In the fast-paced crypto ecosystem, protocols continue to test new ways to align user activity with token value through supply management strategies. Hyperliquid’s similar approach has drawn attention for its aggressive use of trading revenue to repurchase its native token, achieving notable reductions in available supply within a relatively short period compared with longer-established networks like Ethereum.

The difference stems from how each protocol captures and deploys revenue. Hyperliquid routes the vast majority of its fees directly into open-market purchases of its native token. Ethereum burns a portion of base fees as a byproduct of network usage.

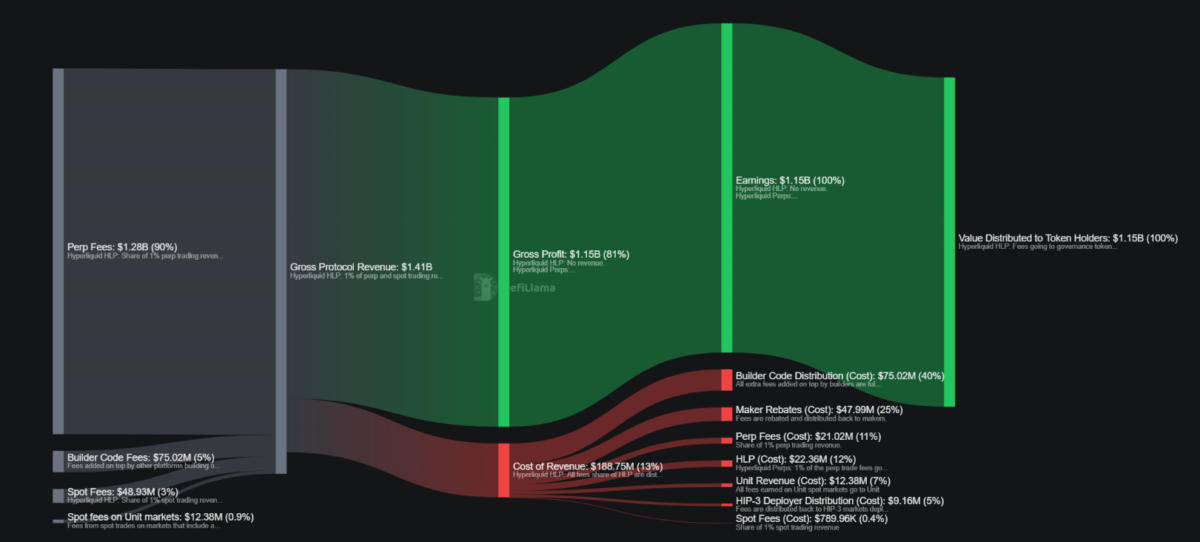

Data from DeFiLlama show Hyperliquid’s mechanism has generated over $1.15 billion in cumulative revenue, with nearly all of it directed toward HYPE acquisitions.

Hyperliquid’s Assistance Fund and Buyback Mechanics

Hyperliquid operates a decentralized perpetual futures exchange on its own custom Layer 1 blockchain. The platform uses a central limit order book model and achieves high throughput through its HyperBFT consensus. Trading fees on perpetuals and spot markets—typically in the range of a few basis points—flow overwhelmingly into the Assistance Fund.

According to protocol design and DefiLlama accounting, 99% of these fees go to the fund. The fund then executes automated daily purchases of HYPE on the open market. These acquisitions remove tokens from active circulation.

The fund has accumulated approximately 45.7 million HYPE through this process, with recent daily buybacks in the range of $1.8 million to $2 million.

The mechanism functions like an automated, transparent share repurchase program scaled to trading activity. Unlike discretionary corporate buybacks, it runs continuously without requiring governance votes for each purchase. In late 2025, the community voted to formally recognize tokens held by the Assistance Fund as burned, solidifying the deflationary effect.

Circulating supply of HYPE currently sits just above 253 million tokens out of a 1 billion maximum. The buybacks have therefore removed a double-digit percentage of the float that has entered circulation. This has coincided with periods of strong price performance, including all-time highs above $76 earlier in 2026, though price remains influenced by unlock schedules and broader market conditions.

Daily protocol fees have recently hovered around $1.9 million to $2.4 million, translating into annualized buyback pressure in the hundreds of millions of dollars when volume sustains. The system scales directly with usage: higher trading activity means more fees and larger purchases.

Ethereum’s EIP-1559 Burn: A Different Scale

Ethereum introduced its fee-burning mechanism with the London hard fork on August 5, 2021. Under EIP-1559, a base fee—dynamically adjusted based on block fullness—is permanently destroyed with every transaction. Tips paid to validators remain separate.

Cumulative burns have reached approximately 5.35 million ETH as tracked by explorers such as beaconchain data. This figure reflects nearly five years of operation across a much larger and more mature network. Ethereum’s total supply stands near 120–122 million ETH, meaning the burns equate to roughly 4.4 percent of current supply.

The burn rate fluctuates with network demand. High-activity periods, such as NFT mints or DeFi surges, increase base fees and therefore burns. However, the mechanism does not involve active purchasing of ETH on the open market. It simply destroys a slice of fees that users would have paid anyway. Issuance from staking rewards continues, so net supply change depends on whether burns exceed new issuance on any given period.

What’s Powering Hyperliquid’s Revenue: Perps Volume and TradFi Crossover

Hyperliquid’s fee generation has been driven primarily by perpetual futures trading. The platform has captured a dominant share of on-chain perp volume, with 30-day figures exceeding $200 billion in recent periods and cumulative perp volume in the trillions.

A growing portion of this activity comes from non-crypto assets. Through its HIP-3 framework, Hyperliquid offers perpetuals on U.S. stocks, indices, commodities, and other traditional instruments. Reports indicate that equities and related products now occupy multiple spots among the platform’s highest-volume pairs. Significant trading occurs outside traditional market hours, including weekends, when Nasdaq and other exchanges are closed.

This 24/7 accessibility, combined with high leverage and USDC collateral, has drawn participants seeking exposure to assets like major tech stocks without the constraints of conventional brokerage hours or margin rules. Open interest in builder-deployed markets has reached billions of dollars, with notable activity in oil, Nasdaq-linked products, and individual equities.

The resulting trading volume generates the fees that feed the Assistance Fund. Unlike many decentralized exchanges that rely on liquidity provider incentives or token emissions, Hyperliquid’s model ties token value accrual directly to organic usage. The platform launched without traditional venture capital backing in the conventional sense and has scaled through product-market fit in derivatives trading.

The contrast with Ethereum highlights differing approaches to tokenomics. One protocol burns fees passively as a side effect of general usage. The other actively recycles nearly all trading revenue into its own token through market purchases. Both mechanisms aim to align incentives between users and token holders, yet they operate at different speeds and through different channels.

Hyperliquid’s approach has drawn attention for its intensity relative to the platform’s age. Whether the pace sustains will depend on continued trading volume, competition from other perpetuals venues, and the broader appetite for on-chain derivatives that bridge traditional assets with crypto rails. Data from analytics platforms will continue to provide the clearest measure of how these dynamics evolve.

Also read: Cristiano Ronaldo Targeted in Deepfake Crypto Scam Amid Portugal’s World Cup Exit