U.S. inflation is no longer background noise for crypto markets in 2026. It is the main filter behind Bitcoin ETF flows, dollar liquidity, Treasury yields, gold demand, stablecoin positioning, and the growing rush into tokenized real-world assets.

The April CPI report showed U.S. consumer prices rising 3.8% year over year, up from 3.3% in March. Core CPI, excluding food and energy, rose 2.8%, while energy prices jumped 17.9% and gasoline rose 28.4% over the year. Food prices rose 3.2%.

That immediately changes the crypto setup. Inflation is bullish for Bitcoin only when investors see it as a fiat-debasement hedge. But inflation can also be bearish when it pushes the Federal Reserve toward tighter policy, higher real yields, and a stronger dollar.

The sharper 2026 reality is this: Bitcoin is not the whole inflation trade. Crypto investors now have three separate hedge lanes — Bitcoin, tokenized Treasuries/RWA, and traditional defensive assets like gold and TIPS.

Inflation data: CPI, PPI, PCE and the Fed

| Indicator | Latest reading | Market meaning |

|---|---|---|

| Headline CPI | 3.8% YoY in April | Inflation is moving away from the Fed’s 2% target |

| Core CPI | 2.8% YoY in April | Underlying price pressure is still sticky |

| Energy CPI | 17.9% YoY in April | Energy shock adds pressure to consumers and miners |

| Gasoline CPI | 28.4% YoY in April | Transport and fuel costs can feed broader inflation |

| PPI final demand | 1.4% MoM, 6.0% YoY in April | Wholesale inflation may pass into consumer prices |

| PCE price index | 3.5% YoY in March | Fed-preferred inflation gauge remains hot |

| Core PCE | 3.2% YoY in March | Fed has little room to declare victory |

April PPI is the second warning sign. The Producer Price Index for final demand rose 1.4% in April, the largest monthly increase since March 2022, and rose 6.0% year over year, the largest 12-month increase since December 2022. Goods prices rose 2.0%, services rose 1.2%, and gasoline prices accounted for more than 40% of the goods increase.

PCE adds another layer. The BEA’s March data showed the PCE price index rising 3.5% year over year, while core PCE rose 3.2%. The next PCE release is scheduled for May 28, 2026, making it the next major macro checkpoint after CPI and PPI.

The Federal Reserve held the federal funds target range at 3.50% to 3.75% on April 29 and said it remains committed to returning inflation to its 2% objective. That keeps crypto trapped between two forces: the long-term debasement trade and the short-term rate shock.

Why inflation does not automatically make Bitcoin go up

Bitcoin’s inflation story is simple on paper: fixed supply, no central bank, global settlement, and a hard-money narrative. But the market does not trade only on that story.

When inflation rises, traders first ask three questions:

| Question | Why it matters for crypto |

|---|---|

| Will the Fed stay hawkish? | Higher rates pressure risk assets |

| Are real yields rising? | Bitcoin struggles when inflation-adjusted bond returns improve |

| Is ETF demand strong enough? | Institutional flows now drive Bitcoin’s hedge narrative |

The real-yield piece is critical. FRED’s 10-year breakeven inflation rate measures expected average inflation over the next decade, derived from nominal Treasuries and inflation-indexed Treasuries. The monthly 10-year breakeven rate stood at 2.38% in April, while the 10-year real interest rate was 1.63% in May. Higher real yields make Treasury-linked assets more attractive and can weaken Bitcoin’s short-term bid.

That is why Bitcoin can be right on the long-term monetary story and still sell off on a hot CPI print.

Crypto market snapshot

Bitcoin was trading around $80,000, while Ethereum traded near $2,266 on May 13. Coinbase shares were near $201.78, Strategy traded near $178.82, MARA traded near $12.78, and Riot Platforms traded near $24.70.

| Asset | Inflation-trade role | Current read |

|---|---|---|

| Bitcoin | Debasement hedge | Strongest crypto hedge, but rate-sensitive |

| Ethereum | Productive crypto beta | More tied to risk appetite and tokenization growth |

| Stablecoins | Dollar liquidity | Useful for liquidity, not inflation protection |

| Tokenized Treasuries | On-chain cash yield | Strong defensive crypto-native lane |

| Gold / tokenized gold | Defensive hard asset | Cleaner hedge than BTC during shocks |

| TIPS | Direct CPI hedge | Best traditional inflation-linked asset |

| Crypto stocks | Public-market crypto beta | Exposed to both crypto demand and equity-rate pressure |

Bitcoin: best crypto hedge, not the cleanest inflation hedge

Bitcoin remains the strongest hedge asset inside crypto because it is the only large-cap digital asset with a clear scarcity narrative, ETF access, deep liquidity, and growing institutional recognition.

But Bitcoin’s hedge status is conditional. It works best when inflation fears combine with liquidity support, ETF inflows, a weaker dollar, and falling confidence in fiat money. It struggles when inflation pushes real yields higher, the dollar strengthens, or investors reduce exposure to risk assets.

That is exactly what ETF flows are showing.

| Date | U.S. spot Bitcoin ETF net flow | Market signal |

|---|---|---|

| May 4 | +$532.3M | Strong institutional dip buying |

| May 5 | +$467.3M | Hedge bid still active |

| May 6 | +$46.2M | Momentum slowed |

| May 7 | -$268.5M | Rate and macro pressure returned |

| May 8 | -$145.7M | Outflows continued |

| May 11 | +$27.2M | Weak rebound |

| May 12 | -$233.2M | Inflation/Fed fear hit demand again |

Farside data shows that U.S. spot Bitcoin ETFs posted strong inflows on May 4 and May 5, but the trend reversed sharply with outflows on May 7, May 8, and May 12. The May 12 outflow totaled $233.2 million, led by redemptions from FBTC, ARKB, IBIT, BITB, and GBTC.

That flow pattern is the whole Bitcoin inflation debate in one table. The digital-gold narrative is alive, but it still needs real institutional demand to overpower macro pressure.

On-chain signals: the hedge trade still needs proof

Bitcoin’s inflation-hedge narrative is facing a harder test in 2026 as on-chain data shows stronger holder profits, slower momentum, and renewed selling pressure near key resistance levels.

The key metrics to track are:

| Metric | What it shows |

|---|---|

| Long-term holder supply | Whether conviction holders are accumulating or distributing |

| Exchange balances | Whether coins are moving into cold storage or exchanges |

| ETF holdings and flows | Whether institutional demand is absorbing supply |

| Realized cap | Whether capital is entering or leaving the network |

| MVRV | Whether holders are sitting on large unrealized profits |

| Short-term holder SOPR | Whether recent buyers are selling into profit |

| BTC vs gold correlation | Whether Bitcoin is behaving like hard money |

| BTC vs Nasdaq correlation | Whether Bitcoin is behaving like tech beta |

Recent on-chain reads are mixed. Glassnode’s Week 19 market pulse said overhead supply was beginning to cap Bitcoin momentum, with declines in price momentum, net buying pressure, and trading activity. CryptoQuant also flagged rising realized profits, with daily realized profits reaching 14,600 BTC on May 4, the highest since December 2025.

That means Bitcoin is still in a “prove it” zone. The asset has the best crypto hedge narrative, but the market is also showing profit-taking whenever price rallies into resistance.

RWA and tokenized Treasuries: crypto’s cash-yield hedge

This is the most important missing piece in the 2026 inflation trade.

Tokenized Treasuries are not a pure inflation hedge like TIPS, and they are not a debasement hedge like Bitcoin. They are crypto’s cash-yield hedge — a way to stay on-chain, stay liquid, and earn Treasury-linked yield while inflation keeps rates elevated.

RWA.xyz shows tokenized U.S. Treasuries at around $15 billion in total value, up 5.66% over last 30 days, with 79 assets, 62,515 holders, and a 3.38% 7-day APY.

The broader RWA market tracked by RWA.xyz stands at $26.71 billion in distributed asset value, while represented asset value is $345.07 billion. Stablecoin value is far larger at $299.30 billion, with more than 241 million holders.

| RWA category | Inflation role | Best use |

|---|---|---|

| Tokenized Treasuries | On-chain cash-yield hedge | Park capital while earning Treasury yield |

| Tokenized money market funds | Institutional liquidity product | Compliant on-chain cash management |

| Tokenized gold | Commodity inflation hedge | Hard-asset exposure inside crypto rails |

| Private credit RWA | Yield product | Higher yield, higher credit risk |

| Tokenized equities/funds | Market-access product | Long-term tokenization adoption trade |

Franklin Templeton’s FOBXX/BENJI shows how this market is evolving. The fund invests at least 99.5% of assets in U.S. government securities, cash, and repurchase agreements backed by government securities or cash. It had $824.62 million in total net assets as of April 30, 2026, with a 3.57% 7-day effective yield as of May 8.

Ondo’s OUSG also sits in this lane, offering institutional investors exposure to short-term U.S. Treasuries with daily yield and instant mint/redemption features. Ondo listed OUSG’s APY at 3.44%.

The inflation-era appeal is obvious: idle stablecoins lose purchasing power, but tokenized Treasury products can at least capture yield while keeping capital inside crypto infrastructure.

Tokenized Treasuries vs stablecoins

Stablecoins are not inflation hedges for U.S. dollar investors. They track the dollar, so they lose real purchasing power when U.S. inflation rises.

The better distinction is:

| Product | What it protects against | What it does not protect against |

|---|---|---|

| Idle USDT/USDC | Crypto volatility and local currency weakness | U.S. dollar inflation |

| Yield-bearing stablecoin products | Idle-cash drag | Issuer, regulatory, and smart-contract risk |

| Tokenized Treasuries | Opportunity cost of sitting in cash | Negative real yields if inflation exceeds returns |

| TIPS | CPI inflation | Crypto-native liquidity needs |

| Bitcoin | Monetary debasement | Short-term rate shocks |

Tokenized Treasuries are therefore not “risk-free crypto.” They carry issuer risk, custodian risk, smart-contract risk, redemption risk, permissioning limits, jurisdiction restrictions, and liquidity risk. But compared with idle stablecoins, they are a much stronger inflation-era parking lane.

Gold and tokenized gold: the cleaner defensive hedge

Gold remains the cleaner hedge when the market is worried about inflation, war, energy shocks, or central-bank credibility. Unlike Bitcoin, gold does not need ETF inflows to prove it is a hedge. Unlike Ethereum, it is not tied to network fees or application demand.

Tokenized gold brings that hedge on-chain. RWA.xyz shows tokenized commodities with a $7.40 billion market cap, $12.50 billion in monthly transfer volume, and more than 192,000 holders.

That makes tokenized gold a useful bridge product for crypto investors who want hard-asset exposure without leaving blockchain rails.

| Asset | Hedge quality | Yield | Volatility | Best role |

|---|---|---|---|---|

| Gold | High | None | Lower than BTC | Defensive hedge |

| Tokenized gold | High, with issuer/custody risk | None | Gold-linked | On-chain commodity hedge |

| Bitcoin | High long-term, unstable short-term | None | High | Debasement hedge |

| Tokenized Treasuries | Medium inflation hedge, strong cash hedge | Yes | Low | Yield-bearing cash defense |

| TIPS | High CPI hedge | Yes | Low/medium | Direct inflation protection |

TIPS: the direct inflation hedge crypto cannot replace

TIPS remain the cleanest direct inflation hedge because their principal adjusts with CPI. Crypto cannot replicate that structure without taking smart-contract, issuer, or market risk.

For conservative capital, TIPS are still more precise than Bitcoin. Bitcoin may outperform during monetary debasement cycles, but TIPS are built to hedge CPI directly.

The iShares TIPS Bond ETF traded near $111.12 on May 13, while SPDR Gold Shares traded near $429.60. These traditional-market proxies show why inflation hedging in 2026 is not only a crypto conversation.

Ethereum: tokenization growth asset, not the first inflation hedge

Ethereum belongs in the inflation article, but not as the top hedge.

ETH is more of a productive crypto-beta asset. It benefits from staking, stablecoin settlement, tokenized finance, Layer-2 activity, and RWA expansion. But it is also more tied to risk appetite than Bitcoin.

In a pure inflation scare, Bitcoin usually gets the “hard money” bid first. Ethereum performs better when inflation fears are paired with liquidity growth, lower real yields, and stronger on-chain activity.

That makes ETH a tokenization and crypto-growth trade, not the first line of defense against CPI.

Bitcoin miners: energy inflation cuts both ways

Energy inflation is directly relevant to Bitcoin miners. April CPI showed energy prices up 17.9% year over year, gasoline up 28.4%, electricity up 6.1%, and fuel oil up 5.8% month over month.

For miners, that creates a margin squeeze unless Bitcoin price rises enough to offset higher power and operating costs.

| Miner factor | Inflation impact |

|---|---|

| Electricity costs | Higher power costs pressure margins |

| Bitcoin price | Higher BTC can offset energy pressure |

| Hashprice | Falls if mining competition rises faster than BTC |

| Treasury strategy | BTC holdings can help if Bitcoin rallies |

| Debt and financing | Higher rates raise capital costs |

That is why miners are not clean inflation hedges. They are leveraged Bitcoin-and-energy businesses.

Crypto stocks: public-market proxies for the inflation trade

Crypto-linked equities are also moving into the inflation trade as investors look beyond tokens for exposure to Bitcoin, ETF infrastructure, stablecoin revenue, and mining economics.

| Stock/category | Inflation-trade role | Main risk |

|---|---|---|

| Coinbase | Trading, custody, ETF infrastructure, stablecoin exposure | Lower volumes during risk-off periods |

| Strategy/MicroStrategy | Leveraged Bitcoin proxy | BTC drawdowns and debt/equity pressure |

| Bitcoin miners | High-beta Bitcoin exposure | Energy costs and hashprice compression |

| ETF issuers/asset managers | Institutional flow proxy | Fee compression and ETF outflows |

| Stablecoin-linked firms | Benefit from high-rate reserve income | Regulation and rate cuts |

Coinbase and Strategy are both macro-sensitive. Coinbase benefits when trading volumes, ETF custody, and institutional demand rise. Strategy remains one of the most aggressive public-market Bitcoin proxies, but that also means its stock can fall harder when Bitcoin weakens.

For miners such as MARA and Riot, inflation is more complicated. A higher Bitcoin price helps revenue, but higher energy costs and tighter financing conditions can hurt margins.

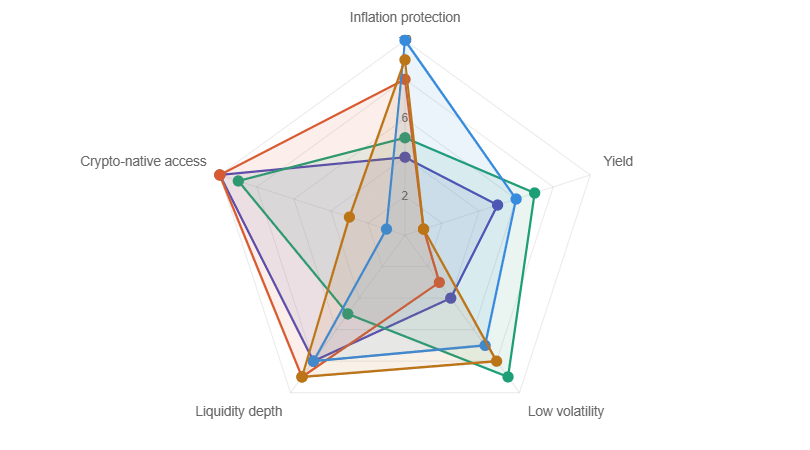

Best hedge assets for 2026

| Rank | Asset | Best role | Why it works | Main weakness |

|---|---|---|---|---|

| 1 | Gold | Defensive inflation hedge | Deep market, crisis demand, hard-asset history | No yield |

| 2 | TIPS | Direct CPI hedge | Explicit inflation adjustment | Less upside |

| 3 | Bitcoin | Fiat debasement hedge | Scarcity, ETF access, global liquidity | Volatile, rate-sensitive |

| 4 | Tokenized Treasuries | On-chain cash-yield hedge | Treasury yield inside crypto rails | Not true CPI protection |

| 5 | Tokenized gold | On-chain hard-asset hedge | Gold exposure with crypto settlement | Issuer/custody risk |

| 6 | Short-duration Treasuries | Cash defense | Yield with lower duration risk | Traditional-market rails |

| 7 | Ethereum | Tokenization growth trade | RWA, stablecoins, staking, DeFi | Risk-asset behavior |

| 8 | Stablecoins | Liquidity hedge | Trading, settlement, dollar access | Lose real purchasing power |

| 9 | Crypto stocks | Public-market crypto beta | Equity access to crypto themes | Rate and earnings risk |

| 10 | Altcoins | High-beta speculation | Upside in risk-on conditions | Weak inflation hedge quality |

Scenario map: what wins under each inflation path

| 2026 scenario | Likely winners | Likely losers |

|---|---|---|

| Hot inflation + hawkish Fed | Gold, TIPS, tokenized Treasuries, short-duration T-bills | Altcoins, miners, high-beta crypto stocks |

| Hot inflation + dovish Fed | Bitcoin, gold, ETH, tokenized gold | Idle stablecoins |

| Falling inflation + rate cuts | BTC, ETH, altcoins, Coinbase, miners | TIPS may lag risk assets |

| Stagflation | Gold, TIPS, Bitcoin, tokenized Treasuries | Growth stocks, weak altcoins |

| Dollar spike | T-bills, tokenized Treasuries, stablecoins | BTC, ETH, altcoins |

| ETF inflow revival | Bitcoin, Strategy, Coinbase, miners | Cash-heavy positions |

| ETF outflow cycle | Gold, TIPS, tokenized Treasuries | BTC beta, miners, crypto equities |

The 2026 inflation hedge playbook

The strongest portfolio logic is not “buy crypto against inflation.” It is more precise:

| Investor goal | Best-fit asset |

|---|---|

| Protect against fiat debasement | Bitcoin |

| Hedge CPI directly | TIPS |

| Reduce shock risk | Gold |

| Stay on-chain and earn yield | Tokenized Treasuries |

| Keep trading liquidity | Stablecoins |

| Capture tokenization growth | Ethereum |

| Add hard-asset exposure on-chain | Tokenized gold |

| Express crypto through equities | Coinbase, Strategy, miners |

| Speculate on risk-on recovery | Select altcoins |

Bitcoin is the best inflation hedge inside crypto, but not the cleanest hedge across all markets. Gold and TIPS still own the defensive lane. Tokenized Treasuries now own the crypto-native cash-yield lane. Ethereum owns the tokenization-growth lane. Stablecoins own liquidity, not inflation protection.

Outlook

U.S. inflation has turned the 2026 crypto market into a macro sorting machine. CPI and PPI are forcing traders to separate hard-money narratives from rate-sensitive risk trades. PCE will decide whether the Fed gets any room to soften. ETF flows will decide whether Bitcoin’s digital-gold story has institutional backing. RWA and tokenized Treasuries will decide how much idle stablecoin capital moves into yield-bearing on-chain products.

The best 2026 hedge is not one asset. It is a layered basket.

Bitcoin is the high-upside debasement trade. Gold is the cleaner defensive hedge. TIPS are the direct CPI hedge. Tokenized Treasuries are the on-chain cash-yield hedge. Stablecoins are liquidity tools. Ethereum is the growth bet on tokenized finance.

That is the real inflation story for crypto in 2026: the market is no longer choosing between Bitcoin and cash. It is choosing between hard money, yield-bearing on-chain dollars, traditional inflation protection, and tokenized real-world assets.

Also Read: How ETFs Are Driving Bitcoin in 2026: Big Players Shaping the Trend