Key Highlights

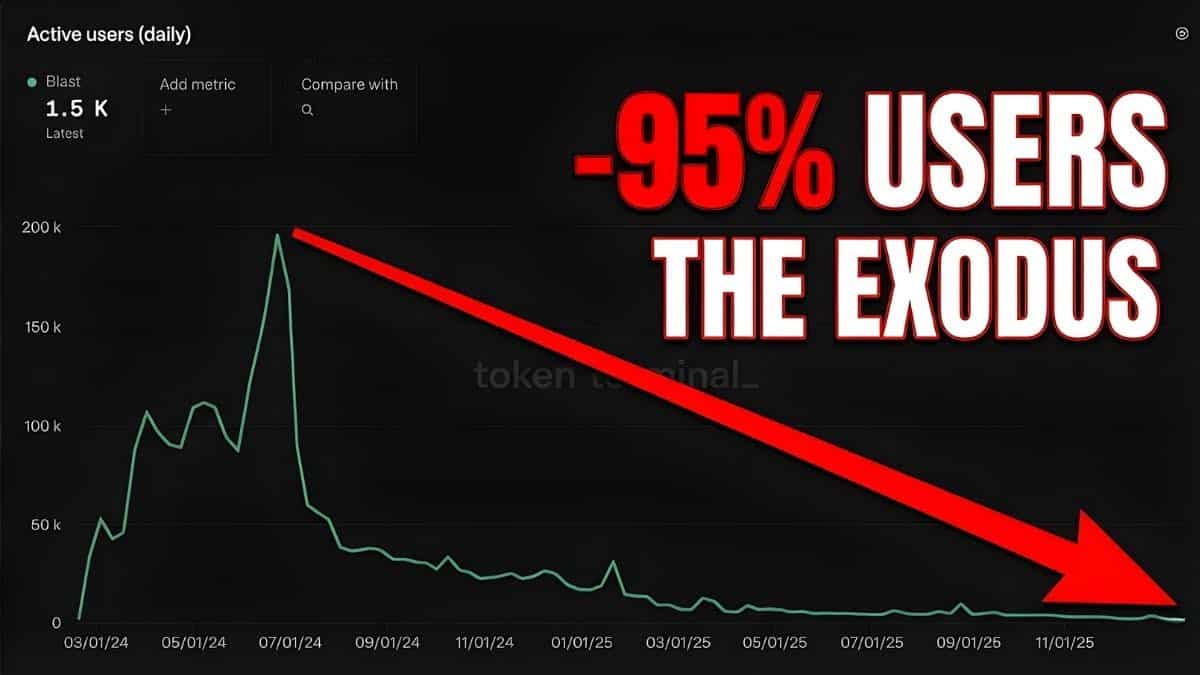

- The Crash: Blast Network’s daily active users have plummeted from over 160,000 to under 4,000—a 95% drop from its peak.

- The Flaw: The model relied on “Points” rather than utility. Once the incentives (airdrop) were distributed, mercenary capital fled immediately.

- The Valuation: At its peak, the BLAST token implied a $2.8 billion valuation. Today, it trades near $0.0008, effectively rendering the protocol irrelevant.

The cryptocurrency industry has a tendency to remember its failures selectively. When collapse is sudden and violent, as in the case of Terra-Luna or FTX, the post-mortems are exhaustive and relentless. But the majority of crypto projects do not end in catastrophe. Capital leaves quietly, users drift elsewhere, and the protocol remains technically operational while becoming economically and culturally irrelevant.

The industry rarely documents these quieter deaths, even though they are far more common. And Blast Network is a near-perfect example of this phenomenon.

The idea behind Blast

Blast was launched in late 2023 as an Ethereum Layer-2 network that promised something most rollups did not: native yield. Instead of users having to deploy capital into decentralized finance (DeFi) protocols themselves, Blast claimed it could generate returns automatically on bridged ETH and stablecoins.

The project was backed by the team behind Blur, one of the most successful non-fungible token (NFT) marketplaces at the time, which immediately gave it credibility and attention.

Users were encouraged to bridge funds into the network in exchange for “points” that would later convert into BLAST tokens. Withdrawals were initially locked, and access was gated through referral codes, creating both urgency and exclusivity.

At launch, there were few live applications and little actual on-chain activity, but that hardly mattered. The promise of future rewards, combined with the reputation of the team, was enough to pull in capital at scale.

The entire design was built around accumulation first and utility later — a structure that worked extremely well in attracting deposits, but left an open question about what would keep users engaged once incentives faded.

Peak valuation and the illusion of scale

The BLAST token launched at around $0.020 and quickly ran up to an intraday high of $0.0281. At that point, the project was valued at nearly $2.8 billion on a fully diluted basis, with a circulating market cap close to $480 million.

Daily active users have dropped below 4,000, from its peak of millions when it launched. BLAST trades between $0.00079 and $0.00081, down more than 95% from post-launch highs, with a circulating market capitalisation fluctuating between $40 million and $53 million and daily spot trading volumes frequently below $8 million.

Official social media accounts have been inactive for months, developer activity has slowed dramatically, and the network no longer features meaningfully in discussions about Ethereum’s scaling roadmap.

This article examines how a network that once absorbed billions of dollars in capital lost relevance without collapsing, and what Blast’s trajectory reveals about the mechanics of hype, incentives, and attention in crypto markets.

A market structurally primed for excess

Blast launched publicly on November 21, 2023, at a moment when several structural forces aligned in its favor. Ethereum transaction fees remained volatile, Layer-2 (L2) networks were increasingly viewed as essential infrastructure rather than experimental sidechains, and investors were actively searching for the next dominant execution layer.

At the same time, yields across DeFi had compressed significantly. Ethereum staking returns had stabilized between 3% and 4%, while stablecoin yields across most protocols had fallen below levels that many users considered attractive.

Blast’s core proposition addressed this dissatisfaction directly. The protocol promised that assets bridged to the network would become yield-bearing by default. ETH deposits would automatically earn staking rewards through integrations with Lido, while stablecoins such as USDC and USDT would generate yield through MakerDAO-linked strategies, rebased into Blast’s native stablecoin, USDB.

These yields were advertised at approximately 4% for ETH and between 5% and 8% for stablecoins at launch, with later promotional material citing annualized returns as high as 11.5% and, at times, “up to 50%” under certain incentive conditions.

From a technical perspective, Blast was an optimistic rollup compatible with the Ethereum Virtual Machine (EVM), similar in structure to Optimism and Arbitrum. Transactions happened off-chain and were settled on the Ethereum mainnet at intervals, which helped keep fees low and throughput high. That part wasn’t new.

What set Blast apart was the way it sold the idea. The network wasn’t just a place to use yield-generating apps—it presented yield as something built directly into the chain itself.

That message landed perfectly in a market already trained to hunt for easy, passive returns.

Founder reputation as financial collateral

Equally important to Blast’s rapid adoption was the identity of its founder. Tieshun “Pacman” Roquerre had previously launched Blur, an NFT marketplace that successfully displaced OpenSea as the dominant venue for professional traders by aggressively redistributing value through token incentives.

Early Blur users collectively received hundreds of millions of dollars worth of BLUR tokens, creating a cohort of traders who associated Pacman’s projects with outsized financial upside.

That association proved decisive. When Blast launched, users did not demand detailed technical documentation or comprehensive risk disclosures. Instead, they bridged capital. The assumption was implicit: if Pacman had delivered once, he would deliver again.

Blast leaned heavily on that trust by raising $20 million from well-known venture firms such as Paradigm, Standard Crypto, and eGirl Capital. In crypto, this kind of backing often acts as a stamp of approval.

For many users, the presence of big-name investors signals credibility, even when the product itself is still early, or the fundamentals have not caught up with the money flowing in.

Capital before a network

One of the most controversial aspects of Blast’s launch was its sequencing. Users were encouraged to deposit funds before the network itself was live. There was no fully operational mainnet, no production-grade testnet, and limited public documentation explaining how assets were managed during the interim period.

Deposits flowed into a multisignature wallet controlled by a small group of signers, with withdrawals disabled until the mainnet launch scheduled for February 29, 2024.

In return, users were promised yield and points.

That points system quickly became the real driver of Blast’s growth. Points are accumulated over time based on how much a user deposits and how long the funds stay locked. Referrals pushed this even further.

Anyone who brought in new users earned a share of the points their invitees collected, turning the system into a self-reinforcing loop. Early access required a referral code, which added a sense of scarcity and insider status, even though the protocol itself was meant to be open.

The response was immediate. Within the first 24 hours, more than $130 million was bridged into the network. By December 2023, deposits had crossed $900 million. By July 2024, Blast’s total value locked had climbed to between $2.2 billion and $2.7 billion, briefly putting it ahead of several long-standing L2 networks.

But the on-chain data told a different story. Money was pouring in, yet actual usage lagged behind. Capital kept accumulating, while real transactional activity failed to keep pace — an imbalance that would later become impossible to ignore.

A significant portion of wallets deposited assets and conducted little to no further activity. The majority of interactions were related to point optimisation rather than application usage.

Blast had succeeded in attracting money without creating sustained demand for blockspace.

The trap: Locked liquidity

One of Blast’s most damaging design choices was also one of its least questioned. At the time, it was presented as a feature rather than a flaw.

From the very beginning, user funds were locked. Withdrawals were disabled until the mainnet launch, meaning that once funds entered Blast, there was no way to pull them out. It was sold as a protective measure meant to stabilize liquidity and discourage short-term speculation. In reality, it masked the true level of demand and made the network appear stronger than it actually was.

Because funds could not be withdrawn, total value locked (TVL) could only move in one direction. Every deposit made Blast appear larger, stronger, and more successful than it actually was. On-chain dashboards showed billions of dollars committed to the network, but that commitment was not voluntary. It was enforced by design.

That distinction mattered far more than most people realized.

Locked liquidity removed price discovery from the system. There was no way to tell how much of the capital genuinely believed in the project and how much was simply waiting for an exit. Growth appeared organic, but it had never been tested. Demand looked strong, but it had not been given the chance to express doubt.

When withdrawals were finally enabled, the reality surfaced immediately. Users who had appeared patient began selling. Capital that had looked loyal turned out to be opportunistic. The same mechanism that had inflated Blast’s perceived success now accelerated its decline.

In effect, Blast had borrowed credibility from the future. When that future arrived, repayment was unavoidable.

The irony is that the system worked exactly as intended. It attracted capital, boosted metrics, and created momentum. By postponing the moment when users could make a real decision, Blast made the eventual exit sharper and far more damaging.

Tokenomics and the airdrop inflection point

Blast’s tokenomics were ambitious in scale. The BLAST token had a total supply of 100 billion units, of which 50% was allocated to the community over a three-year distribution period. Of this, 17% was released in the initial airdrop in June 2024.

Contributors received 25.5% of the supply, investors 16.5%, and 8% was reserved for ecosystem development.

The airdrop was positioned as a reward for early participation, with allocations divided between users who bridged assets, users who interacted with decentralized applications (dApps), and the Blur Foundation. Market expectations, however, had drifted far beyond the actual distribution.

Public complaints emerged almost immediately. One prominent investor reported depositing more than $50 million worth of assets and receiving an airdrop valued at approximately $100,000.

Smaller users quickly grew frustrated. Months of farming points ended up paying off in rewards that, while noticeable, rarely felt worth the time, effort, or risk they had taken.

Things got worse once the airdrop made BLAST freely tradable. With liquidity suddenly available, the system that had kept funds tied to the network no longer worked. Selling the token became the obvious choice, and many users did just that.

Within a few weeks of launch, BLAST dropped below its initial listing price. The tokens set aside for user rewards lost much of their value, making future payouts far less appealing.

The feedback loop of decline

By August 2024, Blast’s total value locked had fallen under $1 billion. By mid-2025, it had shrunk even further to around $65 million. Money left the network, users pulled out, and the cycle of decline fed on itself, leaving Blast a fraction of what it had once been.

By December 2025, it fluctuated between $55 million and $60 million, according to DeFiLlama data. Daily active users fell from more than 160,000 at peak to fewer than 4,000.

The BLAST token followed a similar trajectory. From a high of $0.0281, it declined to approximately $0.0025 by late 2025 and continued falling into early 2026. Liquidity deteriorated, with some decentralised exchange pools exhibiting extreme slippage. At times, selling modest quantities of BLAST resulted in price impacts exceeding 90%.

As the price of BLAST tokens fell, the yields paid out in the token quickly lost their appeal. Lower rewards prompted users to leave, and as users withdrew, developers and projects began pulling back as well.

The network never managed to produce applications that could keep people engaged without ongoing incentives, leaving Blast dependent on a story that had already lost its credibility.

Structural weaknesses and unanswered questions

From the start, Blast faced ongoing criticism over centralization and a lack of transparency around risk. Funds were initially held in a 3-of-5 multisignature wallet, which raised questions about how concentrated control was.

Withdrawal delays restricted liquidity and limited what users could do with their assets. The network also depended heavily on other protocols like Lido and MakerDAO, creating weak points that were never fully tested under real-world stress or attacks.

Security problems only made things worse. During the airdrop, phishing attacks hit high-value wallets, with one single incident costing users more than $217,000. Other exploits in apps built on Blast led to losses of tens of millions, further shaking trust in the platform.

None of these events alone destroyed the protocol. But together, they revealed how fragile it really was. When rewards were high, users overlooked the risks. Once those incentives disappeared, that patience disappeared too.

Silence as an ending

By mid-2025, Blast’s official social media accounts were mostly quiet. Updates from the founder became sporadic and then stopped entirely. Even critics stopped talking. In crypto, this kind of silence isn’t neutral—it usually means the project has been abandoned.

As Ethereum Layer-2 activity consolidated around a small number of dominant networks such as Base, Arbitrum, and Optimism, Blast was left behind. The protocol continued to function, but without users, liquidity, or narrative momentum.

By January 2026, Blast existed primarily as an artefact of a specific moment in crypto history—a reminder of how quickly belief can be manufactured, and how quietly it can disappear.

The broader lesson

Blast demonstrates that in crypto markets, total value locked is not adoption, incentives are not loyalty, and hype is not durability. Capital attracted by rewards behaves differently from capital attracted by necessity. Once rewards end, only utility remains, and Blast failed to establish itself as necessary.

The network did not collapse because it was fraudulent or incompetent. It collapsed because it confused attention with permanence.

In crypto, hype does not die when something breaks. It dies when nothing replaces the promise.

Blast is still operational. The contracts are still executed. The token still trades. But the market has moved on, and in crypto, that is the final verdict there is.

Also Read: Monad’s Post-Mainnet Hangover: Massive Talks But No Real Traction