CASHCAT’s perpetual futures on Hyperliquid collapsed more than 60% in a matter of minutes, wicking from above $0.190 to roughly $0.080 before rebounding, while the Robinhood Chain memecoin’s spot price never followed it down.

The Crash Happened in Derivatives, Not the Token

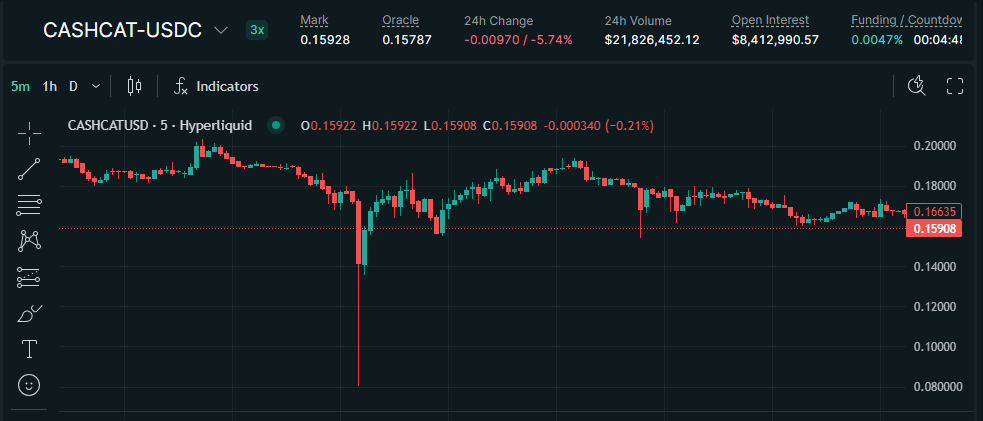

The token itself barely registered it. CASHCAT is down 5.74% over 24 hours, with the perp marked at $0.15928 and the oracle index, which tracks the underlying spot market, at $0.15787.

That gap between a 60% wick and a sub-6% daily move is the entire story. During the collapse, the mark price detached from the oracle; the contract fell while the asset it references did not. Holders of the spot token saw a routine down day. The traders who lost money were those holding leveraged longs on a contract that had existed for barely two days.

The recovery has also been partial rather than clean. Price bounced off the wick low but has since drifted, trading near $0.159 against the roughly $0.19 level that preceded the flush.

A Two-Day-Old Perp Market on a Ten-Day-Old Token

Hyperliquid listed CASHCAT perpetual futures earlier this week following community requests, capping the market at 3x leverage with isolated margin. The exchange noted at the time that the listing was not an endorsement of the project.

Those constraints are conservative by memecoin-perp standards, and they undercut the simplest explanation. A 3x cap means a long position is not liquidated until price moves roughly a third against it—this was not a market stuffed with 50x degenerate longs waiting to be flushed.

What it was instead is a very new, very thin derivatives venue attached to an asset that has existed for under two weeks. Isolated margin contained the damage to the positions themselves rather than draining traders’ full account balances, which is the design working as intended. The mark price still had far less depth beneath it than the wick suggests about CASHCAT itself.

Open Interest Is Nearly as Large as Spot Liquidity

The structural problem is visible in the numbers. Open interest on the CASHCAT perp stands at $8.41 million, with $21.83 million in 24-hour contract volume and funding at 0.0047%.

Set that against the underlying market. CASHCAT’s decentralized exchange pair has held roughly $9.8 million in liquidity against a market capitalisation near $188 million.

In other words, the open leveraged exposure on Hyperliquid is close to the entire depth of the spot market beneath it. When a derivatives book approaches the size of the liquidity that anchors its reference price, the mark price has very little to fall back on — which is what a 60% wick on a 3x-capped market looks like in practice.

Trading routes have also multiplied faster than that liquidity has deepened, spanning Robinhood Chain spot, Solana via a bridge, and Hyperliquid perps. More venues on the same thin base does not distribute risk; it accelerates how fast a move in one market forces closures in another.

The Rally That Set It Up

CASHCAT became the flagship token of Robinhood Chain almost immediately after the network’s July 1 mainnet launch, drawing on the “Cash Cat” mascot from Robinhood’s pre-launch history. TCT reported that its TVL passed $100 million within days, as Robinhood Chain recorded more than 141,000 new active wallets on July 8 and daily active addresses near 193,000.

Individual trades became their own marketing. One wallet turned an $838 entry into more than $1 million, a return above 1,180x. Another reportedly converted roughly $86 into $1.6 million.

CEO Vlad Tenev, who days earlier had argued the future of crypto lies in real-world assets, posted that while Robinhood Chain is built for RWAs, “it works great for memes too.” The token’s run continued from there.

The Leverage Lives on a Competitor’s Venue

There is an awkward footnote for Robinhood. The company routes perpetual futures for its own wallet users through Lighter, the decentralized exchange it backed via Robinhood Ventures.

CASHCAT’s leverage market, however, sits on Hyperliquid — the venue The Crypto Times recently reported Robinhood Chain had out-traded on 24-hour DEX volume, $375.15 million to $198.87 million. The flagship asset of Robinhood’s own chain now has its price discovery on derivatives happening somewhere else entirely.

For traders, the lesson from the wick is narrower and more useful than “memecoins are volatile.” The token did not crash. A thin, new contract on top of it did, and the people holding the contract paid for it.

Also Read: How to Buy Meme Coins on Robinhood Chain: A Complete Beginner’s Guide