Key Highlights

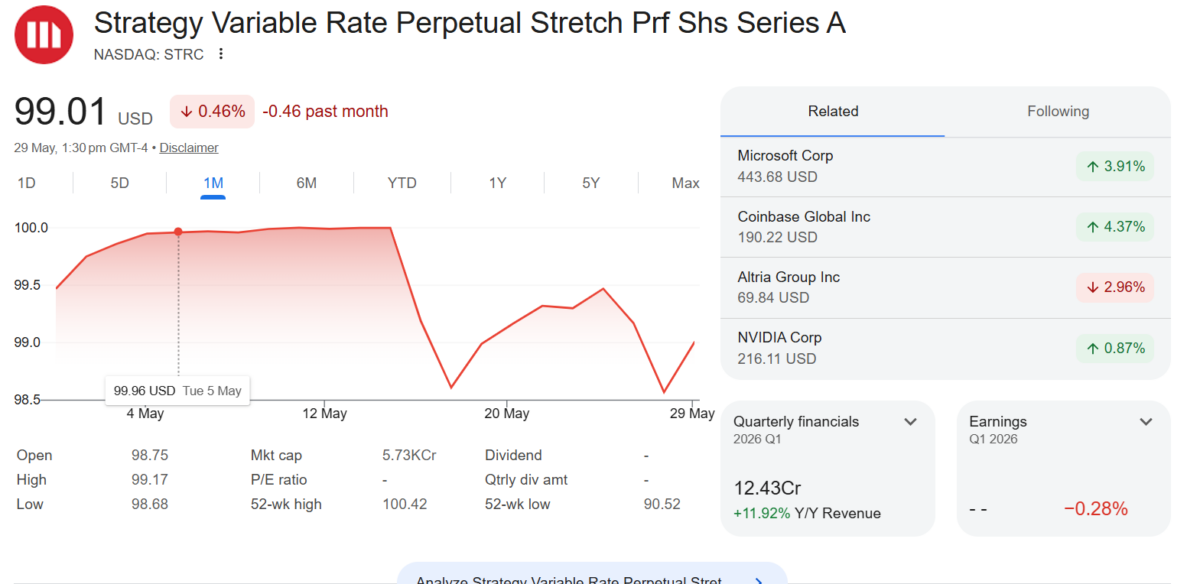

- Strategy’s STRC preferred stock fell as low as $97.11 before closing at $98.57.

- The drop came as Bitcoin slipped near $73,000, weighing on Strategy-linked securities.

- Strategy’s cash reserve has fallen to about $871 million after its recent convertible debt repurchase.

- The company faces roughly $1.7 billion in annual preferred dividend obligations.

- Strive’s SATA preferred stock has stayed closer to its $100 par value with a 13% dividend structure.

Strategy’s perpetual preferred security, STRC, slipped below the $99 level this week, raising fresh questions over whether the Michael Saylor-led Bitcoin treasury firm can keep the instrument trading close to its $100 target price.

STRC fell as low as $97.11 on Thursday before recovering to close at $98.57. The move came as Bitcoin dropped toward the $73,000 range, adding pressure to securities tied to Strategy’s balance sheet and Bitcoin accumulation model.

The decline matters because STRC was designed to trade near its $100 par value. A stable price near par allows Strategy to keep issuing shares through its at-the-market program and raise capital more efficiently. When the preferred stock trades below that level, the funding mechanism becomes less attractive for the company and more closely watched by investors.

Bitcoin Weakness Adds Pressure on STRC

STRC has historically come under pressure during Bitcoin drawdowns and around ex-dividend dates. The latest decline appears to reflect both forces: weaker Bitcoin price action and investor sensitivity to the preferred stock’s monthly dividend mechanics.

The security pays a variable cash dividend and is structured to remain close to its $100 stated amount. However, the latest move below $99 shows that market confidence in the structure can weaken when Bitcoin falls and Strategy’s liquidity position becomes a bigger part of the discussion.

For Strategy, this is not just a market-price issue. STRC is part of the company’s broader capital stack, which includes common equity, preferred securities, debt, and its large Bitcoin holdings. The preferred stock has become one of the tools Strategy can use to raise capital without relying only on common stock issuance or convertible debt.

Strategy’s Cash Reserve Falls After Debt Buyback

Investor attention has also shifted to Strategy’s cash position after the company repurchased $1.5 billion of its 0% convertible senior notes due 2029.

The transaction reduced Strategy’s debt burden, but it also drew down the company’s U.S. dollar reserve. Strategy’s cash balance fell from about $2.25 billion to roughly $871 million following the repurchase.

Strategy also has large preferred dividend commitments, based on current estimates, the company faces around $1.7 billion in annual preferred dividend obligations. At the current cash level, the reserve covers only about six months of those obligations, compared with the earlier goal of covering a much longer runway.

Strategy has said it plans to rebuild its cash reserve over time through a mix of capital sources, including common equity, preferred securities, and other market-based financing.

Saylor’s Capital Choices Come Under Focus

Executive Chairman Michael Saylor has previously pointed to several ways Strategy could meet dividend obligations and support its balance sheet.

Those options include issuing more MSTR shares when the stock trades at a premium to net asset value, selling additional STRC, or, in a more difficult scenario, selling Bitcoin. Saylor has repeatedly framed Strategy’s capital decisions around whether they increase Bitcoin per share for shareholders.

That makes STRC’s price important. If the preferred stock stays near $100, Strategy can continue using it as a cleaner capital-raising vehicle. If it remains below par, investors may question how effective the instrument can be in helping fund the company’s dividend obligations and Bitcoin strategy.

Strive’s SATA Draws Comparison

The pressure on STRC also comes as Strive’s preferred security, SATA, has remained closer to its $100 par value.

Strive has announced that SATA will move from monthly dividend payments to daily business-day dividend payments beginning June 16, 2026, while maintaining a 13% annualized dividend rate. The company has positioned the daily dividend structure as a stabilizing feature for investors seeking regular income.

Although the daily payout mechanism has not yet begun, SATA has stayed tightly linked to its $100 level in recent trading, even as Bitcoin weakened. That contrast has drawn more attention to STRC’s recent discount to par.

For Bitcoin treasury companies, preferred securities are becoming a key test of market confidence. The issue is no longer only how much Bitcoin a company holds, but whether its capital structure can remain durable when Bitcoin falls, cash reserves shrink, and dividend obligations keep running.

For Strategy, STRC’s move below $99 is a warning signal. It does not break the company’s model by itself, but it shows investors are watching the preferred stock, the cash reserve, and the dividend burden much more closely than before.

Also Read: Michael Saylor and Strategy’s Bitcoin Bets Face New Scrutiny Over Cash Deployment Choices