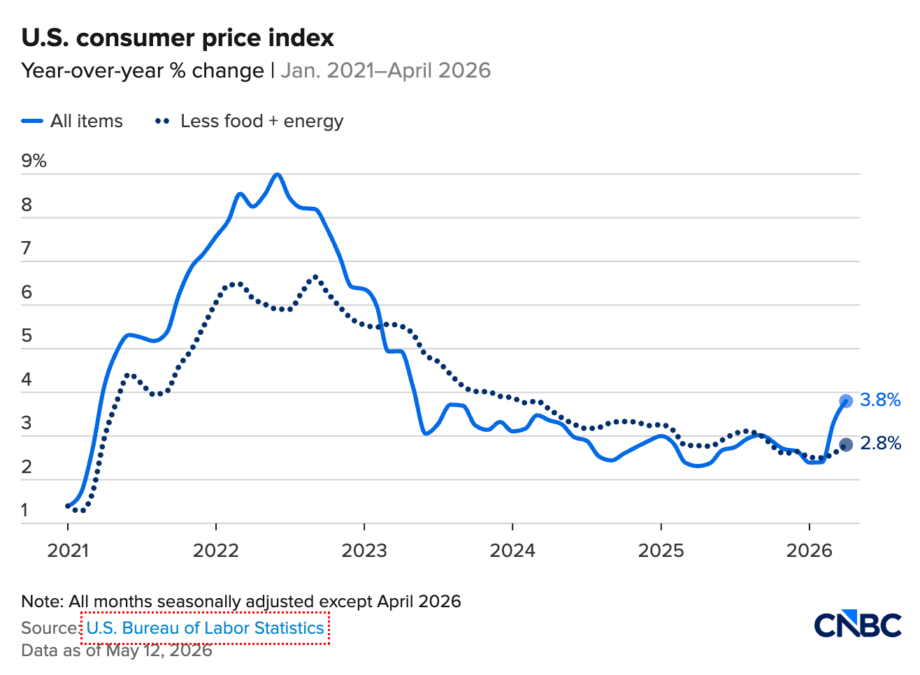

On Tuesday, May 12, the US Bureau of Labor Statistics dropped the kind of number that resets every portfolio conversation: April 2026 headline CPI came in at 3.8% year-over-year — the hottest annual print since May 2023, and a sharp jump from 3.3% in March. Monthly prices rose 0.6%. Core CPI (stripping out food and energy) climbed to 2.8%, also above forecasts.

The driver isn’t a mystery. The energy index alone jumped 17.9% over the past 12 months — the steepest annual gain since September 2022 — with gasoline up 28.4% and fuel oil up 54.3% as the oil shock from the US-Israel conflict with Iran (precipitated by late-February 2026 US-Israeli strikes that broke out into open war by March) rippled through every supply chain. Food at home posted its biggest monthly gain since August 2022. Even shelter inflation accelerated.

Real average hourly wages fell 0.5% for the month and are down 0.3% year-over-year. Translation: workers are getting poorer in real terms, and anyone holding plain dollar cash is watching purchasing power evaporate at roughly the speed of a four-and-a-half-year T-bill yielding less than CPI. For the first time in three years, Americans’ wages are no longer outpacing inflation.

CME FedWatch traders, who started 2026 pricing in multiple cuts, are now openly debating whether the Fed will cut at all this year. A growing minority is even pricing in the tail risk of a hike.

This is the macro setup. Now here’s what’s actually happening on-chain — and why “smart money” stopped waiting for the Fed months ago.

What Smart Money Is Actually Doing (And It’s Not Buying More Bitcoin)

Bitcoin (BTC) still has its bid. But the more interesting capital flow in 2026 isn’t into BTC — it’s into two boring, yield-bearing, regulation-blessed corners of the crypto market:

- EUR-denominated stablecoins (currency diversification away from a structurally weakening dollar)

- Tokenized real-world assets — especially short-duration US Treasuries (real yield that beats CPI, settled on-chain, liquid 24/7)

Neither is speculative. Both are now infrastructure. And both crossed major milestones in the last 30 days.

Let’s look at the numbers.

Pillar 1: Tokenized US Treasuries — $15.2 Billion and Climbing

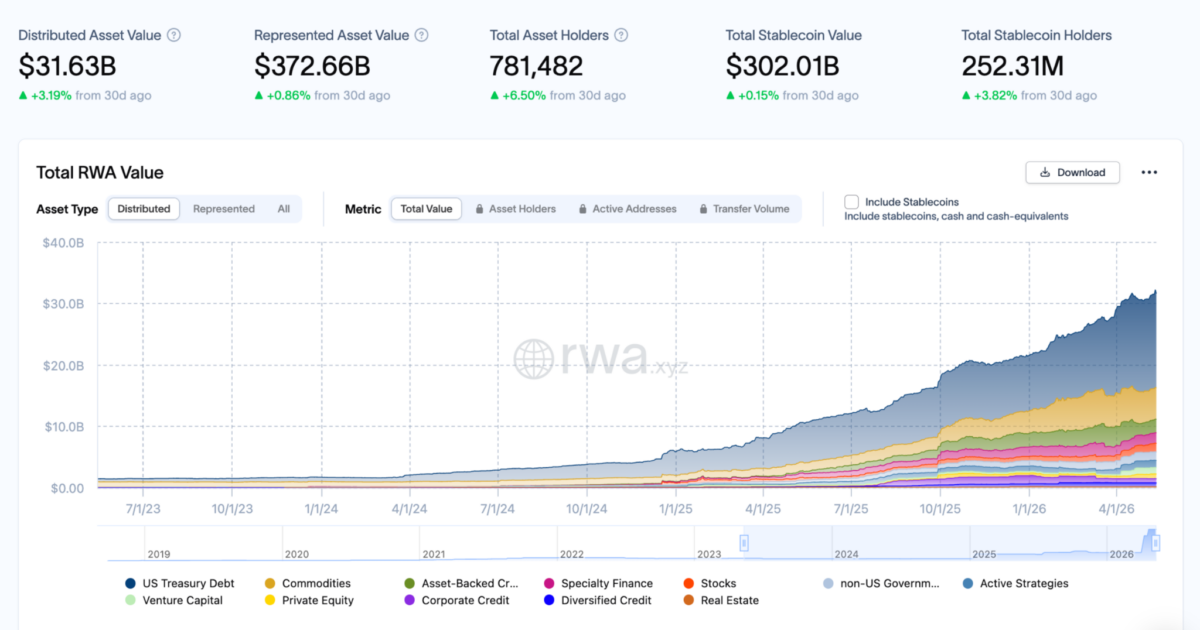

The tokenized US Treasury market hit $15.20 billion at the start of May 2026, according to on-chain data from rwa.xyz — adding $1.06 billion in the prior 30 days alone. The broader tokenized RWA market (excluding stablecoins) sits at roughly $19–26 billion depending on what you count, after reportedly more than tripling year-on-year.

Why it works as an inflation hedge: these tokens pass through the yield on actual short-dated Treasury bills, repos, and government money market positions — settled on a blockchain, redeemable daily, and usable as collateral inside DeFi. The sector’s weighted average APY clocked in around 3.36% over the past week (sector-wide), but flagship products are paying meaningfully more.

The five funds doing the heavy lifting

| Fund | Issuer | TVL (May 2026) | Notable |

|---|---|---|---|

| USYC | Circle (acquired Hashnote) | ~$2.91B | Largest tokenized Treasury product. Live on Ethereum, Solana, BNB Chain |

| BUIDL | BlackRock (via Securitize) | ~$2.58B | Available on 8 blockchains; widely used as DeFi collateral |

| USDY | Ondo Finance | ~$2.14B | ~4.5–5% APY; tax-efficient price-accrual model; non-US retail accessible |

| BENJI | Franklin Templeton | ~$2.05B | Operates across 7+ networks; on-chain shareholder records |

| JTRSY | Janus Henderson (Anemoy) | ~$1.24B | Institutional |

Those five alone account for roughly $10.9 billion of the market. RWA.xyz tracks 71 distinct tokenized Treasury assets held across almost 58,700 unique wallets.

Why this isn’t a crypto sideshow anymore

Three events in the first 1O days of May made the institutional thesis impossible to dismiss:

- May 5: Bullish (NYSE: BLSH) announced a $4.25 billion acquisition of Equiniti, one of the world’s largest stock transfer agents — explicitly to plug the “transfer agent gap” that has blocked tokenized equities at scale.

- May 6: Ondo, JPMorgan’s Kinexys, Mastercard’s Multi-Token Network, and Ripple’s XRP Ledger completed the first near real-time cross-border redemption of a tokenized Treasury (Ondo’s OUSG), settling in under 5 seconds. Cross-border settlements like this typically take one to three business days through correspondent banking.

- The DTCC’s tokenization rollout is on the calendar for July 2026, with BlackRock, Goldman Sachs, Morgan Stanley, Nasdaq, NYSE, and Ondo in the working group.

This is the part the 2024-era “RWA narrative” articles got wrong: the infrastructure isn’t coming — it’s arriving in production, in sequence, in 2026.

Pillar 2: The Quiet Boom in Euro Stablecoins

Here is the statistic that should be on every macro desk’s wall:

Circle’s EURC went from 17% to roughly 41–50% of total euro stablecoin market capitalization in the 12 months following MiCA’s December 30, 2024 enforcement deadline. EURC’s market cap stood at approximately $424–449 million in Q1 2026, with circulating supply near 390 million tokens. Circle reports EURC supply grew 4x between January 2025 and March 2026.

The aggregate euro stablecoin market has roughly doubled to $680 million+ a year after MiCA took effect as per Decta’s 2025 report — still a fraction of the ~$300 billion USD-pegged stablecoin market, but the growth rate and composition are what matter. Monthly euro stablecoin transaction volume rose nearly 900% post-MiCA, from about $383 million to $3.83 billion.

Why EUR stablecoins hedge USD inflation

Three reasons, in order of importance:

- The dollar is structurally forecast to weaken. ABN AMRO’s BEER model puts the “fundamental value” of EUR/USD at 1.23 — the highest since 2017. MUFG, Goldman, and Bethmann Bank all see EUR/USD reaching 1.20–1.25 by year-end 2026, driven by a Fed expected to ease more than the ECB and persistent US fiscal and current-account deficits. EUR/USD already climbed from 1.04 to roughly 1.17–1.18.

- MiCA hardened the asset class. Under MiCA, e-money tokens must be issued by licensed credit or e-money institutions, hold 1:1 liquid reserves, and offer par redemption. Three named EUR-stablecoin competitors depegged 3–6% during late-2025/early-2026 volatility. EURC, fully reserved with monthly Big Four attestations, never moved more than a fraction of a cent.

- Real plumbing is being built. Circle’s French entity got MiCA CASP authorization (custody and transfer services across the EEA) on April 20, 2026. EURC is now spendable at 40 million+ Ingenico point-of-sale terminals via WalletConnect Pay. Wirex and Visa settle on Stellar via EURC. ClearBank Europe integrated EURC in April. This is what “regulated euro IBAN on-chain” actually looks like.

A regulatory note worth understanding: Under the GENIUS Act (signed July 2025) and similar US frameworks, stablecoin issuers cannot pay passive deposit-like yield directly to holders. Holders earn yield by deploying stablecoins through separate DeFi protocols (Morpho integration is now live for EURC). This is why this analysis treats EUR stablecoins as a currency exposure, not a yield-bearing instrument — that distinction matters for both tax treatment and risk framing.

The EUR stablecoin shortlist

- EURC (Circle) — dominant, MiCA-compliant, multi-chain (Ethereum, Base, Solana, Stellar, Avalanche, World Chain), monthly attestations.

- EURCV (Société Générale) — bank-issued, growing through DeFi lending integrations (Morpho).

- EURS (Stasis) — one of the oldest, MiCA-ready; saw ~644% gains in 2025.

- EURA / EUROe / EURR — institutional-leaning alternatives.

A note of honesty: EURC’s dominance is partly the result of regulation clearing the field rather than product superiority alone. That makes it a bet on European policy continuity as much as on Circle.

The Combined Playbook: How the Two Pieces Fit Together

Here’s the structural trade institutional desks are running in May 2026:

| Allocation Sleeve | Instrument | Role | Realistic Yield/Return |

|---|---|---|---|

| Defensive cash (USD) | USDC, USYC, BUIDL | Liquidity + Treasury yield | ~3.3–4.8% APY |

| Currency diversification | EURC (sometimes EURCV) | Hedge USD depreciation | Variable; FX upside if EUR/USD rises |

| Real yield core | Ondo USDY, OUSG, BENJI | Long-hold, tax-efficient yield | ~4.5–5% APY |

| Inflation-correlated | Tokenized gold (PAXG, XAUT) | Tail hedge | Spot gold exposure |

A common allocation framework circulating among crypto-native hedge fund desks: roughly 70% USD-stable instruments / 30% EUR-stable for the dry-powder sleeve, with the productive portion concentrated in tokenized Treasuries rather than idle stablecoins. This isn’t a recommendation — it’s a snapshot of what’s actually being run.

The thesis is mechanical:

- Treasury yields at ~4.5–5% on USDY beat current CPI by a hair on a nominal basis and beat core CPI by ~200 bps.

- If EUR/USD moves from 1.17 toward 1.23 over 12 months as ABN AMRO and others model, that’s roughly a 5% currency gain on the EUR sleeve — on top of any euro DeFi yield earned.

- Both legs settle on-chain, are usable as DeFi collateral, and require no banking-hours coordination.

That combination — yield that matches inflation plus optionality on dollar weakness — is hard to replicate in traditional accounts at the same speed, with the same composability, and at retail-friendly minimums.

How a Retail Investor Can Actually Mirror This (Step by Step)

A realistic path, not a sales pitch:

- Set up custody. A hardware wallet (Ledger or Trezor) for anything over a few thousand dollars; MetaMask, Phantom, or Coinbase Wallet for active use. Do not skip the hardware wallet step for sizable positions.

- Complete KYC on at least one MiCA-compliant on-ramp (Coinbase, Kraken, Bitstamp) and one US-compliant ramp if you need both currency exposures.

- Buy your stablecoin sleeve. EURC is available on Coinbase, Uniswap, and a growing list of European exchanges. USDC for the dollar leg.

- Choose your Treasury exposure based on your jurisdiction:

- Non-US retail: Ondo USDY has the lowest accessible minimums and a price-appreciation (tax-friendlier) yield mechanism.

- Accredited US: Ondo OUSG ($5,000 minimum on Ethereum) or Franklin BENJI.

- Qualified institutions: BlackRock BUIDL ($5M minimum) or Circle USYC.

- Retail real-estate exposure (separate category): RealT starts at ~$50 per fractional share.

- Verify yield, redemption terms, and chain. Daily NAV accrual vs. rebasing affects how it shows up in your wallet and how it’s taxed. Read the offering memorandum.

- Monitor with neutral dashboards. rwa.xyz for TVL and product comparisons; DeFiLlama for protocol risk; the issuer’s monthly attestation for reserve verification.

Start small. Treat the first allocation as tuition.

The Risks That Don’t Make the Marketing Decks

Anyone selling this strategy without these caveats isn’t selling the strategy honestly.

- Smart contract risk is real and uninsurable. Even audited contracts fail.

- Issuer/custodian counterparty risk. Treasury tokens are claims on a fund holding the underlying. If the issuer’s custody or accounting breaks, the token does too.

- Peg risk on EUR stablecoins. EURC has held its peg flawlessly. Three competitors did not in the past 18 months. This is a “stick to the proven issuer” market.

- Regulatory whiplash. MiCA is still being implemented unevenly across member states, and the US Reg D/Reg S structures used by most RWA products limit on-chain composability for US persons. From March 2026, EU custody/transfer services for e-money tokens may require both MiCA and PSD2 authorization — doubling some compliance costs and pricing in some smaller issuers.

- Liquidity in stress. Secondary markets for tokenized assets have improved dramatically but are not as deep as their off-chain equivalents during a sharp drawdown.

- Yield is a function of Fed policy. If the Fed actually cuts aggressively (a tail scenario right now), Treasury-token yields fall in lockstep. The currency-diversification leg becomes more important in that world; the yield leg becomes less so.

- Tax complexity. Every token, every chain, every redemption can be a taxable event depending on jurisdiction. Get an accountant who has seen these structures.

This is informational analysis, not investment advice. Crypto investments — even the conservative-looking ones — can result in total loss. Size positions accordingly.

What to Watch in the Next 60 Days

Three calendar items that will move this market more than anything else:

- May CPI release: June 10, 2026. Another hot print and the Fed cut narrative dies entirely. A cooler print reopens the door.

- June 16–17 FOMC: Reportedly Powell’s last meeting before the chair transition; the new chair’s dot plot is the first formal read on 2026 rate path.

- DTCC tokenization rollout: July 2026. If it ships on schedule, expect another step-change in institutional RWA inflows. If it slips, the narrative cools.

The longer game — and this is where the $15B Treasury number connects to a bigger story — is the slow migration of fixed-income settlement from T+1 in correspondent banking to T+0 on programmable rails. Each milestone, each integration, each successful regulatory clearance compounds the case.

The Bottom Line

April’s 3.8% inflation print is not a one-off. It’s a confirmation that the post-2022 disinflation trade is over for now, and that anyone holding non-yielding USD is losing about half a percent of real wealth a month. Smart money has already done the math: dollar-pegged on-chain Treasury exposure for the income, euro stablecoins for the optionality, and tokenized RWAs as the structural bet on how the next decade of fixed-income settlement actually clears.

The tools are live. The yields are real. The regulators — finally — caught up.

The question isn’t whether this playbook works. It’s whether you’ll deploy it before the next CPI print rewrites the conversation again.

Also Read: US Inflation and Crypto 2026: Best Hedge Assets Ranked

FAQs

Is Bitcoin still useful as an inflation hedge in this environment?

Bitcoin remains a high-beta growth asset and a long-horizon monetary hedge. It does not behave like a coupon-paying inflation hedge in the short run. The 2026 institutional pattern is BTC for growth + RWAs and EUR stables for capital preservation, not BTC alone.

Can a US retail investor buy BUIDL or USYC directly?

Generally no — BUIDL requires qualified-purchaser status and a $5M minimum; USYC has institutional access requirements. US accredited investors can access OUSG ($5,000 min). Non-US retail has wider access to Ondo USDY. Always verify eligibility for your jurisdiction.

How safe is EURC compared to USDC?

Both are issued by Circle with the same full-reserve model, monthly Big Four attestations, and MiCA compliance. EURC is smaller and therefore has thinner secondary market liquidity on some platforms — that’s the main structural difference.

What’s the difference between a yield-bearing stablecoin and a tokenized Treasury fund?

Mechanically, often very little — both are claims on a portfolio of short-dated government debt. Legally and tax-wise, the structures differ (note vs. fund share vs. e-money token), and that affects redemption rights, transferability, and how DeFi protocols can use them. Read each offering doc.

Note: Under the GENIUS Act, payment stablecoins cannot pay passive yield directly to holders, so what passes for “yield-bearing stablecoin” is usually a tokenized money market fund (like USDY or BUIDL) rather than a true stablecoin.

What if EUR/USD doesn’t rise as forecast?

Forecasts from Goldman, MUFG, ABN AMRO, and others cluster around 1.20–1.25 for year-end 2026, but Wells Fargo’s alternative scenario sees 1.12 if US data re-accelerates. The euro leg is a probabilistic hedge, not a guaranteed gain. Size it accordingly.

Are tokenized real estate or private credit worth adding?

They offer higher headline yields (8–17% in some private credit pools) but materially higher risk: thinner liquidity, longer lock-ups, and real default exposure. Treasuries are the conservative core; private credit and real estate are the satellite, not the foundation.