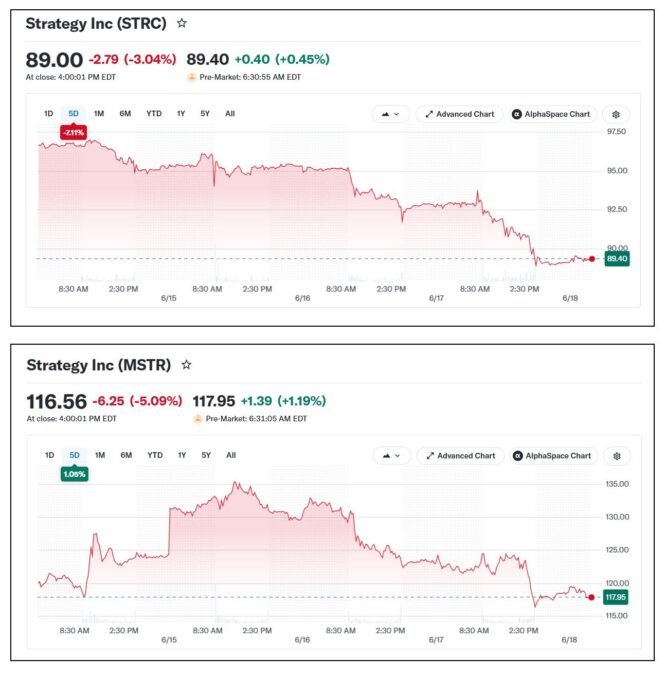

Strategy Inc. (formerly MicroStrategy), long hailed as a pioneer in corporate Bitcoin adoption, finds itself at a crossroads. Its common stock, MSTR, closed at $116.56 on June 17, 2026, down more than 5% in a single session and trading well below its 52-week highs near $457.

This decline coincides with mounting concerns over the company’s flagship financing vehicle STRC—the Variable Rate Series A Perpetual Stretch Preferred Stock. Trading as low as $89 recently—well below its $100 par value—STRC has become a focal point for investors questioning the sustainability of Strategy’s aggressive Bitcoin accumulation approach.

The interplay between MSTR’s volatility and STRC’s struggles highlights the risks embedded in Strategy’s leveraged bet on Bitcoin. With a total of 846,842 BTC on its balance sheet valued at roughly $54 billion (at BTC prices around $64,000–$65,000), the company has transformed from a business intelligence software firm into a de facto Bitcoin yield and treasury vehicle. Yet recent market dynamics, including Bitcoin’s consolidation and competition from rivals like Strive, are testing the resilience of this model.

The Mechanics of Strategy’s Dual-Track Capital Structure

Strategy’s approach relies on a sophisticated capital stack that includes common equity (MSTR), various preferred series, and debt instruments. STRC, launched in mid-2025, was designed as a “Stretch” perpetual preferred stock offering variable dividends tied to market conditions. It aims to trade near its $100 par value, with the dividend rate adjusting monthly (currently 11.50% annualized) to attract buyers when it dips and temper issuance when it rises above par. Proceeds from STRC sales at or above par flow directly into Bitcoin purchases via at-the-market (ATM) programs, creating a self-reinforcing “Bitcoin flywheel.”

This structure has powered remarkable growth. Strategy’s Bitcoin holdings have swelled dramatically, funded not just by equity but by preferred issuances totaling billions. As of mid-2026, the company reports strong coverage metrics: reserves sufficient for multiple years of dividends in some estimates, with only modest BTC appreciation (around 3.1% annually) needed to sustain obligations long-term.

Proponents, including Executive Chairman Michael Saylor, emphasize that the massive BTC treasury—acquired at an average cost near $75,000 per coin—provides a deep liquidity backstop far superior to traditional corporate assets.

However, the model’s sensitivity to Bitcoin price action and investor sentiment has become evident. When STRC trades below par, new issuance slows or halts, forcing reliance on common stock sales (which dilute shareholders) or, in extreme cases, BTC sales.

MSTR’s recent drop reflects this feedback loop, with concerns over STRC depressing the common equity, which in turn signals higher perceived risk in the broader treasury strategy. The stock’s high beta to Bitcoin—often amplified by leverage—means even moderate BTC weakness translates into sharper MSTR declines.

Mounting Scrutiny on Strategy Inc.: Dividend Coverage, Competition, and Cash Reserves

Recent weeks have intensified analyst and investor focus on STRC. The preferred stock hit multi-month or record lows, trading 11% below par despite an effective yield exceeding 12.9% at depressed prices. Key concerns include reduced cash buffers following a $1.5 billion convertible debt repurchase earlier in 2026, which left on-hand liquidity covering roughly 6–7 months of preferred dividends (estimated at $1.5–1.7 billion annually across series).

A small BTC sale of 32 coins in late May marked the first such disposal since 2022 and was intended to “inoculate” markets to the possibility of using holdings for payouts. While negligible relative to the hoard, it fueled narratives of potential forced selling in a downturn.

Critics, including economist Peter Schiff, highlight principal erosion for investors buying above current levels and question whether perpetual preferreds with rising dividend obligations resemble a high-yield trap amid crypto volatility.

“STRC closed at $89. Investors who paid $100 last month are down 11%. The current yield for new buyers is 12.92%,” Schiff said in a latest X post. “If Saylor raises the yield to 13%, he will have to sell even more MSTR at bigger discounts to fund it. If he doesn’t raise the yield, the STRC price will keep falling.”

Additionally, competition has compounded the pressure. Strive’s SATA preferred offering, backed by a smaller BTC treasury, delivers a competitive 13% dividend with daily payouts and has maintained steadier trading near par. Strategy responded by shifting STRC to semi-monthly dividends (approved by shareholders in June 2026) to improve liquidity and stability, but the move has not yet restored full confidence.

Broader market dynamics also played a key role in the scrutiny. Bitcoin’s range-bound trading in the mid-$60,000s has limited upside for leveraged plays like MSTR. Meanwhile, regulatory and macroeconomic headwinds—higher interest rates, tech sector rotation—have weighed on sentiment. Some observers warn of a negative spiral as lower STRC prices raise effective borrowing costs (potentially to 11.75% or more), slowing accumulation and pressuring MSTR’s premium to net asset value (NAV).

Outlook: Resilience Through Bitcoin or the Limits of Leverage?

Despite the scrutiny, Strategy maintains a bullish long-term stance. The company continues aggressive BTC buying when conditions allow and points to its treasury’s scale as a differentiator. Holdings of 846,842 BTC dwarf those of most institutions, and the firm’s “Bitcoin yield” metrics (growth in holdings per share) remain a key investor talking point.

Bullish analysts see MSTR targets well above current levels in a BTC bull market, viewing temporary STRC weakness as a buying opportunity for high-yield exposure with embedded crypto upside. Skeptics, on the other hand, counter that the structure introduces new risks such as dividend ratchets in a prolonged BTC slump could necessitate more sales or dilution, eroding value. The model works elegantly in rising markets but faces stress tests when sentiment sours.

MSTR’s correlation with BTC, combined with capital structure complexities, makes it a high-volatility proxy rather than a pure-play treasury. The MSTR-STRC dynamic offers a case study in innovative corporate finance meeting crypto realities.

Strategy’s experiment has already reshaped how public companies interact with Bitcoin, channeling Wall Street capital into digital assets at scale. Whether it proves durable depends on Bitcoin’s trajectory and management’s ability to navigate the preferred stock mechanics under pressure.

As of June 18, 2026, the market is pricing in caution. The coming months—marked by potential rate decisions, BTC halving’s aftereffects, and Strategy’s ongoing accumulation—will determine if the flywheel accelerates once more or requires recalibration.

Also read: “Bitcoin Rodney” Pleads Guilty in $1.8B HyperFund Crypto Fraud Case