Not long ago, a debit card meant one thing: spending fiat money from your bank account. In 2026, it could also mean spending Bitcoin, Ethereum, or USDC at checkout, with crypto converting to fiat in real time.

Crypto debit cards have matured rapidly. Cards from Bleap, Crypto.com, Binance, and Coinbase are now accepted at millions of merchants worldwide through Visa and Mastercard networks. They look identical to a traditional debit card, but the fees, rewards, tax implications, and consumer protections are very different.

This article breaks down every important fee category side by side, using the latest 2026 data, so you can decide which card belongs in your wallet.

What Is a Crypto Debit Card?

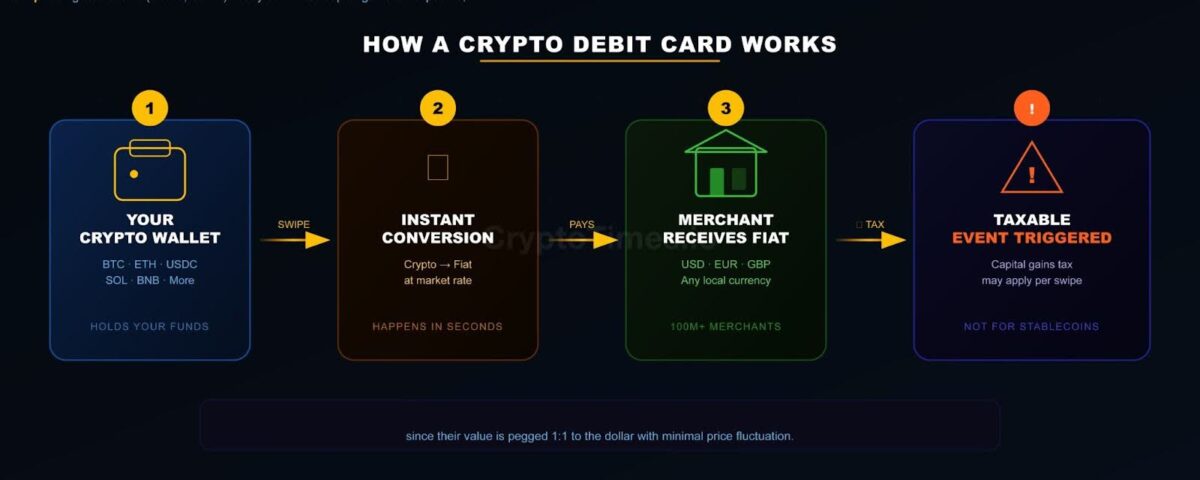

A crypto debit card works like a regular debit card, except it is connected to your cryptocurrency wallet or exchange account instead of a bank.

When you swipe, the card instantly converts your crypto into the local fiat currency. The merchant receives payment in their local currency. You do not have to manually sell your crypto beforehand.

Most crypto cards run on the Visa or Mastercard networks, giving them access to 90–100 million merchants worldwide.

There are three main types:

- Prepaid crypto cards are topped up with crypto in advance and converted to fiat for spending.

- Crypto debit cards pull directly from your exchange wallet or connected crypto balance in real time.

- Hybrid credit/debit cards (like the Nexo Card) let you borrow against your crypto as collateral so you don’t have to sell your holdings to spend.

Monthly & Annual Fees: Crypto Cards Win Easily

This is where crypto cards have the clearest advantage.

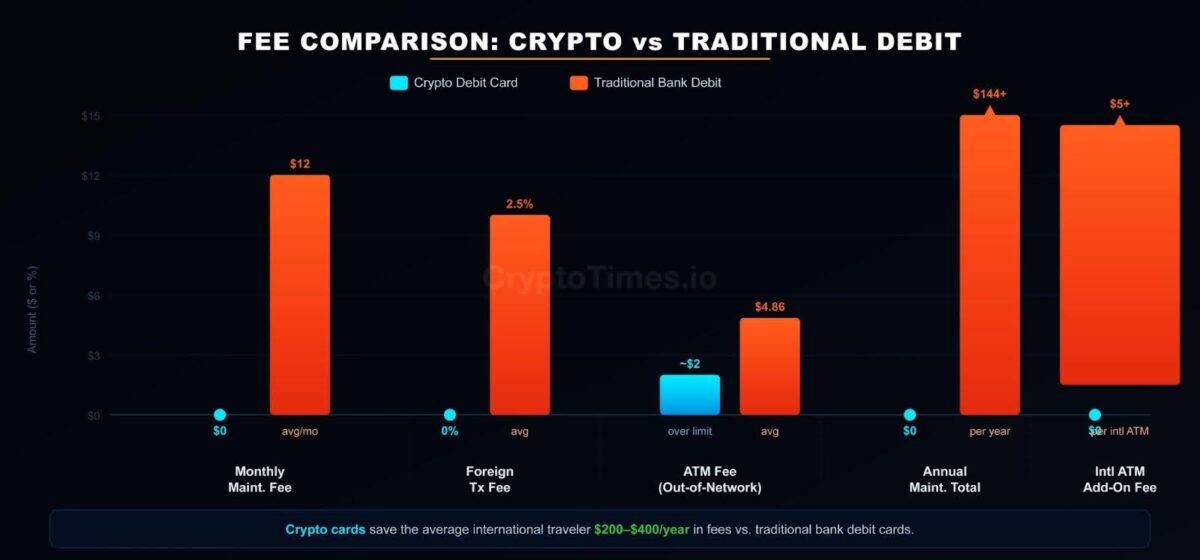

Most traditional bank checking accounts charge monthly maintenance fees ranging from $5 to $15 per month. These fees are often waivable if you maintain a minimum balance, but many people still pay them.

Crypto debit cards almost universally charge $0 in monthly or annual fees. The Nexo Card, Coinbase Card, Binance Visa, Crypto.com Visa, and Bleap Mastercard all carry no monthly, annual, or inactivity fees in standard debit mode.

| Fee Type | Traditional Bank Debit | Crypto Debit Card |

|---|---|---|

| Monthly maintenance | $5–$15 (waivable) | $0 |

| Annual fee | $0–$36 | $0 |

| Card issuance | $0 | $0–$5 (by region) |

| Inactivity fee | $0–$10/month | $0 |

Over a full year, a traditional bank account can cost you $60–$180 in maintenance fees alone, money that a crypto card user does not pay.

Foreign Transaction Fees: A Major Win for Crypto Cards

If you travel internationally or shop from foreign websites, foreign transaction fees are among the most frustrating costs of traditional banking.

Most traditional banks charge 1% to 3% on every foreign purchase or overseas ATM withdrawal. For example, U.S. Bank charges a 3% foreign transaction fee on all overseas transactions. On a $2,000 vacation spending budget, that is $60 in fees alone.

Top crypto debit cards in 2026 charge 0% in foreign transaction fees. The Bleap Mastercard, Crypto.com Visa, Binance Visa, and WhiteBIT Card all offer zero FX fees, making them strong options for international travelers.

| Card | Foreign Transaction Fee |

|---|---|

| Traditional bank (average) | 1–3% |

| U.S. Bank debit | 3% |

| Bleap Mastercard | 0% |

| Crypto.com Visa | 0% |

| Binance Visa | 0% |

| WhiteBIT Card | 0% (0.1% on bank transfers only) |

| Coinbase Visa | 0% domestic; standard Visa FX applies abroad |

Some fee-free traditional banking options do exist. Capital One 360 and Charles Schwab charge no foreign transaction fees on debit, but these are exceptions. Most mainstream banks still charge them.

ATM Fees: A More Complex Picture

ATM fees are where traditional bank users often feel the most pain, especially out of network.

According to Bankrate’s 2025 Checking Account and ATM Fee Study, the average out-of-network ATM fee is $4.86 per transaction, combining the bank’s own fee ($1.64 on average) and the ATM operator’s surcharge ($3.22 on average). If you withdraw cash once a week from an out-of-network ATM, that adds up to over $250 per year in ATM fees.

International ATM withdrawals add another layer of charges, typically 1%–3% on top of a flat fee of up to $5.

Crypto cards handle ATM fees differently. Most offer a free monthly allowance before charging:

| Card | Free ATM Allowance | Fee After Limit |

|---|---|---|

| Traditional bank (in-network) | Unlimited | $0 |

| Traditional bank (out-of-network) | $0 free | $4.86 avg per transaction |

| Bleap Mastercard | $400/month worldwide | Standard ATM charges |

| Crypto.com Visa (Ruby) | $1,000/month (EEA) | Varies by tier |

| WhiteBIT Card | €1,000/day (EEA) | €2 + 2% outside EEA |

| Coinbase Visa (US) | No Coinbase ATM fee | Operator fees may apply |

| Bybit Card | Limited free tier | Low fee after |

For light cash users, crypto cards’ free ATM allowances cover most needs. Heavy cash users should pay close attention to monthly limits.

Crypto-Specific Fees: Hidden Costs to Watch

Crypto cards eliminate many traditional banking fees, but they introduce their own costs. These are often buried in the fine print.

Spread markups occur when the card provider converts your crypto to fiat at a slightly worse rate than the market price. This is typically 0.5% to 1.5% and is less visible than an explicit fee.

Blockchain gas fees apply when you top up your card from an on-chain wallet. Ethereum gas fees can range from $0.50 to $5 or more, depending on network congestion.

Staking costs are an implicit fee. Some cards (like Crypto.com Visa) require you to lock up large amounts of their native token to unlock higher cashback tiers. Tying up $400 to $400,000 in CRO has an opportunity cost.

| Hidden Fee Type | Range | Who Charges It |

|---|---|---|

| Spread markup | 0.5%–1.5% | Most platforms |

| Blockchain gas fees | $0.50–$5+ | Ethereum-based top-ups |

| Staking lock-up cost | Varies | Crypto.com, Binance (for top cashback) |

Cashback Rewards: Crypto Cards Pull Ahead

Traditional debit cards rarely offer cashback. Most offer none. Some premium accounts offer 1% back through linked programs, but these are the exception.

Crypto debit cards make cashback a central selling point. However, there is an important gap between advertised maximum rates and what typical users actually earn.

The Bleap Mastercard advertises up to 20% cashback in USDC with no staking requirement, making it one of the most accessible reward programs. Its flat 2% base rate is reliable for everyday spending.

The Oobit Crypto card offers up to 10% cashback in OOB with no staking requirement, making it one of the most rewarding programs available. Its flat 1% transaction fee keeps costs predictable for everyday spending. Users who prefer stablecoins can earn 5% cashback in USDT — a strong option for those who want rewards without token exposure.

The Crypto.com Ruby Card offers 2% cashback, but this requires staking CRO tokens. Without staking, the effective rate is much lower, and monthly rewards are capped at $25. The Obsidian card offers up to 5% cashback and now has a monthly rewards cap.

The Binance Visa advertises up to 8% cashback, but accessing the top tier requires holding 600 BNB tokens, worth hundreds of thousands of dollars at current prices.

The Coinbase Visa offers up to 4% crypto cashback with no staking requirement, though the crypto-to-fiat conversion fee reduces the net benefit.

The Gemini Credit Card earns up to 4% back on gas and transit, with no annual fee and no foreign transaction fees.

| Card | Realistic Rate | Max Advertised | Paid In | Staking Required? |

|---|---|---|---|---|

| Traditional bank debit | 0% | 0% | N/A | No |

| Bleap Mastercard | 2% | 20% | USDC | No |

| Oobit Crypto Card | 5% | 10% | USDT / OOB | No |

| Crypto.com Visa | 1–3.5% | 5% | CRO | Yes (up to $400K CRO) |

| Coinbase Visa | 1.5–2% | 4% | Crypto of choice | No |

| Binance Visa | 0.1–1% typical | 8% | BNB | Yes (600 BNB) |

| WhiteBIT Card | 1–2% typical | 10% | BTC or WBT | No |

| Gemini Credit Card | 1.5–2% average | 4% | 50+ cryptos | No |

| Bybit Card | 2–4% effective | 10% | Varies | No |

The key takeaway: ignore the headline maximums. Focus on the staking requirements and the realistic rate for your spending level.

The Hidden Cost Nobody Talks About: Tax Implications

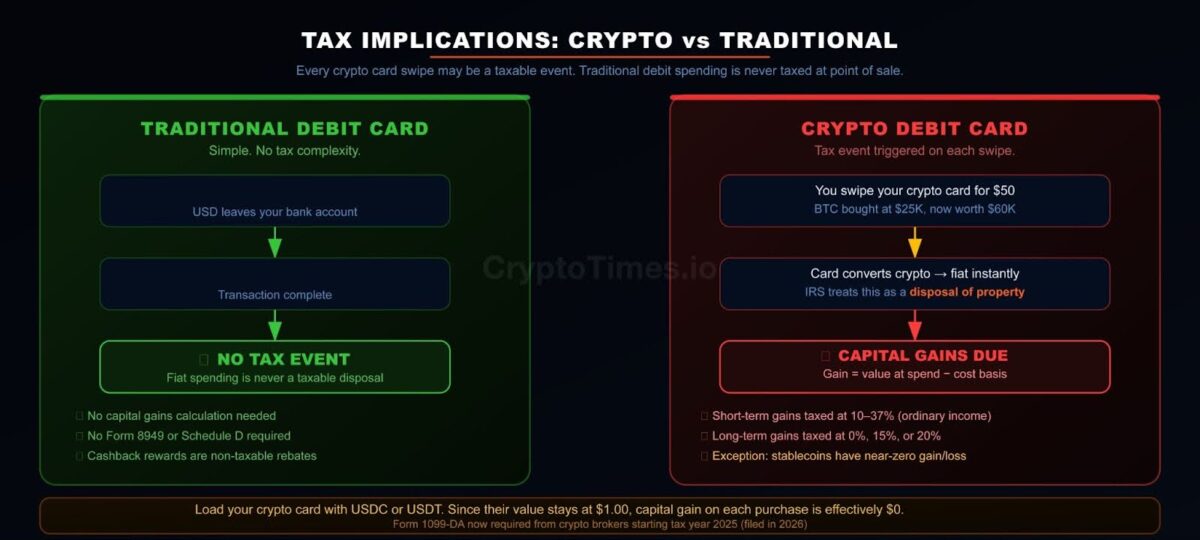

This is the single most important difference between crypto and traditional debit cards, and it is often underexplained.

Spending money from a bank account is not a taxable event. There are no capital gains, no forms to file, and no tracking required.

Spending crypto with a debit card almost always is a taxable event. The IRS treats cryptocurrency as property. Every time you swipe your crypto debit card, you are technically disposing of a capital asset. If the value of your crypto has increased since you acquired it, you may owe capital gains tax on that gain, even if you only spent $5 on a coffee.

For example, if you bought Bitcoin at $25,000 and it is worth $60,000 when you buy groceries worth $60, you have realized a capital gain on the fraction of Bitcoin sold. That gain must be reported on Form 8949 and Schedule D.

Short-term capital gains on crypto held less than one year are taxed at ordinary income rates of 10–37%. Long-term gains on crypto held more than one year are taxed at the lower 0%, 15%, or 20% rates, depending on your income.

A major 2026 regulatory development: starting with transactions on or after January 1, 2025, cryptocurrency brokers are required to report gross proceeds to the IRS using the new Form 1099-DA. The IRS is tightening enforcement, and crypto card transactions are now clearly within scope.

| Tax Factor | Traditional Debit Card | Crypto Debit Card |

|---|---|---|

| Is each purchase a taxable event? | No | Yes (if crypto appreciated) |

| Capital gains owed? | Never | Potentially, on every swipe |

| Short-term rate | N/A | Ordinary income (10–37%) |

| Long-term rate | N/A | 0%, 15%, or 20% |

| IRS reporting required? | No | Yes — Form 8949 + Schedule D |

| New reporting form (2026) | N/A | Form 1099-DA from brokers |

| Tax software recommended? | No | Strongly yes (Koinly, CoinLedger) |

The stablecoin workaround: Loading your crypto card with stablecoins (USDC, USDT) nearly eliminates this problem. Since stablecoins maintain a 1:1 peg with the dollar, any capital gain or loss on a transaction is close to zero. They are still technically taxable disposals under IRS rules, but the gain is typically negligible in most cases.

Security & Consumer Protections

This is one area where traditional bank debit cards maintain a clear advantage.

Traditional bank accounts are FDIC-insured up to $250,000 per depositor. If your bank fails, your money is protected. Under Regulation E, banks are also required to investigate unauthorized transactions and provide zero-liability protection for fraud.

Crypto card accounts are not FDIC-insured. If the platform becomes insolvent or is hacked, your funds may be at risk. Chargeback rights are limited and vary significantly by issuer.

Non-custodial crypto cards (Bleap, Gnosis Pay, and EtherFi) partially address this by keeping funds in user-controlled wallets until the moment of spending, reducing platform risk, though not eliminating market volatility risk.

| Protection | Traditional Bank Debit | Crypto Debit Card |

|---|---|---|

| FDIC/NCUA insured | Yes (up to $250K) | No |

| Fraud protection | Regulation E (strong) | Varies by issuer |

| Chargeback rights | Strong | Limited |

| Platform insolvency risk | Very low | Moderate |

| Card freeze via app | Yes | Yes (most apps) |

Who Should Use Which Card?

Choose a traditional debit card if you:

- Want FDIC-insured protection on your funds

- Don’t want to deal with capital gains taxes on daily purchases

- Need overdraft protection, in-branch services, or wire transfers

- Have a fee-free account (Chime, Capital One 360, Charles Schwab) that already waives FX and ATM fees

Choose a crypto debit card if you:

- Already hold crypto and want to spend it without manual conversions

- Travel internationally and want 0% foreign transaction fees

- Want to earn cashback paid in Bitcoin, USDC, or stablecoins

- Are comfortable using stablecoins for daily spending to minimize tax complexity

- Are a DeFi user who wants self-custody while spending (Gnosis Pay, Bleap, EtherFi Cash)

Best Crypto Cards by Use Case (2026)

| Use Case | Best Card | Why |

|---|---|---|

| Best overall | Bleap Mastercard | 0 fees, 2% USDC cashback, non-custodial |

| Best for stakers | Crypto.com Visa | Up to 5% cashback for CRO stakers |

| Best for US users | Coinbase Visa | Seamless integration, up to 2% cashback |

| Best for travelers | Bleap / Binance Visa | 0% FX fees, global acceptance |

| Best for DeFi users | Gnosis Pay / EtherFi | True self-custody, wallet-connected |

| Best for daily spending | Oobit Crypto Card | Low fees, 5% USDT / 10% OOB cashback, non-custodial |

| Best hybrid card | Nexo Card | Borrow against crypto, earn 14% interest in debit mode |

| Best no-fee traditional | Charles Schwab / Chime | No FX fee, ATM reimbursements |

Key Takeaways

Crypto debit cards win on fees in almost every category. Zero monthly costs, zero foreign transaction fees, and ATM allowances that outperform most bank offerings make them cost-efficient for everyday use, especially for travelers.

But crypto cards come with trade-offs that matter. Tax reporting on every non-stablecoin transaction adds real complexity and cost at tax time. The lack of FDIC insurance is a genuine risk. And headline cashback rates are often inflated by staking requirements that most users won’t meet.

For many people in 2026, the most practical strategy is to use a crypto card funded with stablecoins for everyday spending (earning rewards with near-zero tax complexity), and keep a traditional account for emergency funds, insured savings, and overdraft protection.

Neither card is universally better. The right choice depends on whether you already hold crypto, how much you travel, and how comfortable you are with tax recordkeeping.

Frequently Asked Questions

Are crypto debit cards safe to use?

Most reputable crypto cards (Coinbase, Crypto.com, Binance) are issued through licensed partners on the Visa or Mastercard network, giving them the same transaction security as any other card. The main risk is platform insolvency. Unlike bank accounts, crypto card balances are not FDIC-insured.

Do crypto debit cards charge foreign transaction fees?

Most top crypto cards in 2026 charge zero foreign transaction fees. Bleap Mastercard, Crypto.com Visa, Binance Visa, and WhiteBIT Card all offer 0% FX fees, which is a major advantage over traditional banks that often charge 1–3%.

Is spending crypto on a debit card taxable?

Yes, in most jurisdictions, including the United States. The IRS treats crypto as property, so each transaction is a taxable disposal. Using stablecoins like USDC instead of Bitcoin or Ethereum nearly eliminates capital gains exposure on routine purchases.

Which crypto card has the best cashback?

For no-conditions cashback, Bleap Mastercard offers a reliable 2% in USDC with no staking required (maximum advertised 20%). For stakers, Crypto.com Visa offers up to 5%. Gemini Credit Card offers up to 4% on gas and transit with no annual fee.

Can I use a crypto debit card at any ATM?

Yes. Most crypto cards support ATM withdrawals at any ATM on the Visa or Mastercard network worldwide. The Bleap Mastercard offers free withdrawals up to $400/month globally. Above that limit, standard ATM operator fees apply.