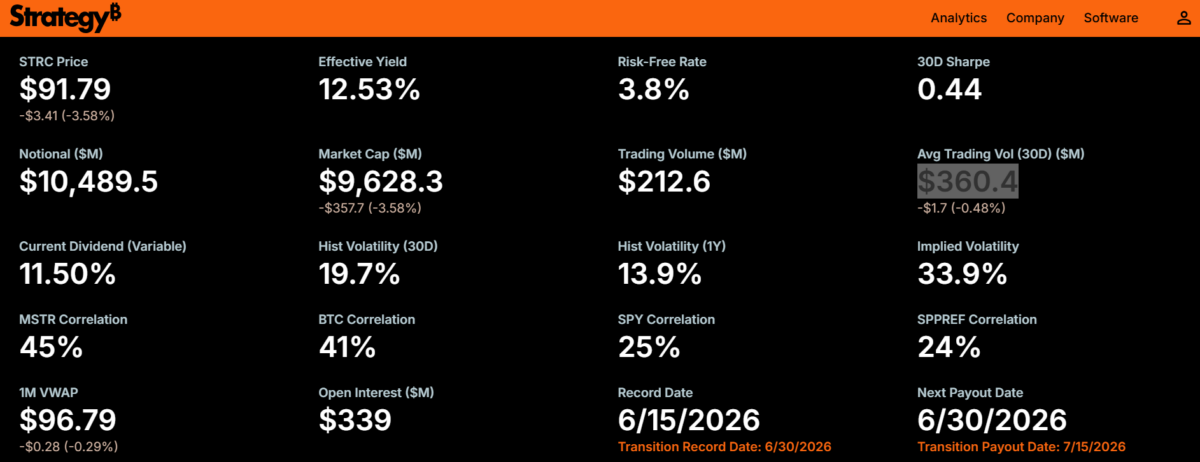

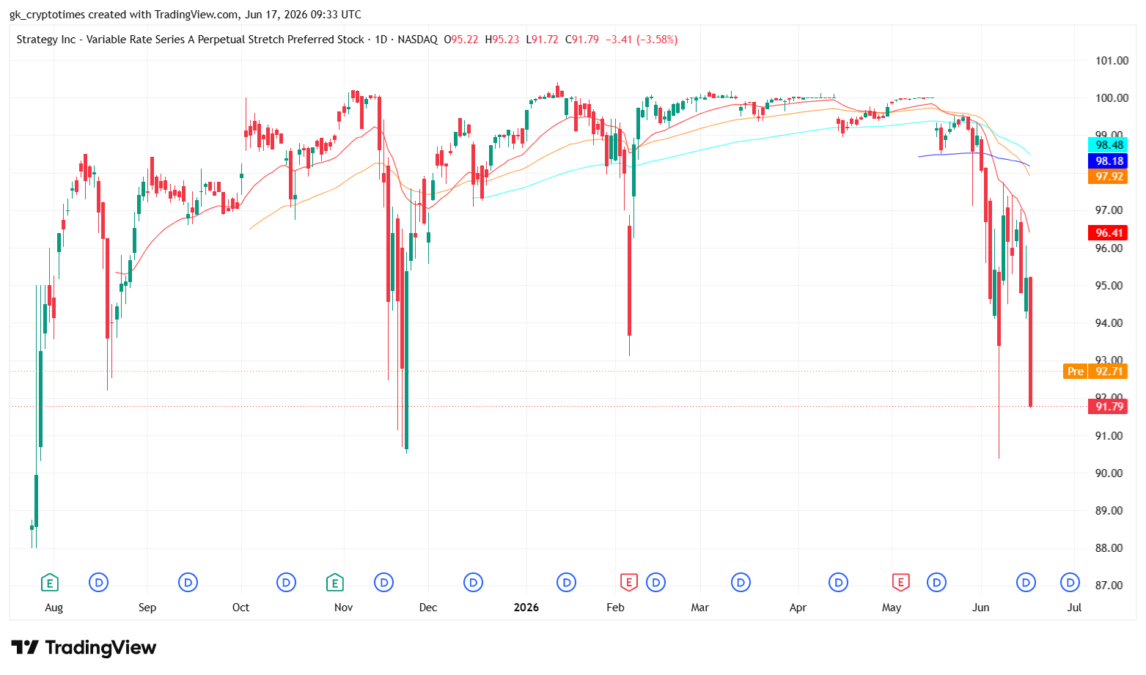

On June 16, 2026 close, Strategy Inc.’s Variable Rate Series A Perpetual Stretch Preferred Stock (STRC) finished at $91.79, down 3.58% on the day and approximately 8.2% below its $100 par value.

This downtrend in STRC price occurs even as Strategy’s official account highlights strong momentum, posting that “$STRC is scaling at a ~350% annualized growth rate.” The contrast underscores the gap between the company’s reported growth metrics in notional scale and the market’s current pricing of the security.

Designed as “short-duration high-yield credit,” STRC aims for low volatility near par through adjustable dividends, cash reserves, and issuance mechanics. Yet recent trading in the low $90s underscores the influence of shifting investor preferences, competitive pressures, and liquidity realities in the evolving digital credit space.

The nominal annualized dividend rate for STRC stands at 11.50%, paid semi-monthly in cash, delivering an effective yield of 12.53% for buyers at current levels. With notional outstanding exceeding $10.49 billion, the persistent discount has drawn attention to how broader market forces are challenging the product’s engineered stability.

Market Dynamics and Intense Yield Competition Drive Pricing Pressure

Investor rotation toward competing products has emerged as a central force behind STRC’s depeg. Rival offerings, such as Strive’s SATA, provide comparable or higher yields—around 13% annualized—with daily dividend payments and have maintained trading closer to par. This has pulled yield-seeking capital, particularly from retail and income-focused accounts, away from STRC.

Social sentiment and trading forums highlight perceptions of SATA as offering more frequent payouts and a cleaner structure, prompting some holders to exit STRC positions after capturing recent dividends. The result is softer demand for STRC at par levels, even as its effective yield climbs attractively above 12.5%.

Broader market dynamics amplify this. In environments where capital chases optimized income with minimal friction, features like payment frequency and perceived simplicity gain outsized influence.

Liquidity and technical factors further shape price action. STRC experiences predictable ex-dividend drops that can accelerate selling in thinner bid environments. Its average 30-day trading volume hovers around $360 million, with occasional spikes, but defensive support has formed in the low $90s amid hesitation to buy aggressively below target.

Quantitative and arbitrage flows may exacerbate moves once key levels break, creating self-reinforcing pressure unrelated to underlying fundamentals.

These dynamics test Strategy’s ability to maintain the tight $99–101 trading band. While the product launched successfully in 2025 and scaled rapidly, sustained trading away from par signals that market participants are weighing convenience, competition, and structural nuances more heavily than in earlier phases—even as the company emphasizes rapid notional growth.

Dividend Coverage and Reserve Management Raise Sustainability Questions

Strategy’s cash reserves, built to buffer dividend obligations, have declined notably following strategic moves such as the repurchase of $1.5 billion in convertible debt in late May. Its coverage now sits in the 6–7 month range against annual preferred obligations approaching $1.7 billion, down from more robust multi-year buffers earlier.

This reduction, while part of broader balance sheet optimization (reducing debt and interest exposure), has heightened investor focus on payout reliability. Preferred dividends are paid from reserves and operational/issuance proceeds rather than direct Bitcoin sales in normal conditions, but thinner cushions invite scrutiny about long-term cash flow management if new capital raises slow.

Management retains flexibility—adjusting issuance pace or rebuilding liquidity—but prolonged discounts limit efficient ATM activity, creating a feedback loop where lower prices constrain the very mechanisms meant to support stability.

The perpetual nature of STRC adds another layer. As equity-like preferred stock, STRC carries no maturity or mandatory redemption at par. Holders enjoy senior claims on residual assets but accept extension and market risk.

The company’s recent semi-monthly dividend transitions aim to enhance appeal through more frequent payments, yet the move has coincided with the current pressure period, underscoring how execution timing interacts with sentiment.

Analysts note that while dividends continue uninterrupted, the combination of reserve drawdowns and issuance economics in a selective capital market environment contributes to the discounted valuation. This reflects standard preferred stock behavior under stress rather than distress, but it tests investor tolerance for temporary deviations from the target price.

Variable Rate Mechanism Navigates Limits Amid Shifting Sentiment

The core “Stretch” self-correcting feature—monthly dividend adjustments in 25 basis point increments—has already lifted the rate from an initial 9% to the current 11.50%. Despite the discount persisting, the board has held steady recently, balancing higher cash costs against the risk of escalating obligations.

Market observers and analysts have offered nuanced perspectives on why the rate has not been raised further. One detailed analysis by Flying Raven on X suggests Strategy is deliberately testing whether structural improvements—specifically the shift to semi-monthly payments combined with rebuilding the USD reserve—can close the discount before resorting to a rate hike.

“The problem with STRC trading below par may not be the dividend rate itself,” the X post reads. “At 11.5% and a market price around $95, investors are already getting a very attractive current yield. The bigger issue may be confidence in the credit, liquidity, and balance sheet support behind the instrument.”

According to the analyst, by avoiding an automatic rate increase, the company aims to avoid training the market to expect mechanical hikes every time pressure appears, preserving flexibility and treating STRC more like a managed credit instrument.

Former bond trader and market commentator Josh Mandell echoed related themes in a video analysis, noting that the market price is sending a clear signal regarding upcoming dividend adjustments.

Mandell highlighted the importance of clear communication around the USD cash reserve strategy—particularly the decision to use reserves to retire convertible debt with the explicit intention of rebuilding them—as a way to demonstrate disciplined balance sheet management rather than reflexive support.

Another prominent recovery roadmap proposed by analyst Parker outlines concrete steps to address the situation. He said to raise the dividend to 12%, announcing a shareholder vote to move to daily dividends (making shorting more expensive), increasing the company’s call price from $101 to $110 or higher (raising risk for shorts), and rebuilding the cash buffer to $2.5 billion to reduce credit risk and counter FUD.

This restraint highlights practical limits as aggressive further hikes could pressure reserves more than they attract buyers if competition and broader yield alternatives remain compelling. The mechanism assumes sufficient demand elasticity, but in today’s fragmented high-yield landscape, price discovery incorporates multiple variables beyond rate alone—liquidity, payment cadence, issuer optics, and macro risk appetite.

Historical patterns show resilience. STRC has previously recovered from lows in the $88–$95 zone during favorable windows, supported by rebounds in demand and issuance. Current 30-day historical volatility stands at 19.7%, with correlations to Strategy’s broader ecosystem but distinct drivers rooted in preferred market mechanics.

However, total returns for holders, factoring reinvested dividends, have remained positive even during drawdown phases.

Management, including CEO Phong Le, has signaled confidence in available levers, including potential rate adjustments, reserve rebuilding, targeted messaging, or incentives to narrow the gap. The design anticipates periodic tests, positioning STRC as innovative yet exposed to real-world market forces—even while the company publicly emphasizes its scaling trajectory.

Outlook: Balancing Innovation with Market Realities

STRC’s current discount offers elevated effective yields for those comfortable with its Bitcoin-treasury linkage and preferred characteristics, without requiring direct crypto custody. It exemplifies the opportunities and frictions in digital credit products that convert asset appreciation potential into cash income.

Challenges center on execution in a competitive, sentiment-driven arena. Recovery paths likely involve restoring demand through demonstrated stability, optimized features, and capital market conditions that favor efficient issuance. Critics raise valid points about dilution risks and structural dependencies, while supporters highlight the product’s track record of adaptation and high cash distributions.

As Strategy expands its suite of instruments, the coming periods will clarify whether market dynamics allow the Stretch mechanism to re-anchor near par or if discounted trading becomes more entrenched—particularly as the company continues to spotlight its growth metrics amid the price pressure.

Also read: CFTC Approves Novig as Sports Prediction Market Boom Accelerates