Key Highlights

- No Tax Relief: Crypto gains continue to be taxed at 30%, with 1% TDS on transactions.

- Stricter Reporting: Section 509 and 446 create enforceable disclosure requirements with daily fines and inaccuracy penalties.

- Serious Consequences: Failure to comply can lead to financial penalties or even imprisonment for significant TDS defaults.

At first glance, India’s Union Budget 2026–27 appeared to have nothing new to say about cryptocurrency. Finance Minister Nirmala Sitharaman’s speech made no reference to crypto, virtual digital assets (VDAs), or blockchain — continuing a pattern of public silence that has frustrated investors and industry players for years.

The real story of crypto in Budget 2026 isn’t in the Finance Minister’s speech. Most of the important details are hidden in the Finance Bill, 2026.

A close look shows that crypto taxes haven’t changed, but the government has quietly tightened the rules on reporting and enforcement for digital assets. The message is clear: India isn’t fully regulating crypto yet, but it won’t allow gaps in reporting, disclosure, or tax compliance.

It’s also worth noting that the Finance Bill, 2026 includes specific sections on crypto reporting and penalties. Sections like 509, 446, 476, and 276B outline what exchanges, intermediaries, and investors must do. They also set out fines, penalties, and in some cases, even jail for serious violations.

In the sections that follow, we’ll go through how these rules work in practice, the types of penalties, and what it means for crypto users and platforms in India.

A budget that chooses enforcement over reform

For much of the crypto industry, expectations going into Budget 2026 were modest but specific. Exchanges and investors weren’t necessarily asking for full-scale liberalization, just some rationalisation of the tax regime introduced in 2022, particularly the 1% TDS that many say has choked liquidity.

None of that happened.

Instead, the Finance Bill shows a clear policy direction. Rather than changing crypto taxes or announcing a full regulatory plan, the government is focusing on strict compliance, using the Income-tax Act as the main tool.

This is intentional. By strengthening reporting rules, widening definitions, and adding clear penalties—including jail terms, the government is tightening control without opening the debate on whether crypto should be fully regulated.

A shift in focus: From tax reform to enforcement

The Union Budget 2026–27 sends a clear signal to the Indian crypto community: you must be transparent. Many investors and exchanges were hoping for relief from the 30% tax on gains or the 1% TDS, but the government has taken a different approach.

Instead of reducing taxes, it has made reporting, disclosure, and compliance stricter.

If you hold crypto or run a crypto platform in India, Budget 2026 does not change how much tax you pay. What changes is what happens if you fail to report correctly.

The big shift: Crypto reporting is no longer a grey area

Until now, crypto exchanges and intermediaries were required to submit transaction data to the Income-tax (IT) Department, but the consequences for lapses were unclear. Delays, incomplete filings, or weak due diligence often existed in a grey zone.

Budget 2026 closes that gap.

Section 509: The Backbone of Crypto Reporting / Surveillance

Most retail investors will never read Section 509, but it is now one of the most important provisions governing crypto in India.

Section 509 requires specified persons to furnish detailed statements of crypto-asset transactions. This includes information on users, transaction values, timing, and other prescribed particulars.

The new penalties under Section 446 exist solely to enforce Section 509. In effect, the government has turned reporting obligations from a procedural requirement into a legally enforceable duty with financial and criminal consequences.

The memorandum accompanying the Finance Bill states that these changes are intended to “strengthen compliance and discourage inaccurate or incomplete reporting” — a line that reflects the government’s broader discomfort with opacity in crypto markets.

A new penalty framework for crypto reporting

What stands out in this framework is that penalties now attach to routine operational failures, not just deliberate non-compliance. A missed filing deadline, an unresolved mismatch in transaction data, or incomplete user information can now attract penalties even in the absence of tax evasion.

For platforms handling high transaction volumes, this introduces a new layer of risk. Reporting is no longer a back-office formality handled at the end of the financial year. It becomes a continuous obligation that requires tighter internal coordination between compliance, finance, and technology teams.

For smaller intermediaries and newer platforms, the change is even more consequential. Without robust reporting systems in place, even minor lapses can accumulate into meaningful financial exposure over time.

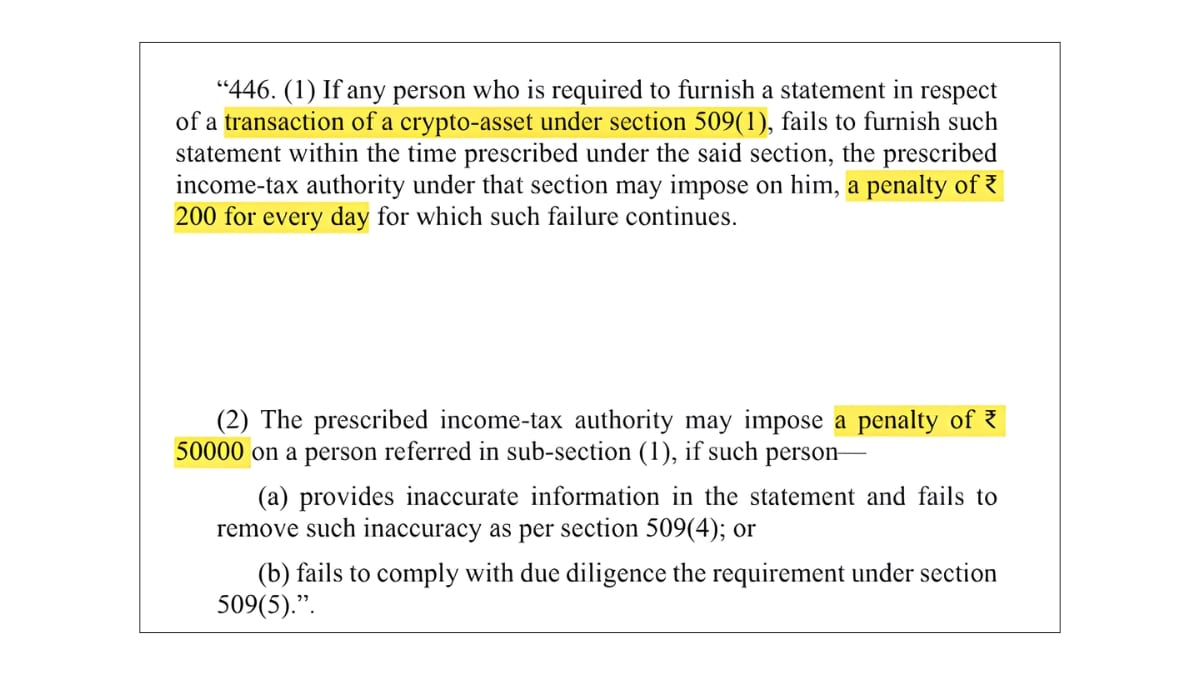

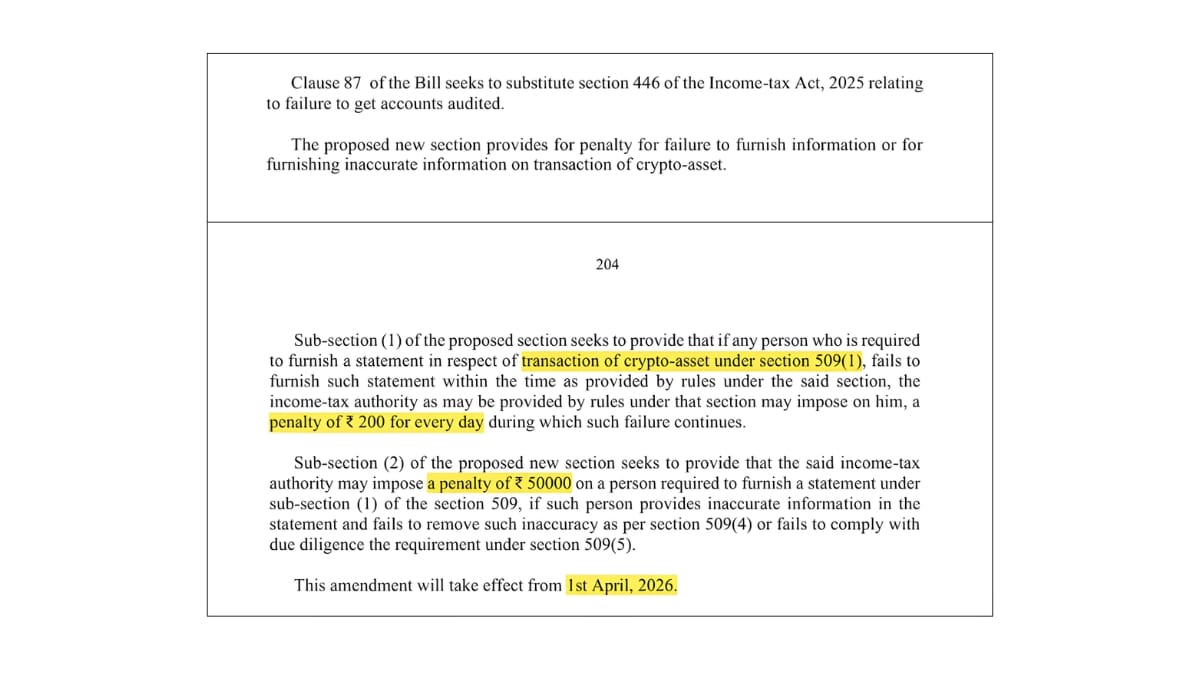

What Section 446 changes

The Finance Bill replaces Section 446 of the Income-tax Act, 2025, and sets up a clear penalty system for crypto reporting mistakes. This section is directly connected to Section 509, which requires platforms and intermediaries to submit detailed statements about crypto transactions.

In simple terms: if you are required to report crypto transactions and you don’t or you do it inaccurately, there is now a clear financial cost.

A reporting entity that fails to submit the prescribed statement on time can be penalised ₹200 per day for every day the default continues. This is not a one-time fine; it accumulates until compliance is achieved.

The daily penalty explained with an example

If a crypto exchange or reporting entity fails to submit the required transaction statement on time, it can be fined ₹200 per day for every day the delay continues.

For example, if a platform delays filing its statement by 30 days, the penalty alone would be ₹6,000. If the delay stretches to 100 days, the fine rises to ₹20,000.

This penalty continues until compliance is achieved.

The ₹50,000 inaccuracy penalty

More importantly, if inaccurate information is provided and not corrected after being flagged, or if due diligence requirements are ignored, the tax authority can impose a flat penalty of ₹50,000.

This applies even if the reporting entity eventually files the statement and applies to exchanges, wallet providers, intermediaries, and any entity covered under Section 509.

The rules will take effect from April 1, 2026, applying to the 2026–27 tax year onwards.

When crypto tax defaults become criminal offences

Reporting penalties are only one side of the story. The Finance Bill also reinforces — and in practice sharpens — the consequences for failing to deposit tax deducted at source on crypto transactions.

This is where enforcement turns serious.

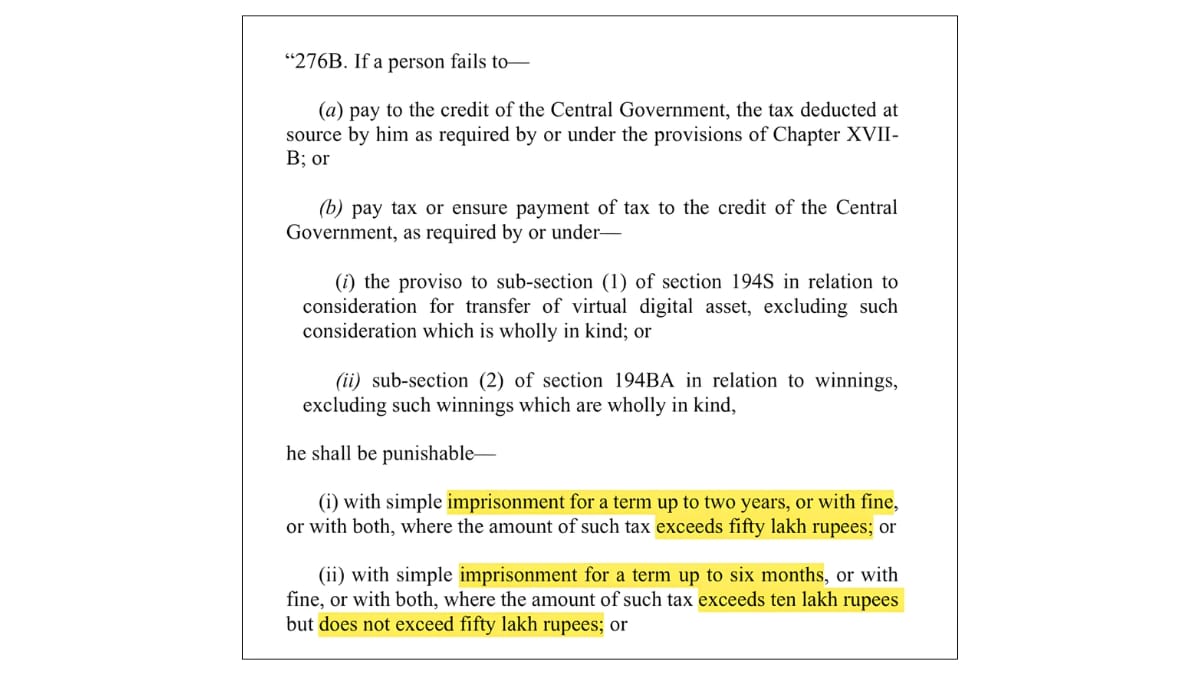

What Sections 476 and 276B actually mean

Sections 476 and 276B deal with failure to pay tax to the credit of the Central Government. Budget 2026 explicitly applies these provisions to tax deducted on consideration received from the transfer of virtual digital assets.

The language is unambiguous.

“If a person fails to pay tax or ensure payment of tax… in respect of any sum by way of consideration for transfer of a virtual digital asset… he shall be punishable with simple imprisonment for a term up to two years, or with fine, or with both, where the amount of such tax exceeds fifty lakh rupees.”

For unpaid tax between ₹10 lakh and ₹50 lakh, imprisonment of up to six months may apply. In other cases, fines can be imposed. Transactions where consideration is wholly in kind are excluded.

What matters here is not just the penalty, but the signal. Crypto-related TDS failures are now explicitly placed in the same enforcement bucket as other serious financial violations.

Crypto’s definition gets tighter and broader

Another change that may appear technical but has real consequences is the expansion of how crypto is defined under tax law.

How the VDA definition has quietly changed

The Finance Bill makes it explicit that “crypto-assets” built on distributed ledger technology fall within the definition of virtual digital assets.

This aligns India with the Organization for Economic and Development (OECD)’s Crypto-Asset Reporting Framework (CARF) and shuts the door on arguments that certain blockchain-based instruments fall outside the VDA net.

In other words, innovation in naming or structure will no longer be enough to escape classification as crypto for tax and reporting purposes.

Simply put, changing labels or structures will no longer help avoid classification as crypto.

What didn’t change and why that matters

Despite the sweeping compliance overhaul, the core tax framework introduced in the 2022 Budget remains untouched.

Crypto gains are still taxed at 30%, with 1% TDS on every transaction, and no provision to offset losses. This rigidity continues to frustrate industry participants who argue that the structure discourages domestic participation.

As Ashish Singhal, co-founder of CoinSwitch, put it: “The current tax framework presents challenges for retail participants by taxing transactions without recognising losses, creating friction rather than fairness.”

He added: “A reduction in TDS on VDA transactions from 1% to 0.01% could improve liquidity, ease compliance, and enhance transparency while preserving transaction traceability.”

That argument, for now, has found no takers in North Block.

Industry leaders continue to warn that this structure discourages domestic participation and pushes activity offshore, but Budget 2026 offers no relief on this front.

The regulation paper that has yet to arrive

Union Budget 2026 does not mention any crypto regulation paper.

This is despite repeated indications over the past year that such a paper was being worked on. At various points, officials suggested it would be released soon, but no formal timeline has ever been announced.

After the Budget, that position remains unchanged.

For now, crypto in India continues to be shaped through a mix of measures rather than a single law. These include tax provisions, registration requirements with the Financial Intelligence Unit (FIU), and alignment with global reporting standards. Together, they set the compliance framework, even though there is still no dedicated crypto legislation.

Budget 2026 follows the same pattern. It introduces no new guidance on when a broader regulatory framework may be released.

Stablecoins, CBDCs, and what the silence suggests

There has been no shortage of public statements urging India to pay attention to stablecoins, particularly for cross-border payments. Yet no announcement on framework for private INR-pegged stablecoins have been made in Budget 2026.

The focus remains firmly on the Digital Rupee, India’s central bank digital currency. If an INR-linked stablecoin does emerge, current signals suggest it will be sovereign-backed and tightly controlled, rather than privately issued.

The bottom line

Union Budget 2026 does not ban crypto. It doesn’t encourage it either.

Instead, it does something more consequential: it locks crypto into India’s tax and reporting machinery with far fewer escape hatches than before. Daily fines, fixed penalties, expanded definitions, and the threat of imprisonment all point in one direction.

Crypto may still be missing from Budget speeches, but it is very much on the government’s enforcement map.

For anyone operating in the space, the message is unmistakable: if you are in crypto, you must now be visible, accountable, and precise, or be prepared to pay for it.

For investors and platforms alike, the message is simple: report accurately, report completely, or be prepared to pay for it.