Key Highlights

- Stablecoins have evolved into the core “transport layer” of global finance, settling over $1.25 trillion in monthly adjusted transaction volume as of late 2025.

- The U.S. GENIUS Act legitimized the sector by enforcing 1:1 reserve backing and banning interest on payment coins, driving a structural split between payment tokens and yield-bearing assets.

- Major institutions like Stripe, Visa, and BlackRock have moved beyond pilots to full commercial integration, cementing stablecoins as critical infrastructure for 24/7 settlement.

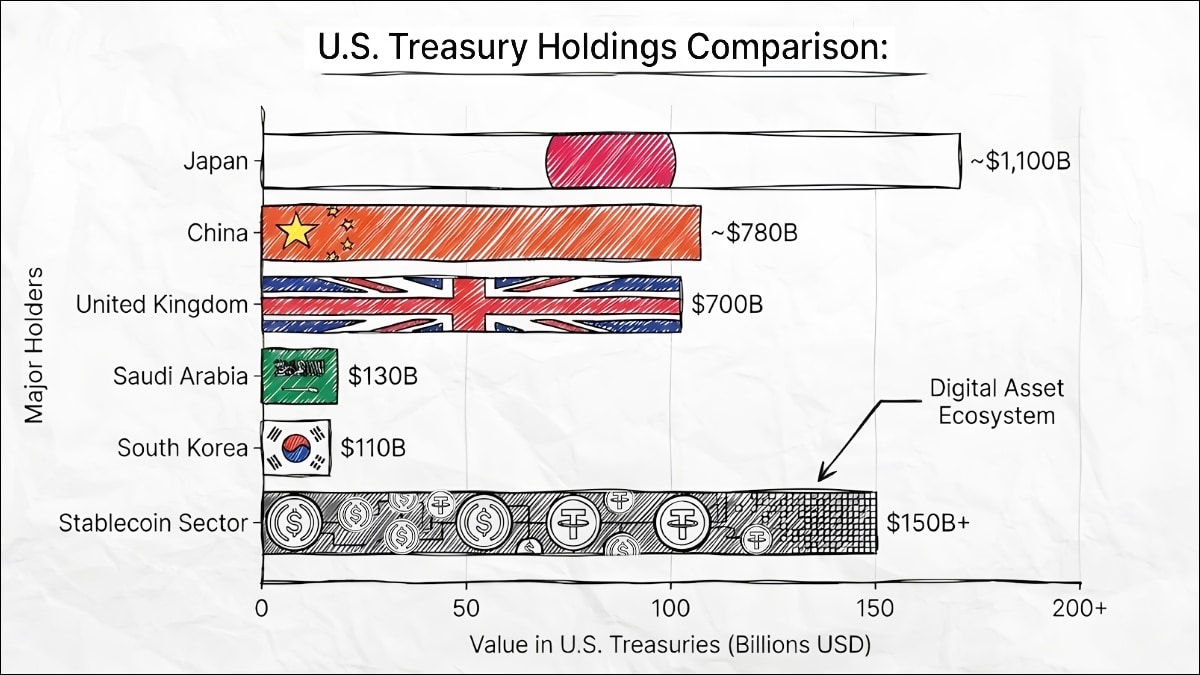

- Private stablecoin issuers have effectively become the U.S. alternative to a retail CBDC, collectively holding over $150 billion in U.S. Treasuries to reinforce dollar dominance.

For years, “crypto” was synonymous with volatility, a speculative casino operating on the fringes of finance. By late 2025, however, the narrative has shifted. The most significant development in the digital assets is no longer Bitcoin or Ethereum, but the steady rise of stablecoins as the new “transport layer” for the global economy.

The numbers tell the story of a quiet revolution. As of November 2025, weekly adjusted stablecoin transaction volume reached nearly $3.5 trillion, a figure that now rivals the throughput of established payment networks like Visa and exceeds PayPal.

According to DefiLlama data, the total market capitalization of stablecoins has surged past $300 billion, and stablecoin issuers, like Circle and Tether, have become heavyweights in the sovereign debt market, collectively holding over $150 billion in U.S. Treasuries.

This article analyzes the structural pivot of 2025, a year defined by the transition from the “Wild West” to a regulated financial infrastructure. It explores how regulatory catalysts like the GENIUS Act have paved the way for institutional giants like JPMorgan and Stripe, and how a new taxonomy of digital money is reshaping the future of global finance.

The regulatory catalyst: From ambiguity to architecture

The surge in institutional activity within the crypto industry in 2025 was not accidental; it was engineered by legislative clarity. After years of uncertainty, major economies established the “rules of the road,” giving traditional finance (TradFi) the confidence to build.

The American framework: The GENIUS Act

On July 18, 2025, the United States enacted the Guiding and Establishing National Innovation for US Stablecoins Act (GENIUS Act). The legislation legitimized payment stablecoins while imposing strict banking-style guardrails.

- Yield ban: To protect the commercial banking model, the Act explicitly prohibits issuers of payment stablecoins from paying interest to end-users. This ensures that stablecoins function as digital cash (a medium of exchange) rather than competing directly with bank deposits (a store of value).

- Reserve mandates: Issuers must maintain 1:1 reserves in cash or short-term U.S. Treasuries with maturities of 93 days or less. This eliminates the “run risk” associated with riskier corporate debt backing.

- Anti-CBDC stance: Parallel to the GENIUS Act, the U.S. advanced the Anti-CBDC Surveillance State Act, effectively halting the Federal Reserve from issuing a retail digital dollar directly to the public. The U.S. strategy is clear: the digitization of the dollar will be a private-sector endeavor, regulated by the government but operated by firms like Circle and PayPal.

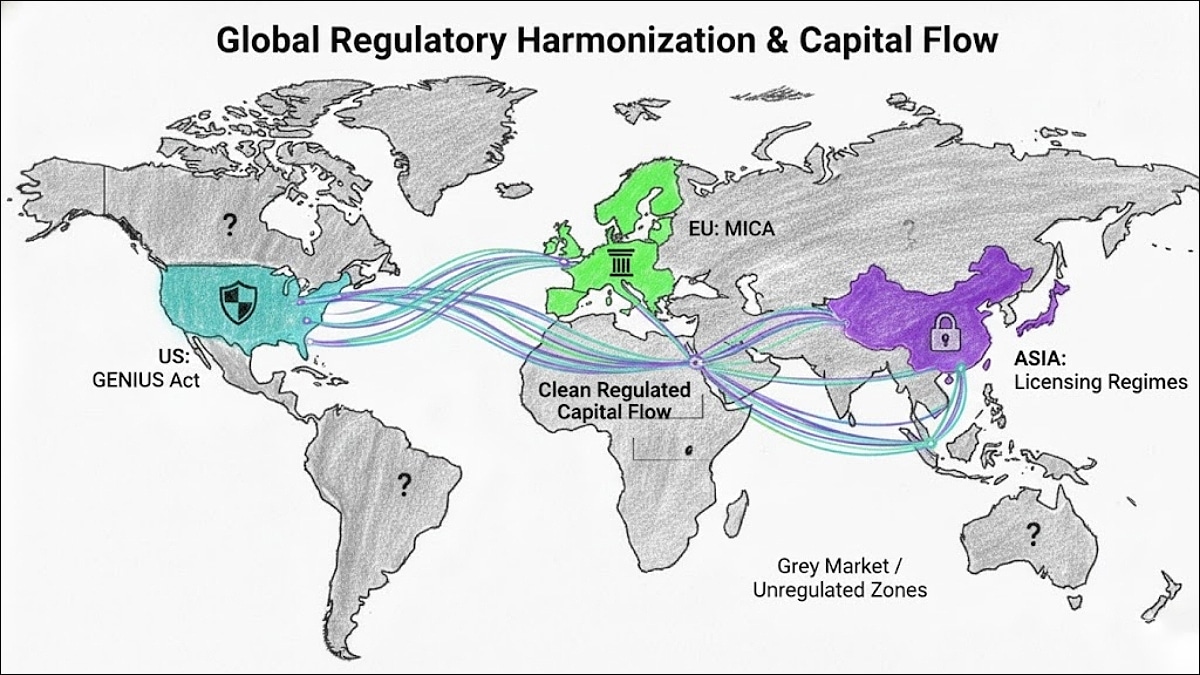

Global harmonization

The U.S. move complemented the full implementation of the Markets in Crypto-Assets (MiCA) regulation in the European Union in 2025. MiCA banned algorithmic stablecoins and enforced strict segregation of client funds. Similarly, Hong Kong’s stablecoin licensing regime went live in August 2025, creating a coherent global corridor for regulated digital value transfer.

Classification of stablecoins: The spectrum of stability

With regulations drawing clear lines, the market has bifurcated into distinct categories. It is no longer just “stablecoins”; it is a sophisticated taxonomy of instruments serving different needs.

1. Fiat-backed “payment” stablecoins

These are the standard-bearers of the industry, designed purely for transaction velocity.

- Examples: USDC (Circle), USDT (Tether), and PYUSD (PayPal).

- Characteristics: Under the GENIUS Act, these tokens are fully reserved by cash and Treasuries but pay zero yield to the holder. They serve as the “checking accounts” of the blockchain world—safe, liquid, and ready to spend.

2. Synthetic and yield-bearing dollars

To circumvent the GENIUS Act’s yield ban, the crypto-native market innovated with “synthetic” dollars that generate returns through financial engineering rather than simple interest.

- Leader: Ethena (USDe). By late 2025, USDe became the third-largest stablecoin.

- Mechanism: It maintains its peg not just through reserves, but by holding crypto assets and hedging the price risk with short futures positions. This “delta-neutral” strategy generates yield (often ~10% APY) from derivatives funding rates, attracting billions from investors seeking returns on their idle cash.

3. Tokenized real-world assets (RWAs)

Institutions are also tokenizing traditional assets to create value-stable instruments that sit outside the strict definition of a “payment stablecoin.”

- Commodities: The HSBC Gold Token has achieved massive adoption in Hong Kong, surpassing $1 billion in transaction volume. It proves that retail investors are eager to use blockchain rails to trade “hard assets” like gold.

- Tokenized Treasuries: Products like BlackRock’s BUIDL fund allow institutional investors to hold tokenized shares of a Treasury fund. These function like stablecoins but legally constitute securities, allowing them to pay yield to qualified holders.

The institutional shift: Who is building what?

In 2025, institutions moved from “exploring” blockchain to deploying it as core infrastructure.

The payments giants: Infrastructure integration

- Stripe and Bridge: Stripe acquired stablecoin infrastructure platform Bridge for $1.1 billion. This acquisition allows Stripe to embed stablecoin payments natively, enabling merchants globally to accept and settle transactions in digital dollars without managing complex crypto wallets.

- Visa: Visa launched a dedicated Stablecoin Advisory Practice in late 2025. More importantly, it expanded its settlement capabilities, allowing partners to settle obligations in USDC on high-speed blockchains like Solana and Ethereum, effectively bypassing the slow correspondent banking network.

The banks: Bridging the yield gap

Banks are navigating the GENIUS Act by offering tokenized deposits and funds that can pay interest.

- JPMorgan’s “MONY”: To solve the “no yield” problem of payment stablecoins, JPMorgan launched the “My OnChain Net Yield” (MONY) fund on Ethereum. This tokenized money market fund allows institutional clients to keep capital on-chain while earning a return, a critical feature for large corporate treasuries.

- JPM Coin on Base: Breaking out of its private walled garden, JPMorgan made its JPM Coin available on Base (Coinbase’s Layer 2 network), allowing for broader interoperability with the wider crypto ecosystem.

The new entrants: AI and political finance

- Cloudflare’s NET Dollar: Recognizing that AI agents need their own money, Cloudflare announced the NET Dollar. This stablecoin is designed for micropayments—allowing AI agents to autonomously pay for API calls and compute power in real-time, a use case that traditional credit cards (with their high fixed fees) cannot support.

- World Liberty Financial (USD1): The Trump family-backed DeFi project launched USD1, a stablecoin deeply integrated with Binance. With massive liquidity support (including a $2 billion injection from an Abu Dhabi-linked firm), USD1 represents the politicization of digital finance, blurring the lines between governance and commerce.

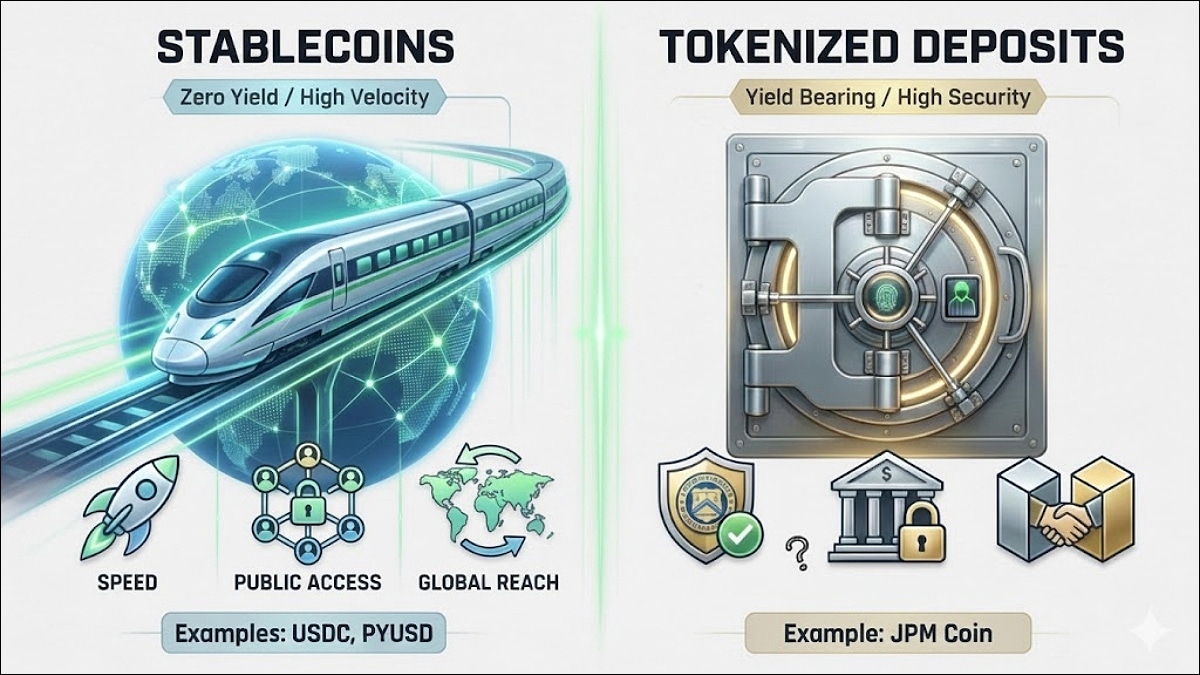

The “great bifurcation”: Stablecoins vs. tokenized deposits

A critical distinction has emerged in the 2025 landscape: the split between stablecoins and tokenized deposits.

| Feature | Stablecoins (e.g., USDC, PYUSD) | Tokenized Deposits (e.g., JPM Coin) |

| Nature | Bearer Instrument (Digital Cash) | Bank Liability (Digital Deposit) |

| Backing | High-Quality Liquid Assets (Treasuries/Cash) | General claim on bank balance sheet |

| Insurance | Uninsured (Issuer risk) | FDIC Insured (up to limits) |

| Yield | 0% (Prohibited by GENIUS Act) | Interest Bearing |

| Network | Public Blockchains (Ethereum, Solana) | Permissioned/Private Ledgers |

Institutions face a trade-off: Stablecoins offer superior interoperability and global reach, making them ideal for cross-border payments. Tokenized deposits offer regulatory safety and yield, making them the preferred vehicle for wholesale interbank settlement.

Geopolitics and macro: The “digital dollar” strategy

The U.S. embrace of stablecoins is a strategic geopolitical play.

Privatization of seigniorage

By outsourcing the digital dollar to private issuers, the U.S. has found a new way to finance its debt. Stablecoin issuers are now among the top holders of U.S. Treasuries, creating a structural buyer for government debt at a time when foreign central bank demand is waning. This “privatization of seigniorage” extends the dollar’s hegemony into the digital realm, as 99% of all stablecoins are USD-denominated.

The battle for settlement: The BIS counter-move

While the U.S. favors private rails, the Bank for International Settlements (BIS) is pushing the “Unified Ledger” concept (Project Agorá). The BIS argues that stablecoins fail the tests of “singleness” and “finality,” and proposes a shared global ledger for central banks to maintain control over settlement. This sets up a clash between the agile, private-sector “Silicon Valley Dollar” and the centralized, public-sector “Unified Ledger.”

Risks and the road ahead (2026-2030)

As the industry looks toward 2030, several friction points remain.

- Narrow banking risk: The Federal Reserve has expressed concern that if stablecoins grow too large, they could drain deposits from commercial banks (which lend to the economy) into stablecoin reserves (which sit in Treasuries). This “narrow banking” phenomenon could increase the cost of credit for businesses and consumers.

- Compliance vs. privacy: The FATF Travel Rules are now live in 99 jurisdictions, requiring the tracking of crypto transactions. This creates a tension between the open, permissionless nature of blockchains and the surveillance requirements of the banking state.

- Market forecast: Despite these risks, the trajectory is upward. Analysts at Citi and Standard Chartered project the stablecoin market could reach $3 trillion to $4 trillion by 2030.

Conclusion

2025 will be remembered as the year the “stablecoin narrative” matured from a crypto subplot into a main chapter of global finance. The passage of the GENIUS Act and the entry of heavyweights like Stripe, BlackRock, and JPMorgan signal that the infrastructure phase is largely complete.

The future financial system will be hybrid: built on the safety of regulated banking but running on the high-speed rails of blockchain technology. Whether through a bank-issued tokenized deposit or a private stablecoin paying for AI compute, the dollar has effectively been upgraded for the internet age.