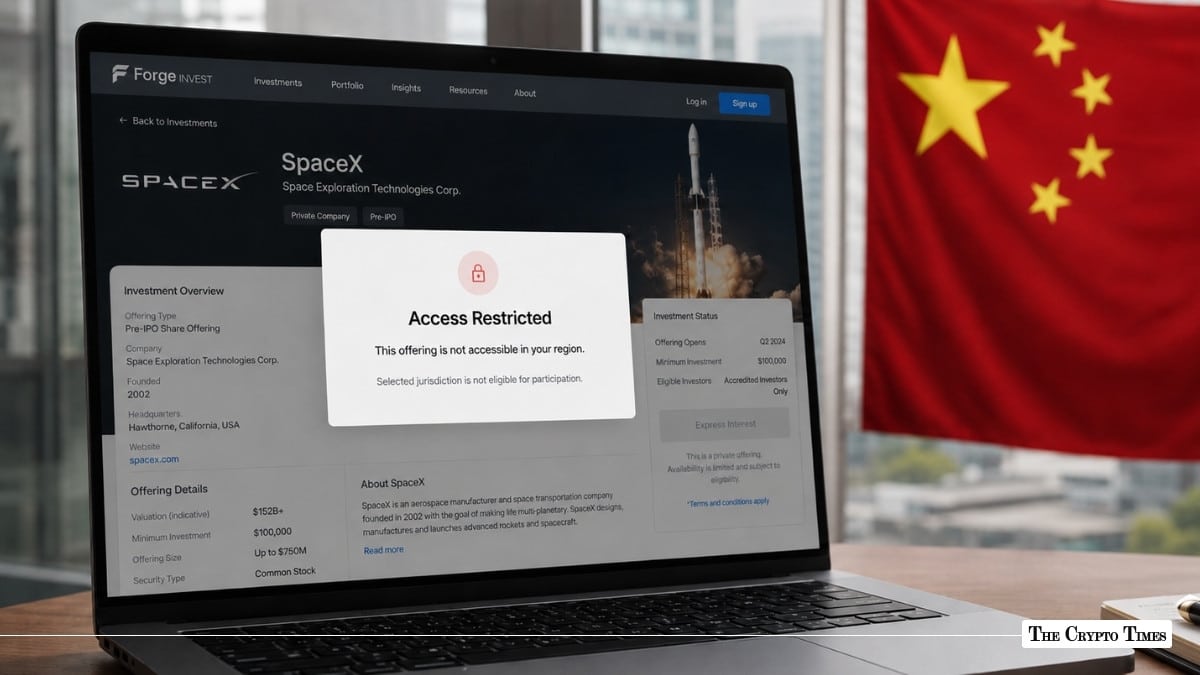

Lead underwriters managing SpaceX’s $75 billion initial public offering have instructed banks in the underwriting syndicate not to accept orders from investors in mainland China and Hong Kong, citing US export control rules around critical defense technology.

The restriction, first reported by Bloomberg, applies to both institutional and private banking clients in those jurisdictions. The exclusion has practical consequences beyond the IPO itself. SpaceX’s website and IPO marketing documents became inaccessible from mainland China and Hong Kong on June 5, while remaining available from other major Asian markets. The company’s roadshow had kicked off the previous day in New York.

For TCT readers, the more interesting structural question is what happens next. Chinese and Hong Kong investors who would otherwise have participated in what is expected to be the largest IPO in history are now structurally excluded from regulated equity exposure to a company valued at approximately $1.75 trillion. The crypto industry has spent the past 18 months building exactly the kind of products that could fill that gap.

The ITAR Logic and Its Limits

The exclusion is built on the US International Traffic in Arms Regulations, which govern the export of defense-related technologies and technical data. SpaceX’s portfolio of defense-adjacent and dual-use products — including Starshield (the military variant of Starlink), national security space launch contracts with the U.S. Department of Defense, and classified satellite deployments — places significant portions of the company’s technology footprint within ITAR’s reach.

The underwriter directive, according to Bloomberg’s sources, stems from “internal guidance” rather than a direct regulatory order. Goldman Sachs and Morgan Stanley, the lead bookrunners, have not publicly commented on the rationale. The decision reflects what Bloomberg described as “regulatory and compliance risks” associated with permitting Chinese or Hong Kong capital to flow into a U.S. company with sensitive defense technology exposure.

The underlying tension is structural. SpaceX is simultaneously a private rocket company, a global telecommunications operator (via Starlink), an AI compute infrastructure builder (via the xAI merger), and a defense contractor. Any of those facets could theoretically attract Chinese investor interest. ITAR’s framework allows the U.S. government, and by extension U.S.-regulated underwriters, to restrict that interest at the point of equity issuance.

What ITAR does not cleanly address is synthetic exposure to the same companies through derivatives that reference the underlying equity without transferring any actual shares, technical data, or controlled defense items.

Hyperliquid’s SpaceX Perps Market

Among the most active venues for synthetic SpaceX exposure is Hyperliquid, the on-chain perpetual futures exchange that has emerged as a major destination for pre-IPO equity speculation.

The contracts operate as synthetic derivatives — they track the implied valuation of SpaceX shares using oracle-fed pricing models, but no actual shares change hands. Traders deposit collateral on Hyperliquid’s Layer-1 blockchain, take long or short positions on SpaceX’s price action, and settle in stablecoins. The structure is operationally identical to Hyperliquid’s Bitcoin or oil perpetual futures markets, just with a private company’s implied equity value as the reference asset.

Binance launched pre-IPO perpetual futures starting with SpaceX on May 21, 2025, as part of co-CEO Richard Teng’s “super app” strategy. Other venues, including Robinhood, Kraken, and Bitget’s Reality Platform, have launched tokenized pre-IPO share products that offer similar synthetic exposure with varying structures.

For Chinese and Hong Kong investors excluded from the traditional IPO process, these products represent the only operationally accessible path to SpaceX exposure. They are not perfect substitutes — there are no voting rights, no actual share ownership, no post-IPO dividend claims — but they capture the most economically meaningful component: price exposure.

The ITAR Gray Zone for Crypto Derivatives

The legal question that the SpaceX IPO restriction raises is whether ITAR’s scope extends to synthetic perpetual futures and tokenized derivatives that reference U.S. defense-adjacent companies. The conventional interpretation is that it does not — ITAR governs the export of defense articles, technical data, and defense services, not the price exposure to publicly or privately held equity in defense-related companies.

A perpetual futures contract on SpaceX does not transfer any SpaceX shares, any SpaceX technical data, or any SpaceX defense services. It transfers price exposure derived from an oracle that itself references publicly observable pricing in secondary markets or implied valuation models. The exposure is economic, not technological.

That said, the U.S. regulatory framework has historically adapted to new product structures when sufficient policy pressure exists. The Treasury Department’s Office of Foreign Assets Control (OFAC) has expanded the scope of sanctions to cover crypto wallets and decentralized protocols when conducting enforcement against sanctioned entities.

The CFTC has established a case-by-case review framework for perpetual contracts on non-Bitcoin asset classes. If U.S. policymakers decide that synthetic exposure to ITAR-controlled companies undermines the policy logic of underwriter restrictions, the legal interpretation could evolve.

For now, the policy gap is real. Chinese and Hong Kong investors blocked from buying SpaceX shares directly can, in theory, gain economically equivalent exposure through crypto-native perpetual futures on Hyperliquid or Binance, with no underwriter directive currently restricting that activity.

Practical Constraints

The theoretical accessibility of these products comes with practical constraints. Hyperliquid’s terms of use explicitly block U.S. residents and certain sanctioned jurisdictions, though enforcement relies primarily on IP-based geofencing that VPN users routinely bypass. Hyperliquid does not restrict mainland Chinese or Hong Kong users by default, but the platform’s recent wallet ban incidents involving third-party AML screening have shown the platform retains discretion over individual access.

Binance similarly restricts U.S. customers but maintains operations across most Asian markets, including with adapted local subsidiaries. Robinhood’s pre-IPO tokenized share products are limited to specific geographies. Bitget’s Reality Platform operates through licensed brokerage partners and applies its own jurisdictional restrictions.

For sophisticated Chinese and Hong Kong investors with crypto-native trading infrastructure, the practical path remains open: hold stablecoin reserves, access Hyperliquid or Binance through standard onboarding, and trade SpaceX perpetual futures at scale. The total volume that could rotate from blocked IPO demand to crypto-native synthetic exposure is impossible to quantify in advance, but the underlying capital pool — Chinese and Hong Kong institutional and high-net-worth interest in SpaceX — is meaningful.

The Broader Pattern

The SpaceX exclusion fits a broader 2026 pattern in which U.S. technology and AI companies are increasingly declining or restricting Chinese capital due to national security and data-security concerns. This represents a structural reversal from the previous decade, when Chinese venture capital and private equity firms regularly invested in Silicon Valley startups.

The same restrictions are likely to apply to upcoming mega-IPOs from OpenAI and Anthropic, both of which have substantial defense and national security exposure through their work with U.S. government agencies. If the SpaceX precedent holds, both companies will likely face similar underwriter restrictions on Chinese and Hong Kong capital participation when they reach public markets.

The implication for the crypto industry is that synthetic pre-IPO exposure may move from a niche speculative product to a structural piece of global capital infrastructure. If U.S. mega-IPOs systematically exclude Chinese capital while crypto-native derivatives continue to offer accessible synthetic exposure, the volume routed through Hyperliquid, Binance, and similar venues could grow substantially in the next 12 to 24 months.

For SpaceX itself, the exclusion is a calculated trade-off. Losing access to Chinese and Hong Kong capital is meaningful but not existential at a $1.75 trillion valuation — the U.S., European, Japanese, Korean, and other Asian markets remain fully accessible. For the crypto industry, the trade-off may run in the opposite direction. A structural source of global investor demand has just been routed away from traditional capital markets infrastructure and toward the on-chain alternative.

The IPO is expected to price in mid-June. The first signal of how Chinese and Hong Kong investor capital responds will be visible in Hyperliquid and Binance perpetual futures volume in the days following the SpaceX listing.