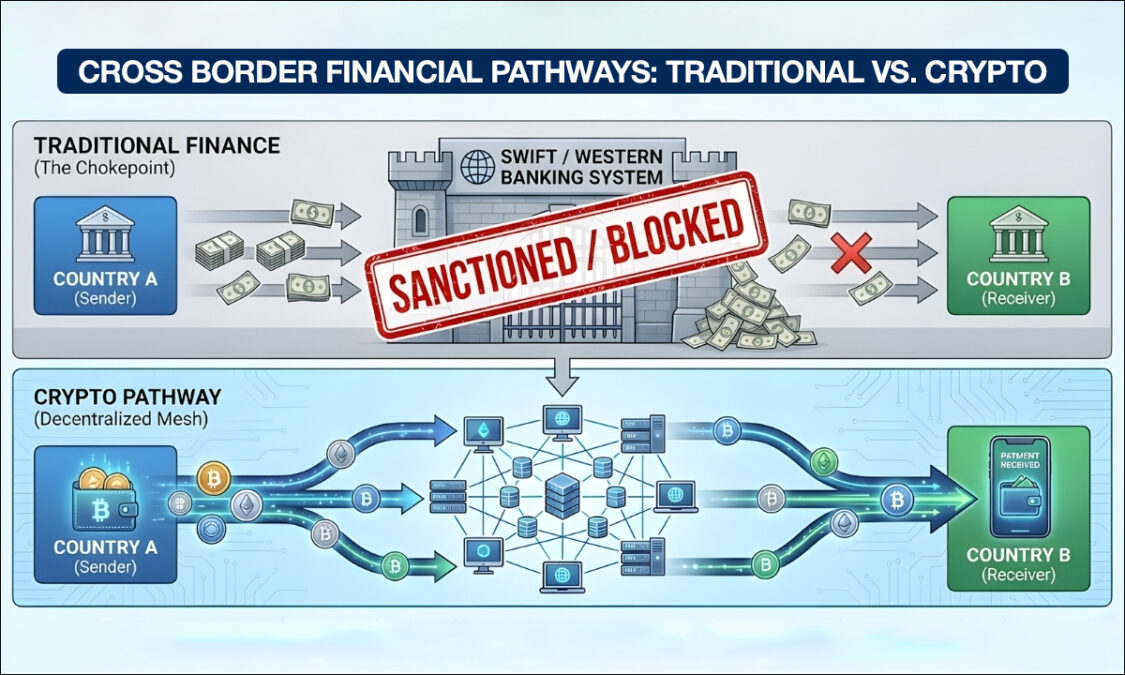

One of the most effective tools of foreign policy of the West has been economic sanctions. These are used by governments and other international bodies like the United States, European Union, and United Nations to limit access to worldwide finance, trade, and technology.

Traditionally, these actions are highly dependent upon the dominance that the U.S. dollar holds, the worldwide banking networks, and systems like SWIFT. However, with evolving technologies like blockchain and cryptocurrencies, the sanctioned nations are finding ways to bypass these restrictions.

At the forefront of the matter lies the nature of cryptocurrencies. In contrast to conventional money transfers, where the process follows the involvement of commercial banks, the processing of cryptocurrencies happens from digital wallet to digital wallet on a decentralized network. There exists no control over the transaction or reversal within it, nor are there any identifiable individuals attached to the wallets but rather encrypted alphanumeric codes.

This also diminishes the effectiveness of sanction enforcement, which relies on banks to highlight unusual transactions and freeze the funds of blacklisted individuals or organizations. Although controlled crypto exchange services must be obliged by know-your-customer (KYC) and sanctions regulations, most transactions originate from unregulated services or direct transactions between individuals, which are much more difficult to trace.

Western sanctions on Russia

Russia is one case that exemplifies the increasing use of crypto in sanctions resilience. After the sanctions were imposed by Western countries following the invasion of Ukraine in 2022, Russian businesses experienced growing delays in cross-border payments. Even the trade relationships that Russia had with countries such as China, India, and the UAE were made more difficult due to banks’ increasing caution resulting from Western regulation.

In reaction to this development, Russian legislators passed a law that makes it possible for businesses to use cryptocurrencies for cross-border transactions. This move was complemented by an initiative from the central bank regarding an “experimental” infrastructure that will allow cryptocurrencies for payment systems, with confirmations that transactions will occur before the end of that year. Cross-border transactions of cryptocurrencies are now legalized in Russia despite a ban on their use locally.

The act was justified by the Russians as a necessity in the face of real economic pressure. Arrears contributed to an 8% reduction in imports in the second quarter of 2024. Although there is an emphasis on using the currencies and methods within the BRICS group, transactions still take place in the environments provided by the dollar and euro. The use of crypto provides an escape route from these bottlenecks, especially in the form of stablecoins like USDT in the energy and commodities segment.

Iran’s strategic approach

Iran has followed a different yet equally thoughtful strategy. With sanctions due to the nuclear issue in place for several years, the Iranian government has concentrated efforts on both the development and usage of cryptocurrencies.

Regulating bitcoin mining within the country has ensured that miners enjoy subsidized energy rates. Also, the Iranian government has started incorporating cryptocurrencies into its trading structure.

In August 2022, the Iranian government permitted the utilization of cryptocurrencies as a payment option for imports. The move came just a short while after the country finalized its first official purchase of imported cars using cryptocurrencies, valuing approximately $10 million.

The new structure makes it acceptable for banks, exchange platforms, as well as miners in the Iranian economy, to facilitate the payment of bills for imports via cryptocurrencies, which was not feasible before due to the dominant influence of the US and European dollars.

Iran is also considering broader collaboration. There have been instances of Turkish authorities partnering with Tehran on projects like the “Muslim cryptocurrency,” and Iran and Russia have contemplated the concept of gold-backed stablecoins, designed to ease Iranian-Russian transactions.

Obvious restrictions on North Korea

North Korea can be considered the most extreme example. Being left out of the mainstream global economy, the state has made cybercrime one of its sources of funds. As per blockchain firm Chainalysis, the amount stolen by North Korean cyberhackers in 2025 reached a record level of $2.02 billion, increasing the total amount stolen to $6.75 billion.

Much of this is done by “hacking” crypto exchanges and taking advantage of vulnerabilities in areas such as cross-chain bridges. One of the biggest hacks for the year was $1.5 billion on crypto exchange Bybit, which was based in Dubai and attributed by U.S. officials to North Korea’s top government hacking squads.

The United States, as well as a private researcher, have repeatedly asserted that the North Korean government uses these thefts of cryptocurrency for funding their development of both their nuclear weapons and their missiles. It is easier for a money launderer to launder their cash using cryptocurrencies, which makes large wallets a ripe target. In other instances, they have managed to get a job in international companies as technical experts from a distance.

The story of Venezuela

Venezuela’s experience illustrates the challenges of crypto with government support. In 2018, Petro, a cryptocurrency that relied on oil reserves, was launched by the Venezuelan government with the aim of addressing the collapsing Venezuelan bolívar and working around sanctions. The idea was rejected from inception due to internal and external criticisms.

The Petro did not actually catch on beyond state-controlled channels. Charges of corruption and mismanagement led to the demise of this token. In 2024, the Venezuelan government officially disbanded Petro and reassigned any remaining tokens back to bolívars. Though unsuccessful, Venezuela is still looking at ways to utilize cryptocurrency.

Together, these examples illustrate just how cryptocurrencies are allowing for the development of other financial systems that operate outside the control of the West. Even though cryptocurrencies do not make sanctions obsolete, they make sanctions ineffective.

National adoption of cryptocurrencies as legal tender and reserves

Bitcoin has gradually transformed from being an esoteric digital currency to being a recognized component of the global financial system. Some countries are already accumulating Bitcoin in their financial plans, while others are finding a way to include it in their reserves. This trend shows that countries are moving towards adopting digital assets for diversification, leverage, and innovation in their economies.

El Salvador

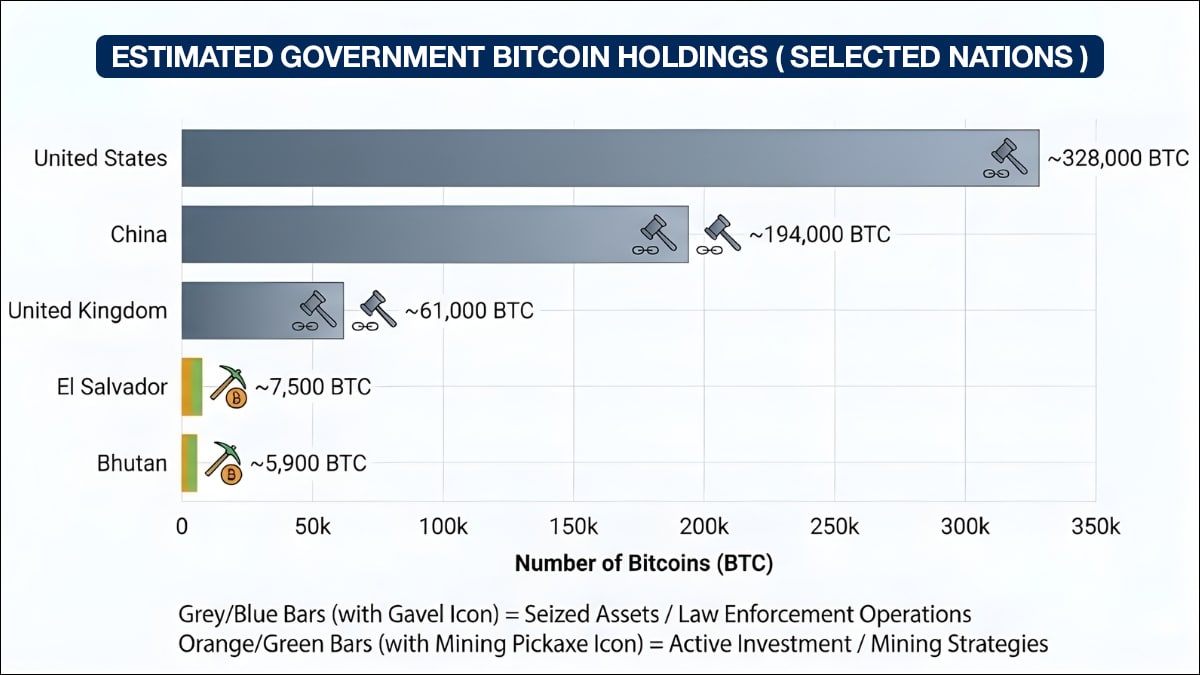

El Salvador made major headlines in 2021 by becoming the first country to recognize Bitcoin as legal tender. Today, it holds approximately 7,516 Bitcoin in its possession, valued at over $655 million at the time of publishing.

The reason behind El Salvador’s recognition as a ‘Bitcoin country’ is its President Nayib Bukele, who is a vocal supporter of Bitcoin. He advocates its usage in order to promote financial inclusion and bring foreign investment into the country. It seems that they are not letting any volatility concerns stop them. They continue purchases in phases and have introduced Bitcoin bonds.

Bhutan

Bhutan is also said to have an estimated holding of around 5,984 BTC in holdings. Bhutan’s state investment agency, Druk Holding and Investment, is also actively involved in investing in cryptocurrencies as well as bitcoin mining. Bhutan is one example of how countries can use bitcoin to pursue economic development.

United Kingdom

The United Kingdom (UK) has more than 61,000 Bitcoin, worth roughly $5.34 billion. This holding consists of BTC mainly seizures and related to financial crimes and dark web raids. Despite the fact that the UK considers Bitcoin illegal tender, the police have continued to acquire more.

China

China is said to have around 194,000 BTC, the second-largest government-held sum of Bitcoin in the world. Interestingly, the reason behind the majority of China’s total is largely because of the seizures from criminal cases, even when the nation has banned trading of cryptocurrencies among the Chinese population.

United States (US)

The leading holding is by the United States with around 328,372 Bitcoin, valued at over $29 billion. The US government has seized Bitcoin through high-profile cases. Some of these Bitcoins are auctioned, but enforcement activities contribute to an increased reserve.

Other countries

Besides, smaller reserves are held by countries like Finland (90 BTC), Georgia (66 BTC), and Venezuela (240 BTC) mostly related to seized or legal cases. Out of these, a few countries are expected to form reserves. There is also an expected creation of a State Fund of Digital Assets at the National Bank in Kazakhstan, including Bitcoin, as the country increasingly becomes a center for mining. Japan, which depends less on U.S. dollar reserves, also begins to consider holding Bitcoins.

The UAE and Singapore, two hotspots for innovation in crypto, could be possible reserve assets, and Singapore has already begun experiments with tokenized real-world assets. Meanwhile, Iran has been accumulating Bitcoin through state-controlled mining, using it to enable international trade in defiance of sanctions.

Some nations had previously held BTC but subsequently sold them in the open markets. The Australian government auctioned almost 24,500 BTC in 2016. The German government also sold nearly all of its confiscated reserves in the year 2024, including 49,858 BTC. The status in the Bulgarian case is unclear, as they confiscated more than 213,500 BTC. They may have lost or redistributed the funds.

CBDCs and state-controlled alternatives

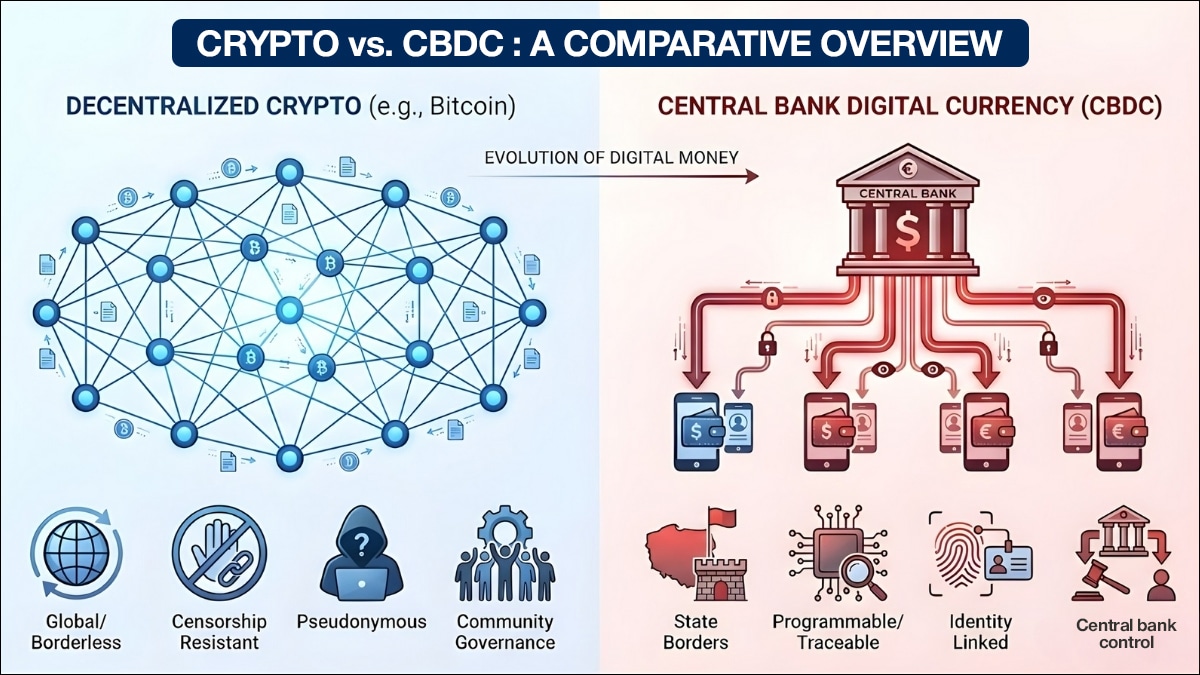

The central bank digital currencies, or CBDCs, are no longer considered a form of digital money but a strategic tool. Although the United States has banned the creation of CBDCs through the Anti-CBDC Surveillance State Act, other nations have already progressed. The Bahamas, Nigeria, Jamaica, and Zimbabwe have already introduced CBDCs in their economies. China and the European Union are already piloting their CBDCs.

CBDCs have been described as digital money that is an electronic form, used just like cash. On an international scale, CBDCs have been considered as tools for exercising influence so as to make payment systems more efficient and less reliant on SWIFT.

Unlike other cryptocurrencies like Bitcoin, CBDCs are under the control of the central banks of the nations in which they are used as the official currency. Although it is stable, the issue of surveillance is a major concern related to its use as programmable money. Stablecoins, as well as the value of cryptocurrencies like Bitcoin, are threatened by CBDCs but, on the other hand, verify the significance of the latter as a competing entity in the crypto market.

China’s e-CNY

One of the most sophisticated central banker digital currencies in the world was introduced by China in what it calls the digital yuan, or e-CNY. This digital currency was introduced by the People’s Bank of China. In China, the e-CNY can be used in usual day-to-day transactions like consumer purchases, transportation fares, bills, wages, and subsidies, and pilots have been conducted in major cities like Shenzhen and Chengdu. It was even employed during the Beijing Winter Olympic Games for foreign visitors on a trial basis.

Internationally, the role of the digital yuan is quite important. China is developing an international cross-border trade system to settle transactions outside of SWIFT networks and is less dependent on the US dollar. Though this system is more efficient and helps with financial inclusion, there are concerns regarding privacy issues and competition with existing private money transfer applications.

Russia’s digital ruble experiment

Russian authorities find themselves increasingly talking about the digital ruble and its potential role in supporting international trade and mitigating sanctions imposed by the West. Introduced by the Russian central bank in 2020, it is actually one of the ways and means of Russia’s overall strategy of avoiding both the US dollar and payment systems like SWIFT, which had rendered money transactions almost impossible after sanctions were imposed in 2022.

The digital ruble project aims to create a retail CBDC that enables payments and has already been piloted by a few commercial banks and real consumers. Benefits that the government sees are faster international payments, reduced costs, and enhanced control over monetary flows.

However, there are some challenges that exist in the project. Trust between the public and the state has been an issue, considering privacy concerns arising from state surveillance capabilities. There are also costs associated with bank integration, apart from ensuring that the design of the digital ruble conforms to the global standards for central bank digital currencies. Despite these challenges, the project is important for the de-dollarization process that exists in Russia.

UAE’s leap in CDBC

On the other hand, the Central Bank of the UAE launched the Minimum Viable Product (MVP) of the mBridge project, which is a multi-central bank digital currency platform for cross-border payments in June 2024. mBridge has been developed in collaboration with the BIS Innovation Hub, China, Hong Kong, and Thailand. This mBridge project is the first multi-CBDC project to have achieved this level of advancement.

The UAE successfully carried out its first real-value cross-border payment utilizing the Digital Dirham in January 2024, transferring AED 50 million to China via mBridge. It was the first CBDC cross-border payment between a MENA region and a non-regional partner.

Several banks licensed in the UAE have been able to connect to the mBridge platform and facilitate faster and cheaper payments in Central Bank Money. mBridge is part of the UAE’s Financial Infrastructure Transformation and promotes trade, less dependency on US dollar pricing systems, and brings world payments a step closer to real-time settlement.

Broader implications around CDBC

By the end of 2023, over 130 central banks, covering around 98% of the global economy, had started thinking about central bank digital currencies. However, some central banks have been planning to introduce digital currencies in the next five to seven years.

With the progression of CBDC initiatives, development is being divided along geo-political lines. Instead of a single global standard, regional blocs of compatible digital money are being developed among geo-political partners, thus threatening the emergence of a fragmented global payment system. This will go on to impact costs for businesses and individuals and can erode current financial infrastructure.

Preference is for public transparency of transactions, Europe advocates for privacy and regulation, and the US is moving towards a private stable coin, rather than a digital dollar. Such a move might start undermining the supremacy of the US dollar, though not necessarily because of a competitor, but due to other digital options.

De-dollarization and shifting alliances

The U.S. dollar is still the primary reserve currency; however, its prevalence is being increasingly called into question due to rising attention on de-dollarization. De-dollarization is a gradual reduction in dependence on the U.S. dollar for world trade and finance because of risks associated with U.S. politics as well as increased confidence in alternative arrangements.

Polarized America, trade conflicts between America against other countries, and extensive reliance on financial sanctions have all contributed to countries considering alternative arrangements. To date, the dollar remains the leader in international trade and exchange, representing almost 88% of FX transactions. This trend begins to emerge in changes in central reserves. The role of the dollar has been reduced to below 60%, but there has been a huge rise in holding gold, especially in emerging countries such as China and Russia.

Crypto and digital currency markets are also in this transformation, opening alternative corridors independent of dollar-denominated markets. The trend indicated through gold, local money, and crypto markets reflects an evolution to escape the dollar, rather than an immediate downfall.

BRICS Pay

The BRICS grouping has made the first move in its de-dollarization efforts by rolling out its own payment system called “BRICS Pay.” This payment system will help in facilitating cross-border payments within the member countries using blockchain technology, without having to rely on SWIFT payments.

The system was exhibited at the BRICS Business Forum in Moscow, and the attendees got demo cards preloaded with 500 rubles. Users utilized the demo cards at the participating vendors and made purchases using mainly QR code transfers. The system is capable of supporting cryptocurrencies and stablecoins pegged on national currencies.

BRICS is set to enhance the BRICS Pay system for business-to-business transactions and the formulation of the BRICS+ UNIT Digital Currency project. Leaders of the organization, including the President of Russia Vladimir Putin, see the system as a way of encouraging investment, enhancing financial independence, and providing choices for developing countries other than the Western banking architecture.

Iran and Russia’s joint exercise

In June 2023, Iranian and Russian fintech entrepreneurs utilized the FINEX exhibition in Tehran to evaluate the role that cryptocurrencies and blockchain technology may play in facilitating trade despite tough international sanctions.

It was generally an agreement by speakers from both nations that the collaboration on crypto has started, but that the process is still far from being fully implemented, especially in the Russian market.

There has been an indication by Iranian authorities that the process has started through the Iranian Central Bank, while Russia has started the process by issuing licenses on digital assets, among other laws.

Members underscored the importance of cooperation not only on cryptocurrencies but also on payment systems, lending tech, and micropayments. Russian delegates pointed out that sanctions have forced Russia to pay increased attention to fintech and learn from Iran’s experience operating without SWIFT for so long.

There were assertions of further discussions on the establishment of alternative international payment infrastructure and the connection of their card systems. Delegates reported that digital money is bound to find increased usage in international transactions of 2024.

Risks, challenges, and countermeasures

Although the blockchain technology is secure, crypto exchanges as well as wallets have been subjected to hacks and scams, rendering users helpless about the theft of their money. On top of that, matters are complicated by taxation issues, as it is considered property in many countries.

Furthermore, the absence of consumer protection, the irreversibility of transactions, and the environmental impact associated with energy-intensive mining methods continue to create ongoing concerns. Nevertheless, the interest in crypto and the initiatives towards better regulation, security, and sustainability continues to develop.

Law enforcements against Tornado Cash

In 2022, a tough regulatory approach was enforced by the U.S. against crypto ‘tools of illicit finance,’ with the imposition of sanctions on ‘Tornado Cash,’ a well-known ‘virtual currency mixer’ operating on the Ethereum blockchain.

According to a press release by the U.S. Treasury’s Office of Foreign Assets Control (OFAC), Tornado Cash had been used to launder more than $7 billion worth of virtual currencies since 2019. It involves more than $455 million of Kunia stolen by the Lazarus Group which is a North Korean entity. Tornado Cash was also associated with some ‘high-profile hacks,’ including ‘Harmony Bridge and Nomad Hack events,’ that occurred in 2022.

“Tornado Cash had not established effective controls despite making public claims of respecting privacy,” officials explained. As noted, the protocol facilitated money laundering by obfuscating transaction origins and destinations. Moreover, hackers and scammers can utilize the protocol to launder their stolen funds.

The Treasury emphasized that most of the operations of cryptocurrencies are legal, although tools for mass anonymity pose serious national security risks. This move symbolizes the overall effort of the West to promote transparency, stronger regulation, and vigorous enforcement in the world of cryptocurrencies.

Hacks and exploits in crypto

From 2023 to 2025, North Korea has proven to be a prominent player in high-value cryptocurrency heists, being blamed for more than half of the over $2.7 billion stolen from cryptocurrency hacks during this time. North Korea has deliberately moved their hacks from decentralized bridges to central exchanges and wallets, preying on human weakness via social engineering attacks involving fake job recruitment as well as malware.

Also Read: Exclusive: Are these North Korean Hackers behind WazirX Hack?

After the thefts, the regime has contracted the laundering process to the so-called “Chinese Laundromat” – the system of shadow bankers, Over-the-Counter (OTC) desks, and trade-based money transfer system. The funds are layered through multi-level money puzzles, transformed into the stablecoins like USDT and ransacked both through fiat and mirror payments.

Moving beyond being just digital money

Cryptocurrency has moved beyond the confines of being just digital money to become part of how countries manage trade, finance, and economic challenges. From Bitcoin donations to using crypto to work around sanctions, these new types of currencies are increasingly tied to national strategies. The world governments are exploring a variety of ways to use cryptocurrencies for reserves, mining, or their legal recognition.

Meanwhile, CBDCs are granting states more control over money while modernizing the infrastructure of national payment systems. China’s digital yuan, Russia’s digital ruble, or even the UAE’s mBridge project demonstrate how governments are using digital money to make transactions more efficient.

Going forward, countries that adapt—be it through holding crypto, implementing CBDCs, or finding ways around sanctions—may have more options in a changing global system. But risks remain around heavy volatility in prices and security threats, while regulations are still evolving.