In the final week before April 18, 2026, a little-known Web3 music token called $RAVE went from $0.25 to above $26 — a 6,000%+ vertical move that briefly pushed RaveDAO’s market capitalization to nearly $4 billion and into the CoinGecko top 50. Retail traders on Binance, Bitget, and Gate had lined up and made huge bets on a possible crash, but they lost tens of millions of dollars.

Here’s the uncomfortable part: the majority of them were not wrong about RaveDAO. They were wrong about how to trade it.

The paradox at the heart of the RaveDAO short squeeze

Before the rally began, 74% of Binance traders were positioned short on $RAVE. In other words, three out of every four retail participants looked at a low-float token with visible insider wallets and correctly concluded the price was unsustainable. Their thesis was right. Their execution was a disaster.

Of the roughly $43 million in RAVE futures liquidations within a single 24-hour window, over $32 million came from short positions. One day saw $17 million in shorts wiped out in a single session. The retail crowd that saw the manipulation clearest got punished the hardest.

This is the signature of a well-engineered short squeeze on a low-float crypto token — and it’s the RaveDAO trading lesson every leveraged trader needs to internalize.

Mistake #1: Treating $RAVE like a normal overvalued asset

Retail shorts assumed mean reversion would arrive the way it does on liquid large-cap tokens. It didn’t, because $RAVE’s supply structure made mean reversion impossible on the shorts’ timeline.

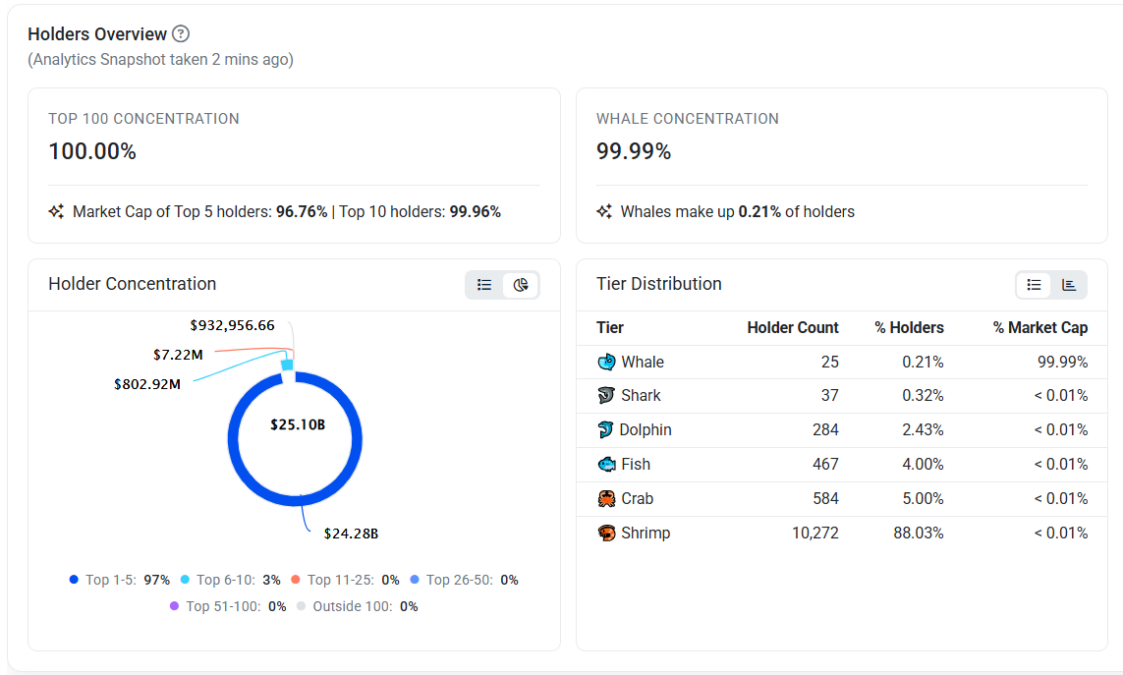

Only 248 million of RAVE’s 1 billion total supply was in circulation — just 24% of the float. Three Gnosis Safe wallets, widely presumed to be team-controlled, held 75.2%, 9.87%, and 4.67% of the entire supply, respectively. Expanded to the top 10 wallets, concentration exceeded 98%.

When insiders control nearly the entire float, they control price discovery. Shorting into that structure isn’t a contrarian bet against an overvalued token — it’s lending ammunition to the people holding the loaded weapon. The first lesson of trading low-float insider tokens: concentration risk flows in both directions.

Mistake #2: Misreading the Bitget transfer as a dump signal

This is where the trap closed.

Roughly 10 hours before the vertical move began, wallets linked to the RaveDAO deployer moved 18.58 million tokens (about $19 million in notional value) onto Bitget. No announcement. No disclosure. Just a visible, on-chain transfer from insider wallets to a centralized exchange while the price was still below $0.50.

To experienced on-chain readers, this looked like textbook distribution: insiders about to dump. Shorts piled in on Binance and Bitget perpetuals. The funding rate flipped decisively negative.

It was bait.

Over the next two days, while retail shorts accumulated, approximately $32 million worth of RAVE was quietly pulled back on-chain as spot price was aggressively pumped. The Bitget deposit was never intended for distribution. It was a signal designed to manufacture short interest so that coordinated spot buying could trigger cascading liquidations.

The deeper lesson for on-chain traders: on a concentrated token, an exchange inflow from insider wallets is not automatically a dump signal. Sometimes it is a trap laid specifically for traders who think they’re reading the chart correctly.

Mistake #3: Assuming CEX listings implied due diligence

Many retail traders reasoned that a token simultaneously listed on Binance, Bitget, Gate, and OKX must have passed some basic float and concentration check. This assumption is doing a lot of unearned work.

The same centralized exchanges (CEXs) that listed $RAVE also hosted the perpetual futures market that made the squeeze mechanically possible. With only 24% of supply circulating, opening deep derivatives markets on $RAVE created a structural mismatch: leveraged positions far exceeded the liquid spot supply available to settle them. Shorts had almost no room to cover cleanly once buying pressure arrived.

ZachXBT’s April 18 post directly named @heyibinance and @GracyBitget, calling on both exchanges to “do better and launch internal investigation offboarding the responsible actors.” Whether Binance, Bitget, or Gate respond with meaningful action — or whether this episode joins the growing list of what traders are now calling Binance “crime tokens” — remains an open question.

For retail, the takeaway is simpler: a tier-one CEX listing is not a diligence stamp. It’s a liquidity venue. Read the token’s wallet distribution yourself.

Mistake #4: Using leverage when the Money Flow Index was pinned at 97+

Technical indicators screamed the warning, and retail traders using leverage ignored it.

$RAVE’s Money Flow Index hit 97.48 during the rally. The MFI caps at 100. Readings approaching 98 mean that nearly every capital flow event in the measurement window has been a buying event — an extreme that appears almost exclusively during parabolic short squeezes, not organic accumulation. RSI above 95 told the same story.

Spot shorts can wait out these readings. Perpetual futures shorts cannot — they get liquidated at the wick. The mistake wasn’t the bearish thesis. It was expressing that thesis through an instrument that forced traders out of position before their thesis had time to play out.

If you’re trading a suspected pump-and-dump, the question isn’t “am I right about the direction?” It’s “can my instrument survive being wrong for longer than I expected?” Leverage on low-float squeeze candidates answers that question badly.

Mistake #5: The long-side retail trap at $8 and $9

Not every retail loss came from shorts. The other half of the story is the traders who bought $RAVE at $8 or $9 believing they were catching a momentum trade early.

They were not early. They were exit liquidity. When three wallets hold 90% of the supply and have already positioned tokens on an exchange, “getting in before the top” is a contradiction in terms — the top is whatever price those three wallets decide to distribute at. Retail longs at $8 were buying a move that had been set up at $0.30 by people who still controlled the remaining 752 million unreleased tokens.

What retail should watch instead

The RaveDAO rally wasn’t a failure of analysis. It was a failure of position sizing, instrument choice, and structural awareness. Before entering any position on a low-float insider token, the checklist is:

Float percentage versus total supply. Top-10 wallet concentration. Recent movements from team-controlled wallets to centralized exchanges. Whether perpetual futures open interest is disproportionate to spot liquidity. Funding rate direction — a sharply negative funding rate means shorts are already crowded and vulnerable. Whether the token has any vesting cliffs or unlock events approaching.

The real RaveDAO lesson

The retail traders who shorted $RAVE were not naive. They read the on-chain data, saw the insider concentration and made the correct fundamental call. What they underestimated was that on a token where 90% of supply sits in three wallets, the insiders do not need the market to agree with them to win. They only need leverage to be available on the other side.

Being right about a scam is not the same as being able to profit from shorting it. On concentrated, low-float tokens listed across Binance, Bitget and Gate, the asymmetry is structural — and it favors the wallets that already control the float.

The next $RAVE is already being deployed somewhere. The traders who remember this lesson will be the ones who walk away from the short.

Also Read: ZachXBT Offers $10,000 Bounty in RAVE Token Pump n’ Dump