Key Highlights

- On March 1–3, 2026, Iranian drone strikes knocked three AWS data centers offline in the UAE and Bahrain—the first time a major cloud provider’s infrastructure has been destroyed by military action.

- While Ethereum’s consensus layer remained unaffected, the attacks exposed critical fragilities in the network’s access layer: 60% of execution nodes run on cloud services, and 70–80% of RPC traffic flows through a handful of centralized providers.

- Layer 2 networks, DeFi protocols, and wallet services like MetaMask experienced cascading disruptions, underscoring systemic concentration risk that the crypto industry has long warned about but failed to address.

- Early signals from APAC and Latin America suggest a growing shift toward geographic diversification and home-staking infrastructure, accelerated by DVT adoption and regulatory clarity in Singapore, Japan, and Hong Kong.

The March 2026 attacks on Middle East cloud infrastructure reveal systemic risks across Ethereum’s execution layer, RPC providers, and Layer 2 networks — even as the consensus layer held firm.

The Strikes: What Happened

In the early hours of March 1, 2026, a wave of Iranian drones struck targets across the United Arab Emirates and Bahrain as part of retaliatory operations following the killing of Iran’s supreme leader during joint US-Israeli military action. Among the targets hit were three Amazon Web Services facilities — two in the UAE and one in Bahrain — marking an unprecedented escalation in the intersection of military conflict and digital infrastructure.

The first impact was recorded at approximately 4:30 AM PST, when AWS availability zone mec1-az2 in the UAE was struck. The attack caused structural fires, prompting local authorities to cut power to contain the blaze. By Monday evening, AWS confirmed that a third facility in Bahrain had sustained collateral damage from a nearby drone impact, with fire suppression systems causing additional water damage to server hardware.

The UAE military reported intercepting 137 ballistic missiles and 209 drones during the assault, but debris and direct hits still caused significant damage across the region. For the first time in history, a hyperscale cloud provider’s data centers were taken offline not by software failure, power outage, or natural disaster — but by military action.

Ethereum’s Cloud Dependency: The Numbers

The attacks brought renewed scrutiny to a vulnerability the Ethereum community has debated for years: the network’s deep reliance on centralized cloud providers. The data paints a concerning picture of concentration risk that extends far beyond what the decentralization narrative suggests.

Node Distribution by Provider

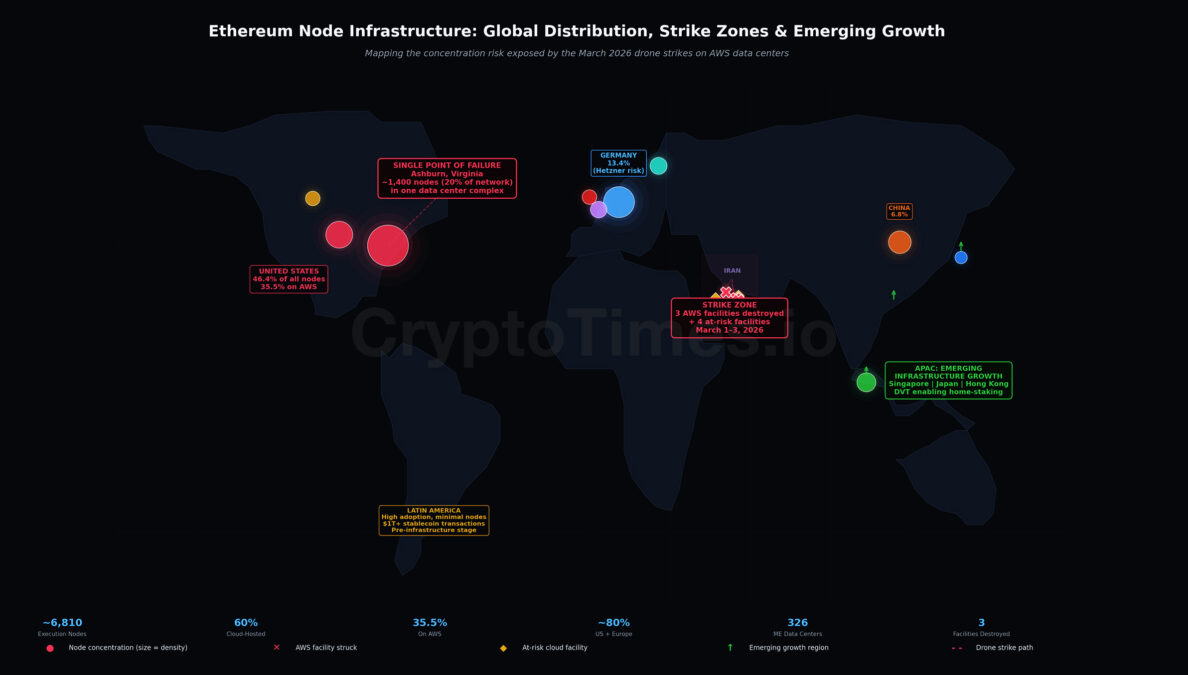

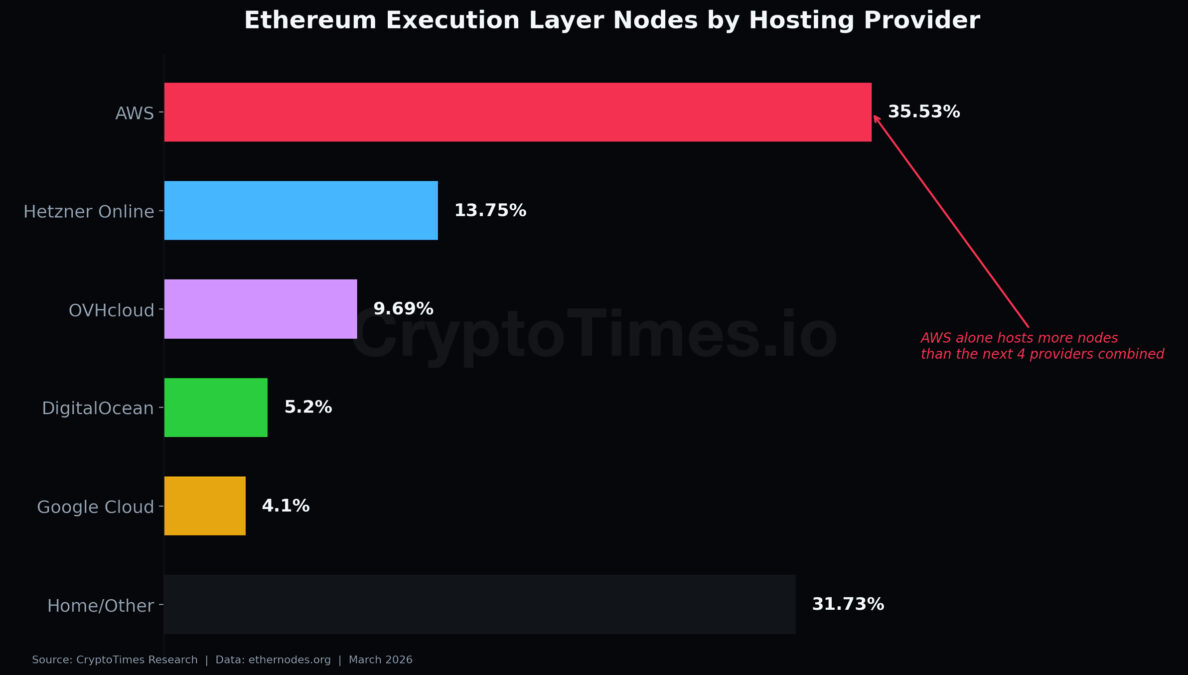

Of Ethereum’s approximately 6,810 execution layer nodes, roughly 60% are hosted on commercial cloud services. AWS alone accounts for 35.53% of all hosted nodes — approximately 2,439 nodes — making it the single largest infrastructure provider underpinning the Ethereum network. Hetzner Online follows at 13.75%, with OVHcloud at 9.69%.

Perhaps more troubling than the provider-level concentration is the geographic clustering: an estimated 1,395 AWS-hosted Ethereum nodes are concentrated in a single data center complex in Ashburn, Virginia. This means roughly 20% of Ethereum’s entire execution layer runs within one physical location.

Geographic Concentration

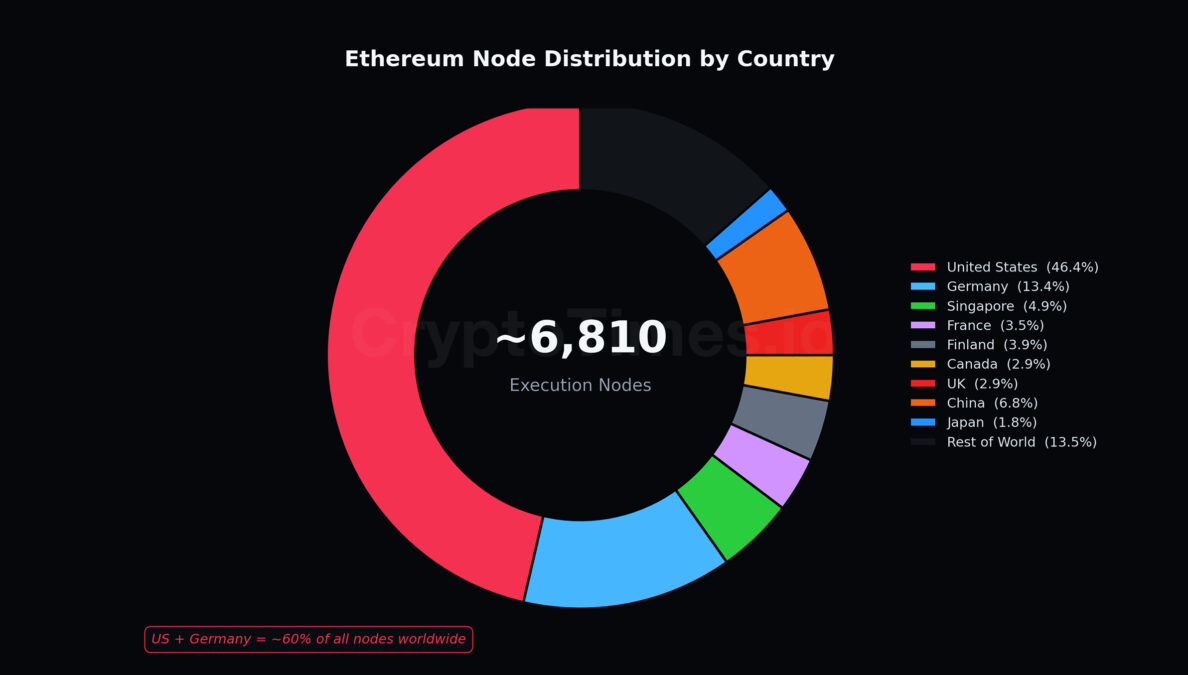

The United States hosts 46.4% of all distributed Ethereum nodes, followed by Germany at 13.4%. Together, these two countries account for nearly 60% of Ethereum’s global node infrastructure.

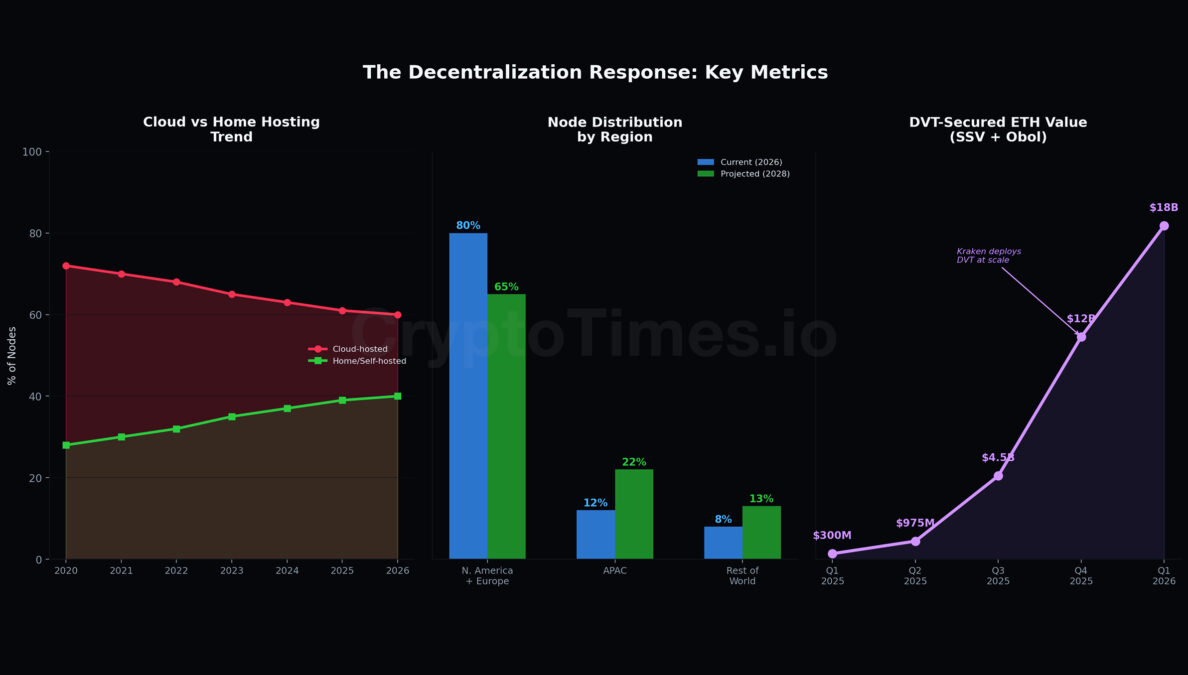

While the network’s overall cloud dependency has improved from over 70% in 2020 to approximately 60% today as more operators move to home-based setups, AWS’s share within the hosted segment has actually grown more dominant over time.

Impact Analysis: What Actually Broke

An important nuance in assessing the damage is that the drone strikes hit AWS’s Middle East regions (ME-CENTRAL-1 in UAE and ME-SOUTH-1 in Bahrain), which are not where most Ethereum nodes operate. The bulk of ETH nodes on AWS sit in US-EAST-1 (Ashburn, Virginia) and European regions. The direct impact on Ethereum’s node count was therefore limited.

However, the precedent and the cascading ripple effects are what make this event significant for the industry.

The Access Layer Collapsed — Not the Consensus Layer

This pattern was already demonstrated during the October 2025 AWS outage in US-EAST-1: Ethereum maintained 100% uptime at the consensus layer, producing blocks without missing a single slot. The blockchain itself kept running. But the infrastructure through which humans interact with Ethereum — wallets, RPC endpoints, front-end applications — collapsed.

Infura, the dominant RPC provider powering MetaMask and thousands of dApps, reported disruptions affecting Ethereum Mainnet, Polygon, Optimism, Arbitrum, Linea, Base, and Scroll during the October 2025 incident. MetaMask users saw wallet balances display as zero. Infura’s co-founder has acknowledged that 70–80% of RPC traffic still flows through a handful of centralized providers — creating a chokepoint that no amount of consensus-layer decentralization can mitigate.

Layer 2 Networks: The Weakest Link

Ethereum’s Layer 2 ecosystem proved even more vulnerable. Base, Coinbase’s L2 network, reported that AWS infrastructure disruptions reduced its operational capacity. This is not surprising: most L2 sequencers, data availability layers, and bridging infrastructure are hosted on the same cloud providers as the base layer — often with less redundancy.

The implication is stark. While Ethereum’s base layer has achieved meaningful decentralization at the consensus level, the application layer that users actually interact with daily remains critically dependent on a small number of cloud providers and RPC services.

Staker Exposure

Validators running on AWS-hosted infrastructure face a tangible financial risk: extended outages can trigger inactivity penalties and, in extreme cases, slashing. During prolonged cloud disruptions, stakers could face losses in the thousands to millions of dollars, depending on the duration and the number of validators affected.

Vulnerability Framework: Four Tiers of Risk

To properly assess Ethereum’s exposure to cloud infrastructure disruption — whether from military conflict, cyberattack, or regulatory action — it is useful to evaluate risk across four distinct layers of the network stack.

| TIER | LAYER | RISK | ASSESSMENT |

|---|---|---|---|

| Tier 1 | Consensus Layer | LOW | 1.06M validators staking 34M ETH with 99.78% participation. Distributed enough to withstand major regional outages without halting block production. |

| Tier 2 | Execution Nodes (AWS) | MEDIUM | ~1,400 nodes in Ashburn, VA represent the single biggest physical vulnerability. A targeted disruption there would be far more damaging than Middle East strikes. |

| Tier 3 | RPC / Access Layer | HIGH | 70–80% of RPC traffic flows through a handful of centralized providers. When these go down, users cannot transact even though the blockchain is running. |

| Tier 4 | DeFi & L2 Infrastructure | VERY HIGH | L2s like Base, Optimism, and Arbitrum plus major dApps on AWS are the most exposed. They have gone down in every major AWS outage to date. |

The Ongoing Threat: Data Centers in a War Zone

Image: Middle East Cloud Corridor

The forward-looking concern extends well beyond AWS. The Middle East cloud corridor — a region where AWS, Microsoft Azure, Google Cloud, and Oracle all operate significant infrastructure — has effectively become an active theater of war. There are roughly 326 data centers across the Middle East, with the largest concentrations in Israel, Saudi Arabia, and the UAE.

Facilities Still at Risk

Microsoft Azure operates its UAE North region out of Dubai, backed by a $15 billion investment commitment through 2029. Google Cloud maintains operations across the UAE and surrounding regions. Oracle runs infrastructure in Dubai. Local operators including Khazna Data Centers, Gulf Data Hub in the UAE, and Center3 in Saudi Arabia all sit within the same risk corridor.

AWS itself has warned customers that the broader operating environment in the Middle East remains unpredictable, recommending that organizations back up data and consider migrating workloads to alternate regions.

CSIS Warning: Data Centers as Strategic Targets

The Center for Strategic and International Studies warned last week that the nature of strategic targeting is evolving. In previous conflicts, adversaries focused on pipelines and refineries. In the compute era, data centers, the energy infrastructure supporting them, and fiber chokepoints are emerging as high-value targets. The March 2026 strikes validated this assessment in real time.

The Decentralization Response: Early Signals from APAC and Latin America

While the immediate aftermath of the strikes has focused on damage assessment and market reaction, a quieter but potentially more consequential shift is underway in Asia-Pacific and Latin America. These regions — historically underrepresented in Ethereum’s node infrastructure — are showing early signs of accelerated diversification that could reshape the network’s geographic risk profile.

The Geographic Gap: Where Nodes Don’t Run

The structural imbalance is stark. North America and Europe together account for approximately 80% of Ethereum’s Beacon Chain nodes. Singapore, despite being a major crypto hub, hosts only around 4.9% of the network’s nodes. Japan, South Korea, India, and the entirety of Latin America collectively represent a fraction of the remaining share. Validator nodes now span across 80 countries, but the density remains overwhelmingly concentrated in Western jurisdictions and their associated cloud regions.

This concentration creates a compounding vulnerability. Not only are the nodes physically clustered in the US and Europe, but they overwhelmingly rely on the same Western cloud providers — AWS, Hetzner, OVH — whose regional availability zones share correlated failure modes. A regulatory action in the US, a policy shift at Hetzner in Germany, or a physical disruption at Ashburn, Virginia would disproportionately impact the entire network.

APAC: Institutional Infrastructure Meets Grassroots Adoption

Asia-Pacific is uniquely positioned to absorb some of this concentration risk, driven by a convergence of regulatory clarity, institutional capital, and grassroots crypto adoption. Singapore, Hong Kong, and Japan have all established clear regulatory frameworks for digital assets. India ranks first on the Chainalysis Global Adoption Index, with Vietnam third and the Philippines fifth. The region received an estimated $2.36 trillion in on-chain value in 2025, up 69% year-over-year.

The infrastructure investment is following the adoption. A December 2025 survey of 500 Asian family offices found that 72% planned to increase their crypto allocations by Q1 2026, with 41% prioritizing Ethereum and Bitcoin for long-term holding. This institutional confidence is translating into infrastructure buildout: Singapore hosts TOKEN2049, the region’s largest crypto event drawing 25,000 attendees, while Hong Kong’s Consensus conference has become Asia’s premier Web3 policy forum. Japan’s ETHTokyo 2026 conference in September signals a maturing Ethereum-specific developer ecosystem in the region.

The critical question is whether this capital and community momentum will translate into node infrastructure. Early indicators are promising. Simon Kim, CEO of Hashed, one of Asia’s leading blockchain investors, has described 2026 as a “decisive shift” from retail speculation to institutional-grade infrastructure across the region. If even a fraction of APAC’s institutional staking inflows are directed toward locally hosted nodes rather than AWS regions in Virginia, the impact on Ethereum’s geographic distribution could be meaningful.

Latin America and Emerging Markets: The Long Tail

Latin America and emerging markets in Africa and Southeast Asia present a different but complementary picture. These regions have some of the world’s highest unbanked populations — 38% in South and Central America, 50% in Sub-Saharan Africa — and have demonstrated strong grassroots crypto adoption for remittances and payments, with over $1 trillion in stablecoin transactions recorded across emerging markets in 2025.

However, translating this adoption into node infrastructure faces structural barriers: unreliable power and internet connectivity, high hardware costs relative to local incomes, and limited technical knowledge for validator operation. The existing digital divide means that while these regions are major users of Ethereum’s application layer, they remain almost entirely absent from its infrastructure layer.

This is where emerging technologies could change the equation. Ethereum’s 2026 roadmap includes EIP-8025, which introduces zero-knowledge proof-based block verification. By dramatically reducing the computational requirements for validation, this upgrade could make running a full validator feasible on consumer-grade hardware — laptops and modest home servers — rather than the dedicated infrastructure currently required. If successfully implemented, EIP-8025 could lower the hardware barrier enough to enable meaningful node growth in regions that have been priced out of participation.

DVT: The Technology Bridge

Perhaps the most significant enabler of geographic diversification is Distributed Validator Technology (DVT). DVT allows a single validator’s cryptographic key to be split across multiple independent nodes, which collectively sign messages without any single operator holding the full key. This eliminates single points of failure and enables a validator to span multiple geographic locations.

The adoption numbers are already notable. As of May 2025, validators using Obol Network’s DVT solution were collectively securing more than $975 million in staked ETH. Kraken became the first major exchange to deploy DVT at scale for its Ethereum staking service, using SSV Network, which claims to secure over $18 billion across 126,000 validators. In January 2026, Vitalik Buterin proposed embedding DVT directly into Ethereum’s consensus protocol — a move that would make multi-node, multi-geography validator operation a first-class feature of the network itself.

For APAC and emerging market participants, DVT is transformative. A home staker in Singapore or São Paulo can distribute their validator across a local home node, a cloud instance in a different region, and a friend’s machine in another country — achieving genuine geographic redundancy at minimal cost. This turns infrastructure diversification from a large-scale enterprise concern into something achievable by individuals.

Regional Signals at a Glance

| REGION | KEY SIGNAL | STATUS |

|---|---|---|

| Singapore | Clear regulatory framework; TOKEN2049 draws 25K attendees; ~4.9% of ETH nodes | Growing |

| Japan | PM-level crypto engagement; ETHTokyo 2026; active Ethereum dev community | Growing |

| Hong Kong | Consensus HK premier Web3 policy forum; institutional staking inflows rising | Accelerating |

| India | #1 Chainalysis adoption index; strong developer base; node infra still nascent | Early Stage |

| S. Korea | Korea Blockchain Week; strong retail trading; institutional infra developing | Early Stage |

| Latin America | $1T+ stablecoin transactions; high adoption but minimal node presence | Pre-Infra |

| SE Asia | Vietnam #3 adoption; Philippines #5; DVT could enable home-staking at scale | Pre-Infra |

The Hetzner Variable

Adding a policy-based dimension to the physical risk: Hetzner Online, which hosts approximately 16% of Ethereum’s validator nodes, has maintained terms of service that explicitly prohibit all cryptocurrency-related applications, including staking and node operation. The Germany-based provider has been “internally discussing how to address this issue” since 2022.

Should Hetzner choose to enforce these terms, Ethereum could face a simultaneous physical and policy-driven disruption to its node infrastructure — a compound risk that underscores the urgency of diversifying hosting arrangements across the validator set.

Market Reaction

The crypto market’s response to the strikes followed a familiar pattern of initial panic followed by rapid recovery. When the first reports of the attacks emerged on February 28, the total crypto market capitalization shed $128 billion within minutes. Bitcoin dropped sharply, while Ethereum and altcoins fell in tandem.

By Monday, however, sentiment had reversed. Bitcoin surged from approximately $65,500 to over $69,000, with Ethereum gaining roughly 6%. Traders appeared to interpret the conflict as short-lived and isolated in scope, with digital assets reassuming their narrative as alternative stores of value during geopolitical instability; as of today, Bitcoin is trading at approximately $67,898.

The disconnect between the market’s rapid recovery and the underlying infrastructure vulnerabilities exposed by the strikes is notable. Prices bounced, but the systemic risks remain unresolved.

What This Means for Ethereum

The March 2026 drone strikes did not break Ethereum. The consensus layer held. Blocks were produced. The protocol proved its resilience at the most fundamental level.

But the attacks accomplished something arguably more important: they proved that the infrastructure surrounding Ethereum — the cloud servers, the RPC providers, the wallet backends, the L2 sequencers — can be physically destroyed in wartime. The October 2025 AWS outage already demonstrated that the access layer breaks when cloud providers go down. Now we have confirmation that cloud providers can be taken offline by military force.

The implications are clear. Ethereum’s decentralization must extend beyond the consensus layer to encompass the full stack: execution nodes, RPC services, L2 infrastructure, and the cloud providers that host them all. The early signals from APAC and emerging markets — coupled with DVT’s maturation and EIP-8025’s promise of lighter validation — suggest the tools for geographic diversification are arriving. The question is whether the industry will deploy them with the same urgency it brings to protocol upgrades.

With Microsoft, Google, Oracle, and AWS all operating in the same geographic corridor that is now an active conflict zone, the risk is no longer theoretical. The question is no longer whether cloud infrastructure will be targeted again — but when, and whether Ethereum’s node map will look any different when it happens.