In a move that underscores its evolution into a full-fledged Bitcoin treasury powerhouse, Strategy Inc. (formerly MicroStrategy) announced on May 26, 2026, that it has retired $1.5 billion of its 2029 convertible notes at a discount, trimming its overall debt load and delivering an immediate lift to its signature BTC yield metric.

The company, led by Bitcoin evangelist Michael Saylor, paid roughly $1.38 billion in cash for the notes—an 8% discount to par value. The transaction cuts Strategy’s aggregate convertible debt from $8.2 billion to $6.7 billion and contributes 0.7% points to its year-to-date BTC yield, according to the official release.

Debt Management in a Bitcoin-First World

The repurchase represents a deliberate piece of liability management. Strategy had previously signaled it would use a range of tools—cash, equity issuances, and even selective Bitcoin sales—to optimize its capital structure.

By buying back the zero-coupon 2029 notes below face value, the company not only reduces future dilution risk from potential conversions but also frees up balance-sheet flexibility.

“These transactions demonstrate the optionality we have built into Strategy’s capital structure and our dynamic, multi-variate capital allocation model,” Saylor said in the company’s release. “Strategy has the flexibility to fund strategic transactions using cash, Digital Equity, Digital Credit, or Digital Capital, giving us multiple levers to optimize our balance sheet and respond to market conditions.”

Saylor added that the company remains “focused on increasing Bitcoin Per Share” for its shareholders while “maintaining a fortress balance sheet for our Digital Credit investors.”

The deal was funded partly through cash reserves and proceeds from sales of its variable-rate perpetual preferred stock (STRC) and common shares under at-the-market programs.

During the same period, Strategy issued about $2 billion notional of additional STRC and used proceeds, along with other capital, to acquire another 24,869 Bitcoin.

The BTC Yield Metric Takes Center Stage

Strategy’s emphasis on “BTC yield” has become a key performance indicator for investors treating the stock as a leveraged proxy for Bitcoin exposure. This metric is essentially the growth in Bitcoin holdings per share.

The latest debt move added 0.7% to that yield, while the broader year-to-date performance reflects aggressive accumulation even as Bitcoin’s price has fluctuated.

Critics like Peter Schiff have long questioned the sustainability of loading up on debt and issuing new shares to buy more Bitcoin. Yet supporters point to the math: by retiring debt at a discount and continuing to stack sats, Strategy is engineering higher Bitcoin ownership concentration for equity holders without proportionally increasing liabilities.

The company also maintains a designated USD reserve, which currently sits at $871 million, intended to support preferred stock dividends and debt interest. Executives said they plan to replenish it over time through market-based issuances.

From Software Firm to Bitcoin Treasury Leader

Strategy’s transformation traces back to 2020, when it began converting its treasury into Bitcoin under Saylor’s direction. What started as a hedge against inflation has morphed into the company’s core identity.

In early 2025, MicroStrategy officially rebranded to Strategy, adopting a Bitcoin-inspired orange logo and positioning itself explicitly as “the world’s first and largest Bitcoin Treasury Company.”

The software business that once defined the firm—enterprise analytics tools—now plays second fiddle to its digital asset strategy. Strategy has issued multiple tranches of convertible notes and innovative preferred securities like STRC to fund Bitcoin purchases, turning corporate finance into what some call a “Bitcoin leverage masterclass.”

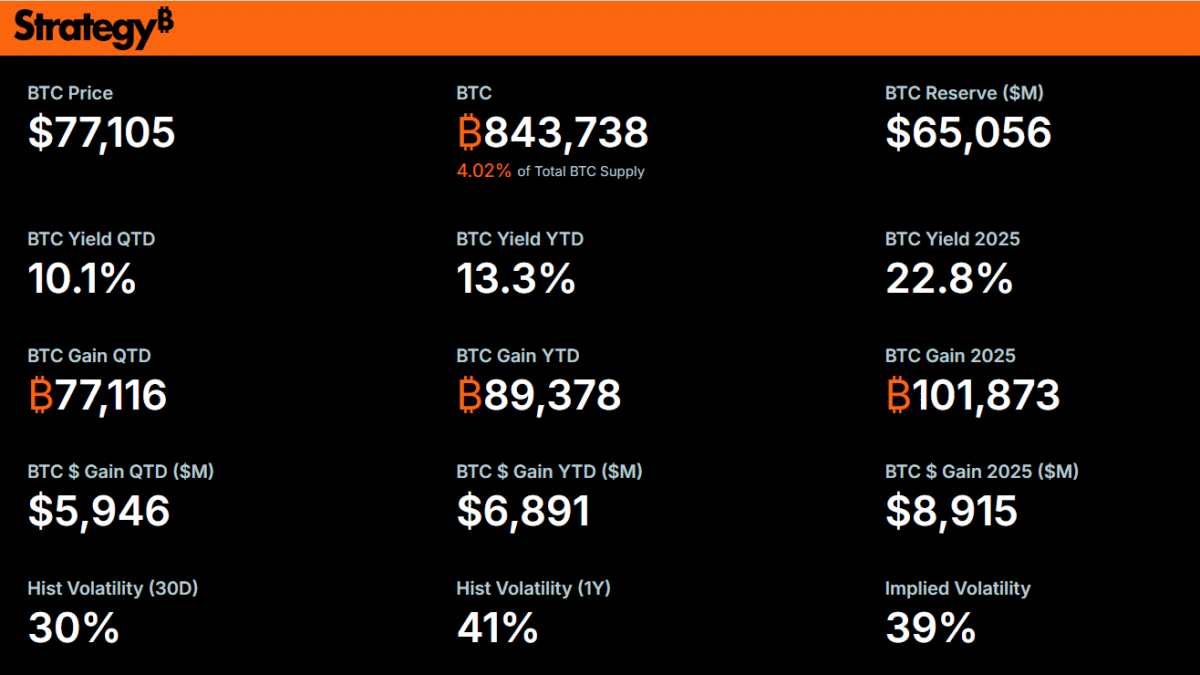

As of May 26, Strategy holds 843,738 Bitcoin, purchased at a total cost of about $63.87 billion with an average price of roughly $75,700 per coin. Year-to-date in 2026, the firm has posted a 13.3% BTC yield alongside a BTC gain of 89,378 coins, valued at approximately $6.8 billion.

This hoard represents a significant portion of all circulating Bitcoin, giving the company outsized influence in the ecosystem while exposing it to the asset’s notorious volatility.

Market Reaction and Broader Implications

Wall Street has largely cheered Strategy’s approach. Its stock (still trading under MSTR alongside other tickers) has delivered outsized returns for investors comfortable with the embedded leverage.

However, the common share MSTR closed nearly 5% on the last trading session (May 22, 2026) after Saylor’s Sunday announcement on the halt of Strategy’s weekly Bitcoin purchase and buying of bonds.

Retiring convertible debt at a discount is credit-positive and equity-positive, with it reducing overhang from potential share issuance upon conversion. At the same time, many analysts state that continued reliance on preferred stock raises questions about the long-term cost of capital and dilution dynamics.

Saylor, never one to shy from bold statements, has consistently framed Strategy’s playbook as a superior way for institutions and individuals to gain Bitcoin exposure. Whether through common equity, preferred instruments, or direct holdings, the company aims to offer tailored risk-reward profiles tied to Bitcoin’s performance.

As Bitcoin enters what Saylor has called a potential “summer” of strength, the company’s latest maneuvers position it to capitalize. With $6.7 billion in remaining convertible debt and a massive Bitcoin reserve, Strategy isn’t just holding the asset, it’s reshaping how public companies interact with it.

The latest announcement arrives as Bitcoin trades in a range many consider consolidative ahead of potential catalysts. At the time of publishing, BTC was trading near $76,900—down decently 0.5% from in the past 24 hours.

Also read: Virtus InfraCap Boosts Exposure to Strategy’s Bitcoin Treasury Play