The ASEAN region continues to solidify its position as one of the world’s most dynamic crypto landscapes. With a young, tech-savvy population, rising remittance needs, and accelerating regulatory clarity across key markets, the region is experiencing robust on-chain growth.

Countries like Indonesia and Vietnam are emerging as high-potential markets, while established hubs such as Singapore and Hong Kong are setting global benchmarks for institutional and retail integration.

In an insightful conversation with The Crypto Times, Diederik Van Wersch, Regional Sales Director for ASEAN and Hong Kong at Chainalysis, shares his perspectives on the rapidly maturing crypto landscape.

Drawing from his extensive experience working with governments, financial institutions, and law enforcement, Van Wersch discusses shifting institutional attitudes, key market trends for 2026, regional growth dynamics, the rise of stablecoins, and the future of crypto infrastructure across Asia and beyond.

Question

From Containment to Participation: The Institutional Shift

The Crypto Times

You’ve spent several years at Chainalysis working closely with governments, financial institutions, and law enforcement. How has the institutional attitude toward crypto evolved during your time there — and what was the inflection point where you felt the conversation fundamentally shifted?

When I joined Chainalysis, the dominant institutional posture toward crypto was containment. Governments wanted to understand the risks, law enforcement needed tools to follow the money, and most financial institutions treated digital assets as a reputational hazard to be avoided. The conversations were almost entirely about what could go wrong.

That has fundamentally changed. Today, the conversations I have with banks, regulators, and government agencies across ASEAN and Hong Kong are about how to participate — how to build compliant on-ramps, how to integrate stablecoins into payment infrastructure, how to license and supervise rather than restrict. The question has moved from “should we engage with crypto?” to “how do we do it responsibly and competitively?”

The question has moved from ‘should we engage with crypto?’ to ‘how do we do it responsibly and competitively?’

Diederik Van Wersch, Chainalysis

Question

The Convergence Defining 2026

The Crypto Times

If we look at the current trends, is there any of Chainalysis’s on-chain data surfacing right now that you think deserves more attention than it’s getting?

I’d say it’s the convergence of stablecoins, AI, regulatory implementation, and institutionalization. What makes 2026 distinctive is not any single trend in isolation but the fact that all of these forces are colliding at once and reinforcing each other.

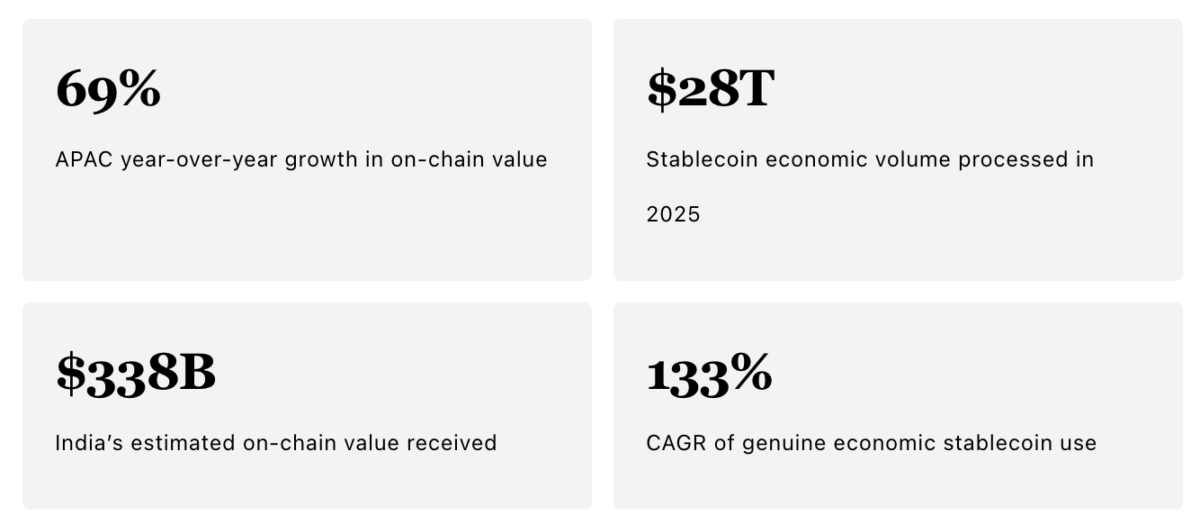

Chainalysis data found that stablecoins processed $28 trillion in real economic volume in 2025 and are on a trajectory that could see them rival Visa and Mastercard’s off-chain transaction volumes within the next decade. That growth is pulling banks and payment companies on-chain, which in turn demands regulatory clarity.

Regulators across Asia, the Middle East, and the U.S. are responding — Hong Kong, Singapore, and the UAE all now have or are developing stablecoin-specific frameworks. Meanwhile, AI is being deployed by both sides of the equation: bad actors are reportedly using it to industrialize fraud and social engineering, while investigators and compliance teams are using it to automate detection, trace funds faster, and scale their operations.

It’s the convergence of stablecoins, institutional entry, regulatory implementation, and AI that defines this moment. No single keyword captures 2026 — which is exactly why it’s such a pivotal year.

Question

Where the Geographic Center of Gravity Is Moving

The Crypto Times

Drawing from Chainalysis’s Global Crypto Adoption Index and your regional work, how is the geographic center of gravity in crypto shifting heading into 2026? Which regions are accelerating, and which are losing ground? Also, beyond the well-known hubs, which underrated jurisdictions are you watching closely as the next wave of crypto activity?

APAC emerged as the fastest-growing region for on-chain crypto activity, with a 69% year-over-year increase in value received. Within the region, several markets stand out.

India is number one on our Global Crypto Adoption Index across every subindex — retail, CeFi, DeFi, and institutional. With $338 billion in estimated value received, India’s market combines grassroots adoption, a massive diaspora driving remittance demand, and a thriving fintech ecosystem that makes crypto integration natural. What happens with India’s regulatory evolution will have outsized implications for the global market.

Japan saw the strongest growth among APAC’s top five markets — 120% over the past year — driven by regulatory reforms, planned crypto tax changes, and the licensing of its first yen-backed stablecoin issuer. After years of being relatively subdued, Japan is showing serious renewed momentum.

Indonesia is growing rapidly at 103% year-over-year and is one of the fastest-growing crypto markets in Southeast Asia. The combination of a young, mobile-first population and evolving regulatory clarity makes it one to watch.

And I’m watching Vietnam closely as well — it may have “only” grown 55%, but that’s because crypto is already deeply embedded in everyday financial activity there, from remittances to gaming to savings. It’s a market where crypto has achieved genuine utility.

Question

Hong Kong vs Singapore vs Dubai: Different Hubs, Different Wins

The Crypto Times

Hong Kong vs Singapore vs Dubai: Hong Kong has aggressively positioned itself as Asia's crypto hub. How would you assess its progress against Singapore and Dubai — and importantly, are these hubs competing for the same thing, or are they winning in different segments (such as institutional capital, retail, builders, infrastructure)?

Each of these markets is competing on slightly different terrain, and the gaps are widening as they move from designing and building frameworks to actually implementing them.

Singapore remains the most mature. The Monetary Authority of Singapore (MAS) has an activity-based regime under the Payment Services Act that now covers consumer protection, technology risk, and stablecoin-specific rules well beyond the original AML/CFT focus. MAS has proposed letting banks hold regulated stablecoins on public blockchains with lower capital requirements and is also piloting tokenized government bills and wholesale CBDC settlement. This shows they are prepared to move at a pace into real payment and settlement infrastructure.

Hong Kong moved quickly from sandbox to statute. The Stablecoins Ordinance is in place, and this April the HKMA granted its first stablecoin issuer licenses to HSBC and a Standard Chartered-led consortium. The fact that these went to GSIBs, not crypto-native issuers, tells you everything about Hong Kong’s approach: institutional-first, tightly supervised, and focused on building credibility. HSBC plans to put its stablecoin directly into PayMe, reaching over three million users, which is a potentially important chapter in the on-chain payments story.

In the Middle East, the UAE has gone some way towards turning stablecoins into a regulated payments infrastructure. The Central Bank’s payment token framework limits merchant payments to licensed dirham backed tokens, while VARA, ADGM, and DIFC each run tailored regimes. This multi-regulator model has the potential for speed and flexibility, but with the potential for a confusing overlap. A key test as far as payments are concerned is coming in September when the Central Bank’s compliance deadline for payment tokens kicks in.

The execution philosophies are clear: Singapore leads on regulatory depth and institutional integration; Hong Kong, on bank-led credibility and retail reach; and the UAE on speed and commercial flexibility. But one thing that will separate all of these markets is how they tackle financial integrity.

Hong Kong is requiring stablecoin issuers to monitor secondary market activity, not just their direct counterparties, leveraging the transparency that public blockchains offer in a way traditional AML regimes can’t. As stablecoins move into mainstream payments, countries that take this risk seriously will be the ones that win and keep serious institutional capital.

Question

How Stablecoins Are Reshaping Cross-Border Flows

The Crypto Times

Stablecoins have quietly become one of crypto's biggest stories—settlement volumes now rival major payment networks. From Chainalysis's vantage point, how is stablecoin adoption reshaping cross-border flows, especially in emerging markets like India and Southeast Asia?

Stablecoins have entered the stage of payment infrastructure, and the data makes this clear. Stablecoins processed $28 trillion in adjusted economic volume in 2025, and when we filter out trading and speculative activity to focus on genuine economic use—payments, remittances, and settlement—stablecoin volumes are growing at a 133% compound annual growth rate.

The strategic moves by major financial institutions confirm this shift. Stripe’s acquisition of Bridge and Mastercard’s partnership with BVNK are not bets on trading volume; they are bets on payments infrastructure.

In markets across Southeast Asia, the Middle East, and Latin America, we are already seeing stablecoins used for cross-border B2B settlement and remittances at a fraction of the cost and time of traditional rails.

That said, the transition is still early. For stablecoins to fully realize their potential as payment infrastructure, the industry needs regulatory frameworks that cover the full lifecycle. This goes beyond issuance and should include distribution, circulation, and integration into existing payment and settlement systems. That’s the work happening now, and it’s why we’re so focused on helping institutions navigate this transition with the right compliance and risk management tools.

Question

The Most Under-Reported Number in Crypto

The Crypto Times

Is there a surprising data point or pattern from Chainalysis's research that your team finds genuinely fascinating but rarely makes it into mainstream coverage? Something that would make our audience see the space differently?

One data point that deserves far more attention is how small the share of illicit activity actually is relative to total on-chain volume. Chainalysis data consistently shows that illicit transactions represent a small fraction of overall cryptocurrency activity — and that share has remained low even as the market grows.

The overwhelming majority of on-chain activity is legitimate: payments, savings, remittances, institutional settlement, and DeFi participation. That matters because the mainstream narrative still tends to frame crypto primarily through the lens of crime and fraud. The reality is that blockchain’s transparency makes illicit activity more traceable, not less — which is exactly why law enforcement agencies around the world have become some of the strongest advocates for on-chain analytics.

We’ve helped trace and recover billions of dollars in illicit funds precisely because public blockchains provide a level of visibility that traditional financial rails simply cannot match.

The same transparency that makes people nervous about crypto is actually its greatest strength for financial integrity.

Diederik Van Wersch, Chainalysis

Interview conducted by The Crypto Times. Responses are attributed to Diederik Van Wersch, Regional Sales Director, ASEAN and Hong Kong, Chainalysis.

Also read: CoinSwitch CEO Says Unlocking India’s Gold is Bigger than Just Crypto