While Bitcoin clawed back roughly 6.5% from its recent lows near $57,832, the shares of Strategy Inc., the largest Bitcoin treasury company, has risen strikingly more than 23% from a 52-week low of $81.81 hit on June 26.

The company formerly known as MicroStrategy and operating under the ticker MSTR for its common shares, saw enormous investor interest after announcing a comprehensive Digital Credit Capital Framework on June 29, 2026 to shuffle a way out from the financial scrutiny.

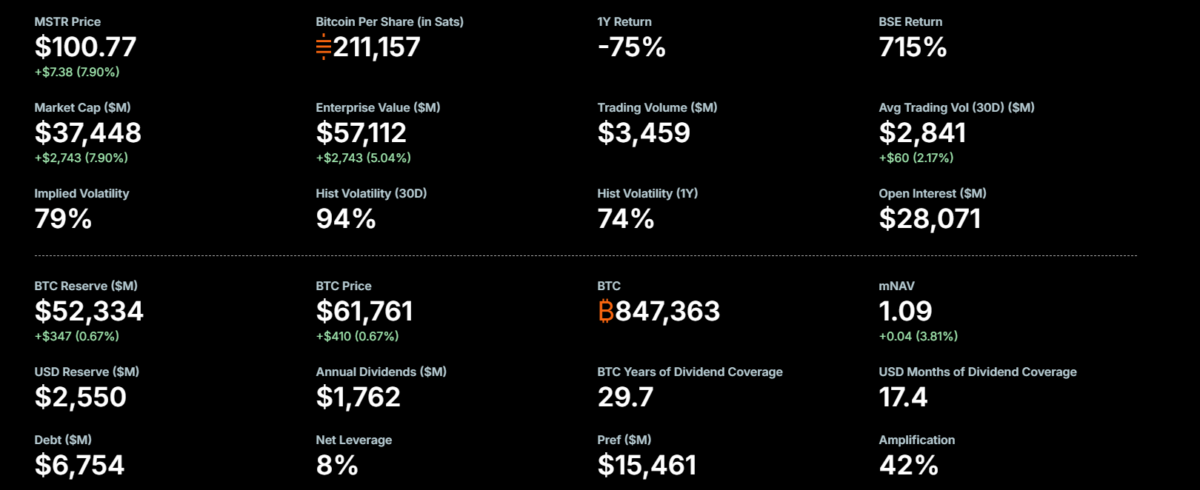

The divergence has reignited debate over whether Michael Saylor’s long-running strategy of turning the company into a leveraged Bitcoin vehicle is finally delivering outsized results—or simply amplifying short-term market swings. Strategy now holds 847,363 Bitcoin, worth around $52 billion at prevailing BTC price of $61,600—acquired at an average cost of roughly $75,651 per coin.

MSTR as a High-Leverage Bitcoin Proxy

Strategy functions less like a traditional software company and more like a magnified bet on Bitcoin. Its core treasury strategy involves accumulating Bitcoin aggressively, funded through a mix of common equity issuance (MSTR), convertible debt, and a suite of preferred securities such as the variable-rate Series A Perpetual Stretch Preferred Stock (STRC).

This capital structure of the company creates leverage. When Bitcoin rises, the value of the company’s holdings increases, and the market often prices in expectations of further accumulation or improved financing terms. The reverse happens on the way down, but with greater intensity because of dilution from equity raises and the sensitivity of preferred instruments to perceived credit risk.

Analysts have long described MSTR as offering “high-beta” exposure to Bitcoin—meaning its percentage moves tend to exceed those of the cryptocurrency itself. In practice, this has translated into amplified gains during rallies and sharper drawdowns during corrections. The company’s Bitcoin-per-share metric, currently around 211,157 satoshis, underscores how directly shareholders are exposed to BTC price action through the balance sheet.

Recent price action illustrates the point. While Bitcoin gained about 6.5% from its early-July low, MSTR advanced more than three times that amount. Such outperformance is consistent with periods when market sentiment toward Bitcoin turns positive and investors rotate into leveraged vehicles that can deliver enhanced returns.

Historical Correlation Between Bitcoin and MSTR

The link between Bitcoin and Strategy stock has strengthened dramatically since the company began its Bitcoin treasury strategy in 2020. Prior to that shift, MSTR behaved like a conventional enterprise software firm with limited or even negative correlation to cryptocurrency prices.

Post-2020 data shows correlation coefficients typically ranging from 0.6 to 0.9 on rolling windows, with recent one-year figures hovering around 0.65.

This is not perfect lockstep—other factors such as dilution, changes in financing costs, and the company’s software business still play roles—but Bitcoin has become the dominant driver.

During Bitcoin’s major upswings, MSTR has frequently delivered 1.5x to 2x or greater percentage gains. In downturns, the stock has often fallen further. This leveraged beta arises mechanically: the company’s enterprise value is heavily influenced by the mark-to-market value of its Bitcoin holdings, while its equity and preferred securities trade with sensitivity to both BTC price and the company’s ability to continue raising capital at attractive terms.

Volatility metrics reinforce the picture. Strategy stock has exhibited significantly higher historical volatility than Bitcoin itself in many periods, reflecting the added layers of financial engineering.

Over the past several months, the performance gap between Bitcoin and Strategy Inc. shares has been stark. From early February through early July 2026, Bitcoin has declined approximately 32.4%, while MSTR has fallen even further at 41.75%, highlighting the stock’s heightened sensitivity during the broader crypto downturn.

The chart above illustrates periods of close tracking punctuated by amplified drawdowns in MSTR, particularly in late June, followed by a sharper rebound in early July that has narrowed the relative underperformance as the stock recovered more vigorously from its lows. This visual underscores the leveraged beta nature of MSTR as a Bitcoin proxy—magnifying both downside risk and potential upside in volatile markets.

A Period of Sharp Declines and Heightened Scrutiny

The current rebound comes after a bruising stretch for both MSTR and its preferred instruments. In 2026, as Bitcoin pulled back from its October 2025 peak of $126,198 toward the low $60,000s and briefly tested below $58,000, Strategy shares fell sharply. The stock reached two-year lows and posted year-to-date declines exceeding 38% at points.

Particular pressure fell on the STRC preferred stock, designed as a key capital-raising tool with a target around $100 par value. In May and June, STRC traded below par, slipping toward $95 and lower at times, triggering contractual increases in its dividend rate. The rate moved to 12%, raising annual dividend obligations and drawing scrutiny over cash coverage and the sustainability of the financing model.

The reason for this decline was pointed to shrinking cash reserves relative to dividend and interest commitments, the impact of share dilution from ongoing equity raises, and mammoth unrealized losses on the Bitcoin treasury that contributed to large reported net losses (including a $12.54 billion net loss in Q1 2026 driven largely by digital asset mark-downs).

Some observers warned of potential feedback loops if a falling stock price impaired the ability to raise new capital or if preferred securities continued de-anchoring from par.

Strategy also executed its first sale of 32 BTC in years amid the pressure, a move that contrasted with the long-standing “never sell” rhetoric associated with Saylor. Legal and investor scrutiny intensified around the capital structure and governance.

The June 29 Framework and Recent Price Reaction

On June 29, Strategy announced its Digital Credit Capital Framework, a structured response to the accumulated stresses. The plan includes building a $2.55 billion USD reserve, raising the STRC dividend rate to 12% while authorizing up to $1 billion in repurchases of Digital Credit Securities (including STRC), and up to $1 billion in common stock buybacks. It also introduces a BTC Monetization Program allowing selective sales of up to $1.25 billion in Bitcoin for liquidity needs.

The announcement aimed to strengthen the preferred securities stack, provide greater balance-sheet flexibility, and preserve long-term Bitcoin exposure without forcing wholesale liquidation. Shares of MSTR jumped sharply in response—rising more than 12% intraday at one point—and have continued to recover.

While the framework does not commit the company to immediate large-scale buybacks or sales, it gives management tools to act opportunistically.

Assessing Whether Saylor’s Approach Is Working

Michael Saylor has positioned Strategy as a Bitcoin development company whose primary mission is to acquire and hold the asset for the long term, using innovative capital markets techniques to scale the treasury. The recent outperformance of MSTR relative to spot Bitcoin suggests that, at least in the short term, the leveraged structure is delivering the intended amplification when sentiment improves.

The company’s Bitcoin holdings now represent a substantial portion of total supply—roughly 4%—and its accumulation has been relentless through multiple market cycles. Software operations continue to generate revenue, providing some underlying business support, though they are secondary to the treasury narrative.

Still, the strategy carries clear risks. Leverage magnifies losses as well as gains. Reliance on continuous capital raises can become problematic in prolonged downturns. The preferred securities layer adds complexity and sensitivity to credit perceptions. The move toward selective monetization introduces optionality but also invites questions about long-term discipline.

Whether the June framework marks a durable turning point or merely a tactical adjustment remains to be seen. Bitcoin’s broader trajectory, interest-rate policy, and investor appetite for leveraged crypto exposure will all play roles.

As of now, the numbers show Strategy stock recovering more vigorously than the underlying cryptocurrency from recent lows. That gap keeps Saylor’s high-conviction Bitcoin bet squarely in the spotlight—both as a potential model for corporate treasury strategy and as a high-risk, high-reward vehicle for those seeking amplified exposure to digital assets.

Also read: Inside the Trump Family’s $1.2B Crypto Windfall: Who Paid the Price?