Bought crypto from someone directly? You owe the government 1% of that amount. Not at year-end. Right now.

Most P2P crypto traders in India don’t realize this, but under the Indian tax system, the buyer in every peer-to-peer crypto deal is legally required to deduct 1% TDS from the payment and deposit it with the Income Tax Department. Miss it, and you are looking at interest, penalties, and in extreme cases, prosecution.

On exchanges like CoinDCX or WazirX, the platform handles this automatically. In P2P? That responsibility falls entirely on you. This guide covers exactly how to do it, step by step, for both the buyer and the seller, with every form, deadline, threshold, and penalty explained for FY 2026-27.

Important update for FY 2026-27: The old Section 194S/Form 26QE framework applied under the Income-tax Act, 1961. For transactions where payment or credit happens on or after April 1, 2026, the corresponding VDA TDS provision falls under Section 393(1), Table Sl. No. 8(vi) of the Income-tax Act, 2025, and the filing route is Form 141 Schedule D.

What exactly is TDS on crypto, and why does it exist?

TDS stands for Tax Deducted at Source. It is a mechanism through which the Indian government collects tax at the point of a transaction itself, rather than waiting for the end of the year when you file your Income Tax Return.

For crypto specifically, TDS was introduced through the Finance Act 2022, which added Section 194S to the Income-tax Act, 1961. The purpose was straightforward: the government wanted a paper trail. Before July 2022, crypto transactions were largely invisible to the tax department. There was no built-in mechanism to track who was buying, who was selling, and how much money was changing hands.

Section 194S changed that by making every qualifying crypto transaction leave a traceable record with the Income Tax Department. From April 1, 2026, the legal reference changes under the Income-tax Act, 2025. The 1% VDA TDS obligation continues.

The important thing to understand here is that TDS is not an extra tax. It is an advance payment towards your total income tax liability for the year. When you file your Income Tax Return (ITR) at the end of the financial year, the TDS already deducted gets credited to your account and is adjusted against whatever tax you owe. If the TDS deducted is more than your actual tax liability, you can claim a refund.

As The Crypto Times reported in December 2025, TDS collections under Section 194S crossed Rs 1,095 crore in the first three years of its implementation, clearly showing that the government’s tracking mechanism is working.

Who is responsible for deducting TDS in a P2P transaction?

This is where most confusion starts. On a centralized exchange like CoinDCX, WazirX, or CoinSwitch, the exchange itself handles TDS deduction automatically. You sell your crypto, the platform deducts 1%, deposits it with the government against your PAN, and you get the remaining amount. Simple.

But in a P2P transaction, there is no exchange sitting in the middle handling this for you. The CBDT clarified this explicitly in Circular No. 14 of 2022, and the same practical principle continues under the new law: in a peer-to-peer transaction, the buyer is the person responsible for deducting TDS.

Let that sink in. If you are buying crypto from another person directly, whether through a P2P marketplace, a Telegram group, or a face-to-face deal, you are the one who needs to deduct 1% TDS from the payment and deposit it with the government. The seller does not handle this.

How it works in practice

Say you are buying 1 ETH from another person for Rs 2,50,000. Here is what you need to do:

- Calculate 1% of the total consideration: Rs 2,500

- Deduct Rs 2,500 from the payment

- Pay Rs 2,47,500 to the seller

- Deposit the Rs 2,500 with the Central Government through the prescribed form within the deadline

The seller receives Rs 2,47,500 in hand, and the Rs 2,500 gets credited against their PAN in Form 26AS. They can then claim this as a credit when filing their own Income Tax Return.

When does TDS apply? Understanding the threshold limits

TDS under Section 194S does not kick in on every tiny transaction. There are threshold limits, and they differ based on who you are.

For “Specified Persons”

If you are what the law calls a “specified person,” TDS is only required when the aggregate value of your crypto purchases from a single resident seller exceeds Rs 50,000 in a financial year.

A specified person is defined as:

- An individual or Hindu Undivided Family (HUF) who has no income under the head “Profits and Gains of Business or Profession”

- An individual or HUF whose gross turnover from business did not exceed Rs 1 crore in the immediately preceding financial year

- An individual or HUF whose gross receipts from profession did not exceed Rs 50 lakh in the immediately preceding financial year

In simple terms, if you are a salaried individual with no business income, or a small business owner with turnover under Rs 1 crore, you fall under the “specified person” category, and your threshold is Rs 50,000.

For all other persons

If you are not a specified person, meaning you are a company, a firm, a large business entity, or an individual with business turnover exceeding Rs 1 crore, the threshold drops to Rs 10,000 per financial year.

Important clarifications on the threshold

The threshold is calculated on an aggregate basis across the entire financial year, not per transaction. So if you buy crypto worth Rs 20,000 in April, Rs 15,000 in August, and Rs 20,000 in December from the same seller, your aggregate crosses Rs 50,000 and TDS becomes applicable on the entire amount going forward.

Also, once the threshold is crossed, TDS applies on the full consideration of subsequent transactions, not just the amount exceeding the threshold.

What qualifies as a “Transfer” under section 393(1)?

This is another area where people get confused. Under the old Act, this was discussed under Section 194S. From April 1, 2026, the corresponding VDA TDS reference is Section 393(1), Table Sl. No. 8(vi) of the Income-tax Act, 2025.

A “transfer” refers to a change of ownership of the virtual digital asset. It does not mean moving your own crypto from one wallet to another.

Transfers that attract TDS include:

- Selling crypto for INR (or any fiat currency)

- Exchanging one crypto for another (say, swapping BTC for ETH)

- Using crypto to pay for goods or services

- Gifting crypto to someone (though gift tax provisions under Section 56 may also apply here)

Transfers that do NOT attract TDS include:

- Moving your own crypto between your personal wallets

- Transferring crypto between your own accounts on different exchanges

- Mining rewards (as clarified by courts, since there is no identifiable “payer” in mining)

The special case: Crypto-to-crypto swaps in P2P

This is one of the trickiest scenarios, and the CBDT addressed it directly in Circular No. 13 of 2022 (the full text is available on the Income Tax Department’s circulars page).

When you swap one Virtual Digital Asset (VDA) for another in a P2P deal, both parties are simultaneously a buyer and a seller. Person A is buying VDA “X” and selling VDA “Y.” Person B is buying VDA “Y” and selling VDA “X.”

In this situation, both persons need to deduct TDS on what they are paying (the VDA they are giving up). The CBDT’s exact guidance states that both parties need to pay tax with respect to the transfer of their respective VDA and both need to deduct tax with respect to the transfer of the other person’s VDA.

Since the payment in this case is entirely “in kind” (crypto for crypto, no INR involved), both parties must ensure the tax is deposited in cash with the government before the consideration (the swapped crypto) is released.

Example

Person A gives 1 BTC (valued at Rs 50,00,000) and receives 25 ETH from Person B.

- Person A must deduct 1% TDS on the value of the 25 ETH being received (which is effectively Rs 50,00,000), which equals Rs 50,000, and deposit it with the government.

- Person B must also deduct 1% TDS on the value of the 1 BTC being received (Rs 50,00,000), which equals Rs 50,000, and deposit it with the government.

Both parties deposit Rs 50,000 each with the government. This is over and above the actual swap of the assets.

What is Form 141 and why does it matter for P2P crypto traders?

Before getting into the step-by-step filing process, it is important to understand Form 141 properly because this is the form you will actually be using for any P2P crypto transaction from April 1, 2026 onward.

Form 141 is a unified PAN-based challan-cum-statement introduced under the Income-tax Act, 2025. It replaces four older forms that existed under the 1961 Act: Form 26QB (property purchase TDS), Form 26QC (rent TDS), Form 26QD (contractor/professional payment TDS), and Form 26QE (VDA/crypto TDS). All four have been consolidated into a single Form 141 with four separate schedules.

The four schedules inside Form 141 are:

- Schedule A: TDS on rent paid by an individual/HUF under section 393(1) [Table Sl. No. 2(i)]

- Schedule B: TDS on transfer of immovable property under Section 393(1) [Table Sl. No. 3(i)]

- Schedule C: TDS on payment by Individual/HUF to contractor/professional under Section 393(1) [Table Sl. No. 6(ii)]

- Schedule D: TDS on transfer of Virtual Digital Assets (cryptos/NFTs) under Section 393(1) [Table Sl. No. 8(vi)]

For P2P crypto transactions, Schedule D is the one you need.

As per the official CBDT guidance note on Form 141 (PDF), Schedule D covers consideration paid for the transfer of crypto-assets, cryptocurrencies, NFTs, and similar VDAs.

A few critical things to know about Form 141:

- It is PAN-based, not TAN-based. You do not need a TAN to file it. Your PAN and the seller’s PAN are enough.

- Each Form 141 filing covers only one schedule (one transaction type). You cannot mix a rent payment and a VDA transfer in the same Form 141. If you have both, file two separate Form 141s.

- A single Form 141 can include multiple deductees, but only if all deductees are of the same type (either all corporate or all non-corporate) and have the same month of deduction. If the month of deduction differs, separate Form 141s must be filed even for the same deductee type. If you bought crypto from both a company and an individual in the same month, you need to file separate Form 141s for each deductee type.

- The due date remains the same: within 30 days from the end of the month in which the TDS deduction was made.

- The compliance is governed by Rules 218 and 219 of the Income-tax Rules, 2026.

Form 141 is available exclusively under the Income Tax Act, 2025 tab on the e-filing portal. If you accidentally navigate to the old Act section, you will not find it there.

Step-by-step: How the buyer files TDS on a P2P crypto transaction

Here is the detailed process for the buyer (the person making the payment) in a P2P crypto transaction.

Step 1: Determine if you are a “Specified Person” or not

This determines which form you need to use and what your filing timeline looks like.

If you are a specified person (individual/HUF with no business income, or business turnover under Rs 1 crore, or professional receipts under Rs 50 lakh), you will use Form 141 Schedule D (previously Form 26QE under the old Act).

If you are not a specified person (company, firm, large business), you will need a TAN (Tax Deduction and Collection Account Number), and you will file quarterly returns using Form 26Q.

Step 2: Collect the seller’s PAN

Before you proceed, you need the seller’s Permanent Account Number (PAN). This is critical because:

- If the seller provides PAN: TDS is deducted at 1%

- If the seller does not provide PAN: TDS must be deducted at 20% as per Section 397(2) of the Income-tax Act, 2025

This is a significant jump. Always collect the seller’s PAN before completing a P2P crypto deal.

Step 3: Deduct TDS at the time of payment

TDS must be deducted at the time of credit of the consideration to the seller’s account, or at the time of actual payment, whichever is earlier. You cannot defer this.

Calculate 1% of the total consideration (excluding GST, if any service charges are involved). Pay the remaining amount to the seller.

Step 4: File Form 141 Schedule D on the e-filing portal (for specified persons)

This is the most common scenario for individual P2P traders.

Here is the complete step-by-step process to file Form 141 Schedule D, based on the official Income Tax Department user manual:

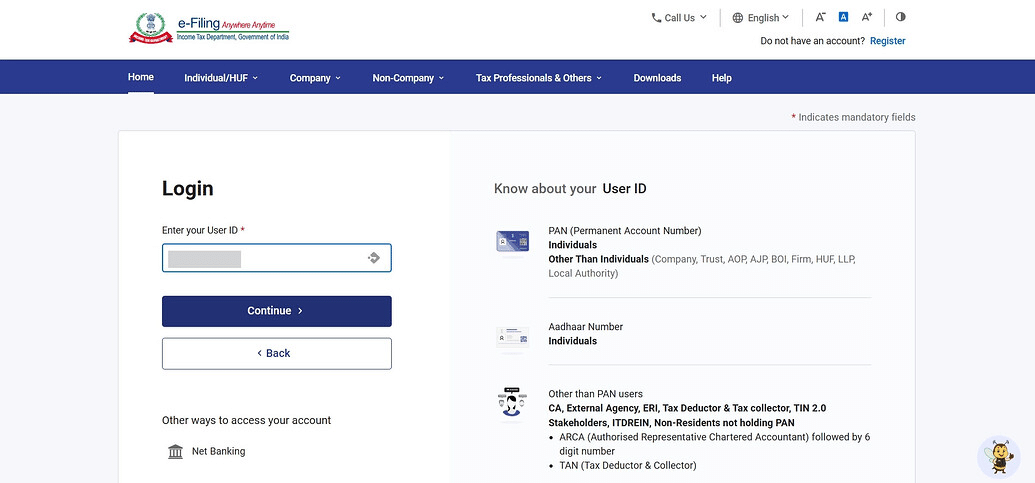

- Log in to the Income Tax e-Filing Portal at incometax.gov.in using your PAN and password

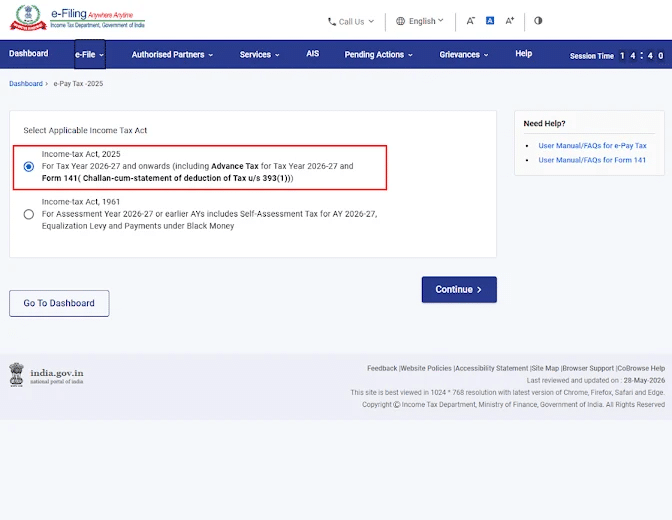

- On the Dashboard, click “e-File” and then select “e-Pay Tax”

- On the Act Selection screen, select “Income-tax Act, 2025.” This is important. Form 141 exists only under the new Act. If you select the old Income-tax Act, 1961, you will not see Form 141 as an option.

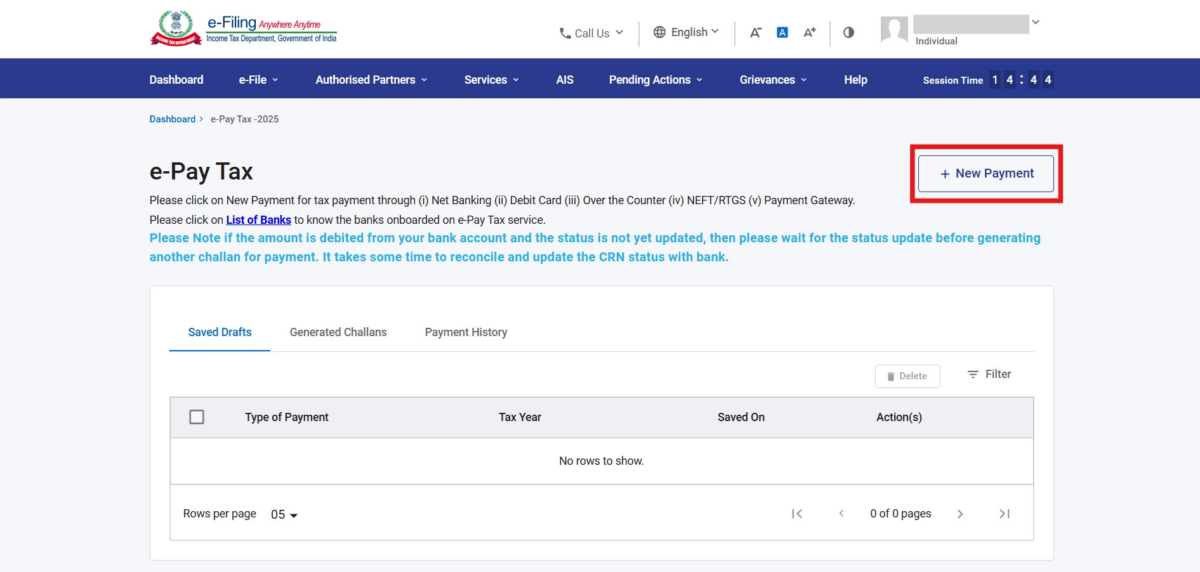

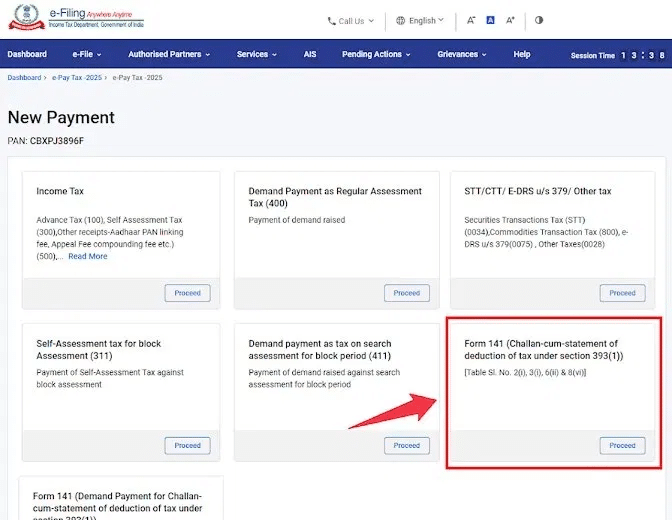

- Click “New Payment” to create a new Challan Reference Number (CRN)

- On the New Payment page, locate the “Form 141 (Challan-cum-statement of deduction of tax under section 393(1))” tile and click “Proceed”

- A pop-up will ask you to select the Nature of Transaction. From the dropdown, select “Schedule D: TDS on payment made by Individual/HUF on transfer of Virtual Digital Asset (VDA) under section 393(1) [Table Sl. No. 8(vi)]”

- Another pop-up will ask you to select the Deductee Type. Choose “Non Corporate Deductee” if the seller is an individual or HUF. Choose “Corporate Deductee” only if the seller is a company. You cannot mix both types in a single Form 141.

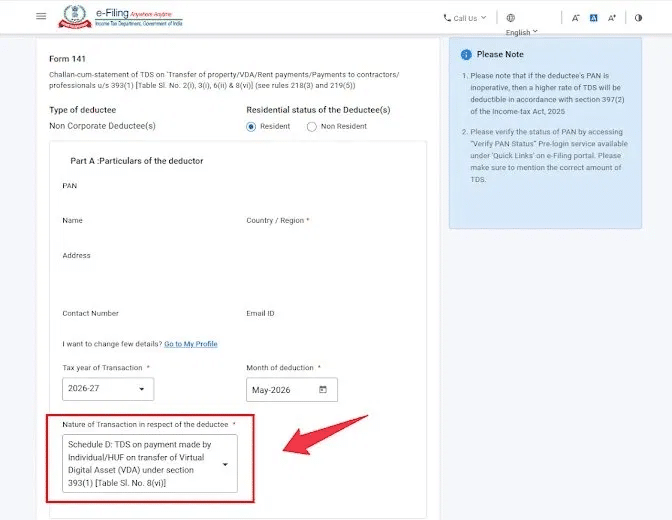

- Click “Continue,” and you will be taken to Part A: Particulars of the Deductor screen. Enter your details:

- PAN (auto-populated from login)

- Name

- Country/Region

- Address

- Contact Number

- Email ID

- Tax Year of Transaction (select 2026-2027)

- Month of Deduction (select the relevant month, e.g., May-2026)

- Click “Continue” to reach the Transaction Details page for Schedule D. Here, enter the following for each transaction:

- Seller’s (Deductee’s) PAN

- Seller’s Name and Address

- Residential Status of the Deductee (Resident or Non-Resident)

- Type of VDA transferred (crypto-asset, NFT, or other VDA)

- Amount of consideration paid or credited

- Date of payment or credit (whichever is earlier)

- TDS amount (1% of consideration, or 20% if seller PAN is not available)10.

10. Click “Save.” The transaction data will be stored in a table format on screen. You can edit or delete any entry by selecting the checkbox next to it. If you have multiple transactions with different sellers (of the same deductee type) for the same month, you can add more entries here before proceeding.

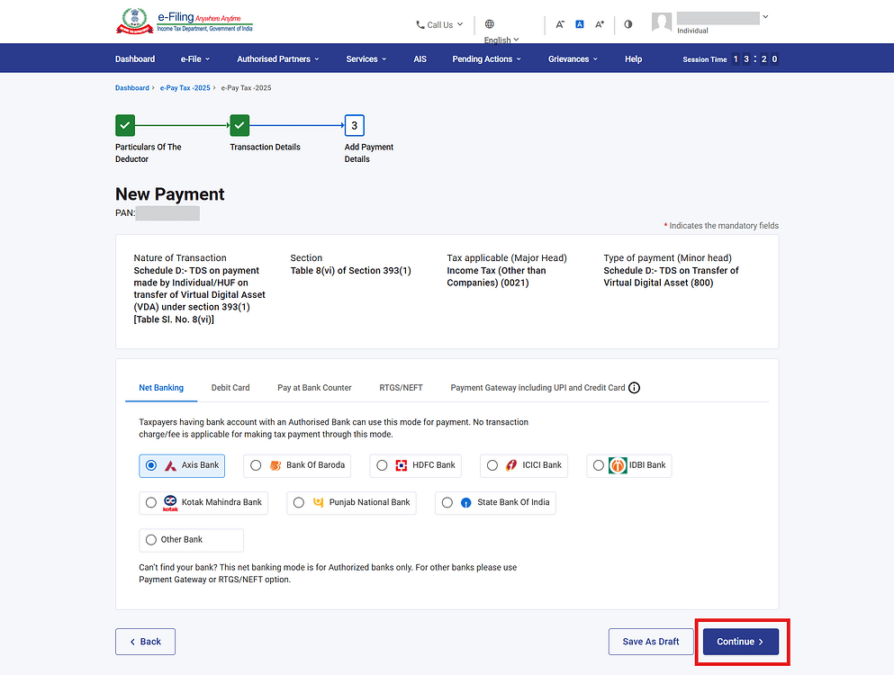

11. Click “Continue” to proceed to the payment screen. Pay the TDS amount through the integrated payment gateway using net banking, debit card, or any available payment mode.

12. After payment, you will be taken to the e-Verification page. Verify the form using either a Digital Signature Certificate (DSC) or an Electronic Verification Code (EVC), whichever applies to you.

13. On successful submission, you will receive an Acknowledgement Receipt Number (ARN). Download and save this receipt immediately. SMS and email confirmations will also be sent to your registered mobile number and email ID.

To view your filed Form 141 later, follow this path on the portal: PAN Login > e-File > e-Pay Tax > Select Income Tax Act, 2025 > Payment History > Action.

If you make any errors in the filed Form 141, corrections can be submitted through the TRACES portal. You must register as a “Taxpayer” on TRACES to access this feature. As per the Form 141 FAQs (PDF) published by the Income Tax Department, a correction statement can be filed within two years from the end of the tax year in which the original statement was due.

Step 5: Issue Form 132 to the seller

Under the old Act, the buyer issued Form 16E after filing Form 26QE. From April 1, 2026, the corresponding certificate is Form 132, issued under Section 395(4) of the Income-tax Act, 2025.

Form 132 is a consolidated TDS certificate that has been created by merging four earlier forms: Form 16B (property), Form 16C (rent), Form 16D (contractor), and Form 16E (VDA). As confirmed in the Form 141 FAQs (PDF), the deductor can download the relevant TDS certificate in Form 132 from TRACES after successful processing.

The process to download Form 132 from TRACES:

- Register on the TRACES portal (tdscpc.gov.in) as a “Taxpayer” if you have not already done so

- Log in to your TRACES account

- Go to the Downloads section

- Select the appropriate form type and enter the details: Tax Year, Acknowledgement Number from the Form 141 filing, and PAN of the Seller

- A request will be generated

- Once the status shows “Available,” download Form 132 and issue it to the seller

The deadline for issuing Form 132 is within 15 days of the due date of filing Form 141. For example, if your Form 141 was due by June 30, 2026 (for a May 2026 transaction), Form 132 must be issued to the seller by July 15, 2026.

Step 6: Filing for Non-Specified persons (Form 26Q route)

If you are not a specified person (a company, a firm, or an individual with business turnover above Rs 1 crore), the process is different:

- You must first obtain a TAN (Tax Deduction and Collection Account Number) if you don’t already have one

- Deposit TDS by the 7th of the following month (for example, TDS deducted in May must be deposited by June 7)

- File quarterly TDS returns in Form 26Q

- Issue Form 16A as the TDS certificate to the seller

The quarterly due dates for Form 26Q are:

- Q1 (April to June): July 31

- Q2 (July to September): October 31

- Q3 (October to December): January 31

- Q4 (January to March): May 31

Quick reference: Old forms vs new forms for P2P crypto TDS

Understanding which form applies to which period is essential to avoid filing mistakes. Here is the complete mapping as documented in the official Form 141 guidance note (PDF):

Challan-cum-statement for VDA TDS (specified persons):

- Up to March 31, 2026: Form 26QE under Section 194S, Income-tax Act, 1961

- From April 1, 2026: Form 141 Schedule D under Section 393(1) [Table Sl. No. 8(vi)], Income-tax Act, 2025

TDS certificate issued to seller:

- Up to March 31, 2026: Form 16E under the old Act

- From April 1, 2026: Form 132 under Section 395(4), Income-tax Act, 2025

TDS credit statement for seller:

- Up to March 31, 2026: Form 26AS / AIS

- From Tax Year 2026-27: Form 168 (AIS) under Section 510, Income-tax Act, 2025

Governing rules:

- Up to March 31, 2026: Rules 30 and 31A, Income-tax Rules, 1962

- From April 1, 2026: Rules 218 and 219, Income-tax Rules, 2026

Important: If your P2P crypto transaction happened before April 1, 2026, but you are filing the TDS statement after that date, you still use the old Form 26QE. The form is determined by when the payment or credit occurred, not when you are filing.

Conversely, if the payment or credit happened on or after April 1, 2026, you must use Form 141 Schedule D even if the filing date falls in the same transition period.

What the seller needs to do

The seller in a P2P crypto transaction does not have the primary TDS deduction responsibility, but that does not mean they can sit back and ignore the compliance side entirely.

Verify TDS credit in Form 168 (AIS) [previously Form 26AS]

After the buyer deducts and deposits TDS, the amount should reflect in the seller’sForm 168 (Annual Information Statement) and the Taxpayer Information Summary (TIS).

For FY 2025-26 transactions (ITR due July 2026), the credit still appears under the old Form 26AS on the portal. For Tax Year 2026-27 onward, the credit will appear under the new Form 168 framework.

The seller should:

- Log in to the Income Tax e-Filing Portal (incometax.gov.in)

- Navigate to “e-File” and select “View Form 26AS” or “Annual Information Statement” for the new format

- Check if the TDS deducted by the buyer appears under Part F (which covers TDS on sale of immovable property, rent, and now Virtual Digital Assets under Section 194S)

- Also, check the AIS (Annual Information Statement) for the transaction details

If the TDS does not reflect, follow up with the buyer to ensure they have filed Form 141 (or Form 26QE for pre-April 2026 transactions) and that the details (PAN, amount) are correct.

Under the new Form 168 framework, sellers also have the ability to submit feedback on individual transactions if they spot incorrect or duplicate entries. This can be done through the AIS portal on incometax.gov.in by selecting a specific transaction and clicking “Give Feedback.” The Taxpayer Information Summary (TIS) will update automatically once the department processes the feedback.

Report in Schedule VDA while filing ITR

When the seller files their Income Tax Return for the relevant financial year, they must:

- Use ITR-2 (if income is from capital gains) or ITR-3 (if crypto trading is treated as business income). ITR-1 and ITR-4 cannot be used to report crypto income.

- Fill out Schedule VDA, which requires transaction-by-transaction details including:

- Date of acquisition of the crypto asset

- Date of transfer (sale)

- Cost of acquisition (the only allowable deduction)

- Sale consideration

- Resulting income or loss

- Pay the flat 30% tax on crypto gains under Section 115BBH (plus 4% health and education cess and applicable surcharge, making the effective minimum rate 31.2%)

- Claim the TDS credit against the total tax liability

What if the buyer does not deduct TDS?

This puts the seller in a tricky spot. The CBDT has clarified that when both parties fail to deduct TDS in a P2P transaction, the primary responsibility falls on the buyer. However, the seller is not entirely off the hook.

The Income Tax Department may still raise questions during assessment if TDS was not deducted on a transaction that clearly should have attracted it. The seller should maintain complete records of all P2P transactions, including screenshots of conversations, wallet addresses, bank transfer receipts, and the seller’s PAN, as evidence that they made a good-faith effort at compliance.

Deadlines and due dates you cannot miss

For Specified Persons (Form 141 Schedule D) [previously Form 26QE]

The TDS must be deposited within 30 days from the end of the month in which the deduction was made.

Examples:

- If you deducted TDS on a transaction on May 15, 2026, the deadline for depositing TDS and filing Form 141 is June 30, 2026.

- If the deduction was on March 10, 2026, the deadline is April 30, 2026 (as specifically confirmed by the Income Tax Department for non-government deductors for FY 2025-26).

As The Crypto Times highlighted in their TDS deadline coverage, for April 2026 crypto transactions onward, direct buyers may need to pay and report TDS by May 30, while exchanges and businesses follow their own filing routes.

For Non-Specified persons (Form 26Q)

- TDS must be deposited by the 7th of the month following the deduction

- Quarterly returns in Form 26Q must be filed by the due dates mentioned above

Form 132 Certificate [previously Form 16E]

Must be issued to the seller within 15 days from the due date of filing Form 141.

What Changed from April 1, 2026: The Income Tax Act, 2025

The Income Tax Act, 2025 became effective from April 1, 2026, replacing the Income-tax Act, 1961. For crypto traders, there are several key changes to be aware of:

New section numbers

The entire 194-series of TDS provisions has been retired. Section 194S now falls under the broader Section 393 of the new Act, which consolidates all non-salary TDS provisions. However, the rates and thresholds remain the same. The 1% TDS on VDA transfers continues as before.

Form 26QE is now Form 141 Schedule D [with Form 132 replacing Form 16E]

For transactions from April 1, 2026 onward, the challan-cum-statement previously known as Form 26QE is being transitioned to Form 141, Schedule D. The process remains similar, but the form number and certain field names are updated.

Similarly, the TDS certificate that the buyer issues to the seller is now Form 132 instead of Form 16E. Both Form 132 and Form 141 are governed by the new Income-tax Rules, 2026 (Rules 218, 219, and 215, respectively).

Expanded VDA definition

The Finance Act 2025 explicitly included “crypto-asset” as a sub-category within the VDA definition, effective April 1, 2026. This eliminates any interpretational gap that may have existed about whether specific tokens or digital assets were covered.

New penalty framework

This is significant. Under Section 446 of the Income Tax Act, 2025 and Section 509(1), new penalties for crypto reporting failures have been introduced:

- Rs 200 per day for non-furnishing of crypto transaction statements by reporting entities

- Rs 50,000 flat penalty for inaccurate information in these statements

As The Crypto Times reported in March 2026, Budget 2026 kept the 30% tax and 1% TDS completely unchanged while adding enforcement muscle through these new penalty provisions.

CBDT circulars are now legally binding

Under Section 400(2) of the new Act, CBDT circulars on TDS, including those related to virtual digital assets, now carry mandatory compliance weight. The argument that these circulars are merely advisory no longer holds legal ground.

Late fee under the new Act

Under Section 427 of the Income-tax Act, 2025, a late fee will be levied for delay in filing Form 141. This replaces the old Section 234E late fee provision for the new form regime. The structure remains similar (Rs 200 per day), but the legal reference has changed. This is confirmed in the Form 141 FAQs (PDF) published by the department.

Error correction window

If you discover an error in a filed Form 141, a correction statement can be filed through the TRACES portal within two years from the end of the tax year in which the original statement was required to be delivered. After the correction is processed, a revised Form 132 can be generated and issued to the seller.

Penalties for non-compliance

Not deducting or not depositing TDS on crypto transactions carries serious consequences. Here is the complete penalty structure:

Interest on Late Deduction

If you fail to deduct TDS or deduct it late, interest is charged under Section 201(1A) [Section 398(3)(a) under the new Act]:

- 1% per month (or part of a month) from the date on which TDS was deductible to the date on which it is actually deducted

- 1.5% per month from the date of deduction to the date of actual deposit with the government

Late Filing Fee

Under Section 234E [Section 427 under the new Act], a late filing fee of Rs 200 per day is charged for the delayed filing of TDS returns. This continues until the total fee equals the TDS amount itself.

Penalty for Non-Deduction

Under Section 271C, a penalty equal to the amount of TDS not deducted can be imposed. So if you should have deducted Rs 10,000 in TDS and failed to do so, you could face a penalty of Rs 10,000 on top of the interest.

Prosecution

In severe cases where TDS is deducted but not deposited with the government, prosecution can be initiated under Section 276B. This can lead to imprisonment.

Under the new Act, maximum imprisonment for TDS defaults has been reduced from seven years to two years, with courts now allowed to convert violations into monetary penalties.

Disallowance of expenses

If you fail to deduct TDS, the related expense may be disallowed as a deduction in your own income tax assessment.

Invalid or incorrect seller PAN

If the seller’s PAN entered in Form 141 is invalid or incorrect, the TDS credit will not be reflected in the seller’s Form 168 (AIS). In such cases, the deductor will also be liable to deduct tax at the higher rate (20% instead of 1%) as per Section 397(2) of the Income-tax Act, 2025. Correcting the PAN later requires filing a correction statement through TRACES.

Practical scenarios and examples

Scenario 1: Simple INR-to-Crypto P2P Buy

Rahul (a salaried individual) buys 0.5 BTC from Priya for Rs 3,00,000 through a P2P deal.

- Rahul is a specified person (salaried, no business income)

- Threshold for specified persons: Rs 50,000

- Rs 3,00,000 exceeds the threshold

- Rahul deducts 1% TDS: Rs 3,000

- Rahul pays Priya Rs 2,97,000

- Rahul files Form 141 Schedule D (or Form 26QE if the transaction was before April 1, 2026) within 30 days from the end of the month

- Rahul downloads Form 132 from TRACES portal after processing and issues Form 16E to Priya within 15 days of the Form 141 due date

- Priya checks her Form 168 (AIS) to verify the Rs 3,000 TDS credit

- Priya claims this credit when filing her ITR

Scenario 2: Crypto-to-crypto swap between two individuals

Amit gives 10 ETH (valued at Rs 5,00,000) to Vikram and receives 5,00,000 USDT (valued at Rs 5,00,000) from Vikram.

- Both Amit and Vikram are simultaneously buyers and sellers

- Amit must deduct 1% of the value of USDT received: Rs 5,000, and deposit it

- Vikram must deduct 1% of the value of ETH received: Rs 5,000, and deposit it

- Both file Form 141 Schedule D independently

- Both download Form 132 from TRACES and issue it to each other

- Since the payment is entirely in kind, both must deposit TDS in cash before releasing the crypto

Scenario 3: Multiple small transactions that cross the threshold

Neha (a freelancer with professional receipts under Rs 50 lakh) buys USDT from the same seller across four months:

- April: Rs 15,000

- June: Rs 20,000

- August: Rs 10,000

- October: Rs 10,000

After the October transaction, the aggregate crosses Rs 50,000 (total: Rs 55,000). TDS becomes applicable to the October transaction and all subsequent purchases from the same seller. Neha must deduct 1% TDS from the October payment onward.

Scenario 4: Filing the wrong form during the transition period

Kavita bought crypto on March 25, 2026, but did not file the TDS return until April 10, 2026. Even though the filing date falls after April 1, 2026, the transaction date (payment or credit) was in March 2026. Therefore, Kavita must use the old Form 26QE, not Form 141.

The form is determined by when the payment or credit occurred, not when you get around to filing. If Kavita makes another P2P purchase on April 5, 2026, that transaction must go through Form 141 Schedule D.

Documents and records you should maintain

Whether you are the buyer or the seller, keep these records for every P2P crypto transaction:

- PAN of the counterparty

- Date and time of the transaction

- Type and quantity of VDA transferred

- INR value of the transaction (or fair market value if it is a crypto-to-crypto swap)

- Proof of payment (bank statement, UPI screenshot, wallet transfer confirmation)

- Form 141 acknowledgement receipt (ARN) for buyer, or Form 132 certificate for seller

- TDS challan payment receipt

- Communication records with the counterparty (WhatsApp messages, Telegram chats, email exchanges)

- Wallet addresses involved in the transaction

Maintaining thorough records becomes especially important because The Crypto Times reported that over 44,000 tax notices have already been issued to crypto traders in India, with the department using tools like Project Insight and internal data analytics to match TDS records with ITR data.

TDS does not apply to buying crypto with INR from an exchange

A common misconception worth clearing up: when you buy crypto using INR, you are acquiring a VDA, not transferring one. Section 194S applies on the “transfer” of a Virtual Digital Asset, which means it kicks in when someone is selling or giving up the crypto, not when someone is buying it for the first time with fiat.

On an exchange, the TDS is handled on the seller’s side by the platform itself. In a P2P deal, TDS is deducted from the payment the buyer makes to the seller, which effectively means the seller bears it as a reduction from their sale proceeds.

How exchanges handle TDS separately under the new Act

While this guide focuses on P2P, it is worth noting that crypto exchanges have their own separate compliance route under the new Act. Exchanges file Form 142, which is a separate quarterly exchange statement for VDA transactions conducted on or through their platform.

This is distinct from the individual buyer’s Form 141 Schedule D obligation in P2P. The two should not be confused. If you trade on an exchange, the exchange handles TDS via Form 142. If you trade P2P, you handle TDS via Form 141 Schedule D.

TDS on international and offshore exchange P2P transactions

Section 194S applies only when the seller is a resident of India. If you are buying crypto from a non-resident through an overseas P2P platform, the standard Section 194S TDS may not apply, but other tax provisions (like TCS under the Liberalised Remittance Scheme, if you are remitting money abroad) could come into play.

However, the government has been cracking down aggressively on offshore platforms. As The Crypto Times covered in January 2026, the Income Tax Department has flagged crypto risks specifically and noted that offshore exchanges pose enforcement challenges because they do not deduct TDS and may not respond to tax notices.

From April 2027, Indian tax authorities will begin automatically receiving crypto transaction data from other participating countries under the Crypto-Asset Reporting Framework (CARF), closing this gap further.

The bigger picture

India’s crypto tax regime remains one of the most discussed topics in the industry. With a flat 30% tax on gains, 1% TDS on every qualifying transaction, no set-off of losses between different crypto assets, and no carry-forward of losses, the framework is significantly more restrictive than what most other major crypto markets impose.

As The Crypto Times has consistently reported, the taxation infrastructure is expanding, but a comprehensive regulatory framework for crypto remains absent. The country taxes crypto aggressively and tracks it through TDS, but there is still no dedicated law defining what crypto assets are, what rights holders have, or how markets should operate.

For now, if you are participating in P2P crypto transactions, compliance is not just advisable; it is essential. The TDS mechanism ensures that every transaction creates a trail, and with 44,000+ tax notices already issued and AI-driven analytics being deployed by the department, the days of flying under the radar are effectively over.

File your Form 141 Schedule D. Issue Form 132. Maintain your records. And when the ITR season comes, make sure Schedule VDA is filled out completely. That is the simplest way to stay on the right side of the law while continuing to participate in the crypto market.

Frequently asked questions

Do I need a TAN to deduct TDS under Section 194S?

No. If you are a specified person (individual/HUF with no or limited business income), TAN is not required. You file using Form 141 Schedule D (previously Form 26QE) with just your PAN. Only non-specified persons (companies, firms, large businesses) need a TAN and must file through Form 26Q.

Is TDS applicable on crypto received as a gift?

Section 194S covers transfers where “consideration” is paid. Gifts where no consideration is exchanged may not attract TDS under 194S, but the recipient may still be liable to pay tax on the gift under Section 56(2)(x) if its value exceeds Rs 50,000.

Can I claim a TDS refund?

Yes. When you file your ITR, the TDS already deducted is credited to you. If your total tax liability is less than the total TDS deducted during the year, you can claim a refund for the excess amount.

Does TDS apply even if I am selling at a loss?

Yes. TDS under Section 194S is on the total consideration (the sale value), not on the profit. It applies regardless of whether the seller is booking a profit or a loss on the transaction. Remember, TDS is a tracking mechanism, not a final tax.

What about GST on crypto?

An 18% GST applies to service charges levied by crypto exchanges and platforms, but it does not apply to the crypto amount itself. When calculating TDS, the CBDT has clarified that TDS is to be calculated on the net amount excluding GST.

Does Section 194S apply to staking rewards or airdrops?

Staking rewards and airdrops, where you receive crypto without making a direct payment to anyone, generally do not attract TDS under Section 194S since there is no identifiable “payer” making a transfer in exchange for consideration. However, these rewards are still taxable as income at the flat 30% rate under Section 115BBH.

What happens if I trade on a foreign-exchange P2P platform?

If you are an Indian resident buying crypto from another Indian resident on a foreign exchange’s P2P section, the TDS obligation under Section 194S still technically applies because the transaction is between two Indian residents. The challenge is enforcement and compliance. Regardless, you are expected to self-comply.

I filed Form 26QE for a transaction before April 2026. Do I need to refile under Form 141?

No. If the payment or credit happened before April 1, 2026, the old Form 26QE filing is valid, and no refiling under Form 141 is required. Form 141 applies only to transactions where the payment or credit occurs on or after April 1, 2026.

What if I cannot see Form 141 on the e-filing portal?

Make sure you have selected “Income-tax Act, 2025” on the Act Selection screen after clicking e-Pay Tax. Form 141 is available exclusively under the new Act. If you are on the old Act tab, it will not appear. Starting in Tax Year 2026-27, all PAN-based payment forms are consolidated into a single tile under the new Act section.

Can I include multiple P2P transactions in one Form 141?

Yes, but with conditions. You can include multiple deductees in a single Form 141 filing, provided all deductees belong to the same type (all corporate or all non-corporate) and the transactions share the same month of deduction.

If you bought crypto from different individuals across the same month, you can report all of them in one Form 141 Schedule D filing. If one seller was a company and another was an individual, you would need two separate filings. If the month of deduction differs, separate Form 141s are required even for the same deductee type.

Also Read: Your Crypto, NFTs, and Online Wealth May Die With You in India