A new working paper from researchers at Stanford University and Singapore Management University has uncovered systematic settlement manipulation in one of the fastest-growing segments of the prediction market industry.

Titled “Settlement Manipulation in Prediction Markets,” the study by David Dai, Ruizhe Jia, and Shihao Yu analyzes Polymarket’s five-minute Bitcoin binary contracts launched in February 2026. Using on-chain transaction data and Binance spot market activity, the authors document how traders exploit the short settlement window to influence outcomes, transferring millions from retail participants to a small group of manipulators.

“In the final seconds before settlement, Binance spot order flow spikes, resulting in price movements that revert shortly after settlement,” authors claimed. “Clearly, this is a transitory push to manipulate the spot price, not trading on information.”

The paper provides a rigorous empirical and theoretical framework showing that asset-price prediction contracts with very short horizons create structural incentives for manipulation. Rather than improving price discovery as traditional economic theory suggests for event contracts, these ultra-short Bitcoin bets appear to degrade information quality in the underlying market while enriching sophisticated players at the expense of ordinary traders.

Evidence of Last-Second Price Pushes

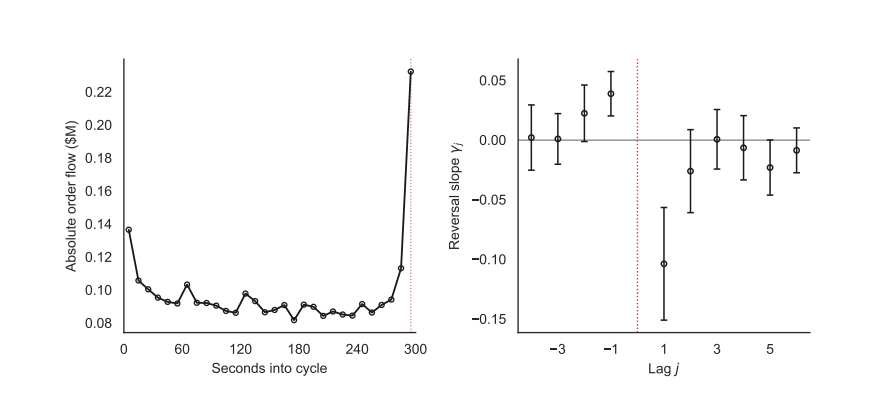

The core empirical finding centers on trading patterns immediately before contract settlement. After the five-minute Bitcoin contract launched on February 12, 2026, Binance spot order flow in the final 10 seconds before each close spiked dramatically—roughly 50% above pre-launch levels.

This surge coincided with heightened volatility, followed by rapid price reversals within seconds after settlement. Such reversals strongly indicate transitory pushes rather than information-based trading, as genuine news or fundamental shifts would persist.

The researchers classify approximately 1,600 cycles in the top decile of abnormal final-second net order flow as likely manipulated. In these windows, especially those where the contract price was near even, manipulative flows flipped the outcome 65% of the time, compared to 41% in normal cycles. Even in cycles where the market assigned 90-100% probability to one side, pushes reversed the result 34% of the time versus just 1% otherwise. The effect is concentrated in thin-liquidity periods—overnight hours and weekends—where smaller volumes move prices more easily.

Notably, the manipulation signature largely disappears in Polymarket’s longer fifteen-minute contracts, supporting the paper’s theoretical insight: longer horizons allow more natural price discovery, reducing the impact of any single push. The five-minute design, which resolves against a Chainlink oracle heavily influenced by Binance pricing, creates a precise, gameable target.

Retail Losses and Profiteer Identification

The study identifies 821 wallets—roughly one in 300 active traders in this contract—as consistent beneficiaries during manipulated cycles. These accounts captured approximately $8.2 million in profits over the two-month sample, breaking even or losing elsewhere. Market makers, who quote passively, largely stayed flat and avoided significant exposure.

Retail traders bore the brunt, funding about 93% of the losses outside of maker activity. They ended up on the losing side of manipulated cycles 65% of the time, versus 48% in normal ones. The model developed in the paper explains this as a wealth transfer: manipulators buy contracts and push the spot price, while liquidity providers in the prediction market shade quotes against anticipated manipulation, harming uninformed participants.

The authors argue this dynamic also harms overall market efficiency. While manipulation increases liquidity in the spot market by reducing adverse selection for makers (uninformed pushes look like random liquidity), it decreases the informativeness of the settlement price. This creates a troubling trade-off for prediction platforms aiming to offer both hedging tools and accurate forecasts.

Implications for Market Design and Regulation

The findings arrive as prediction markets explode in volume, with asset-price contracts becoming a major driver. Polymarket and competitors have seen billions in turnover, attracting regulatory attention and mainstream interest. However, the paper warns that short-horizon asset bets raise exactly the manipulation risks that regulators like the CFTC seek to prevent in designated contract markets.

The proposed remedy is straightforward: lengthen contract horizons. Evidence shows the fifteen-minute version exhibits far weaker manipulation signals. Platform designers could also explore alternative oracles, volume-weighted settlement, or mechanisms that obscure precise timing targets.

This research underscores a broader tension in decentralized finance. While blockchain transparency enables precise detection of trading patterns—something impossible on traditional exchanges—it also reveals how retail enthusiasm for high-frequency crypto bets can be exploited.

As more platforms consider equity-index contracts and regulators evaluate approvals, the study offers timely evidence that market design details matter profoundly. Shorter is not always better when the underlying can be moved in seconds.

Also read: Will Bitcoin Reclaim Its All-Time High of $126K by End of 2026?