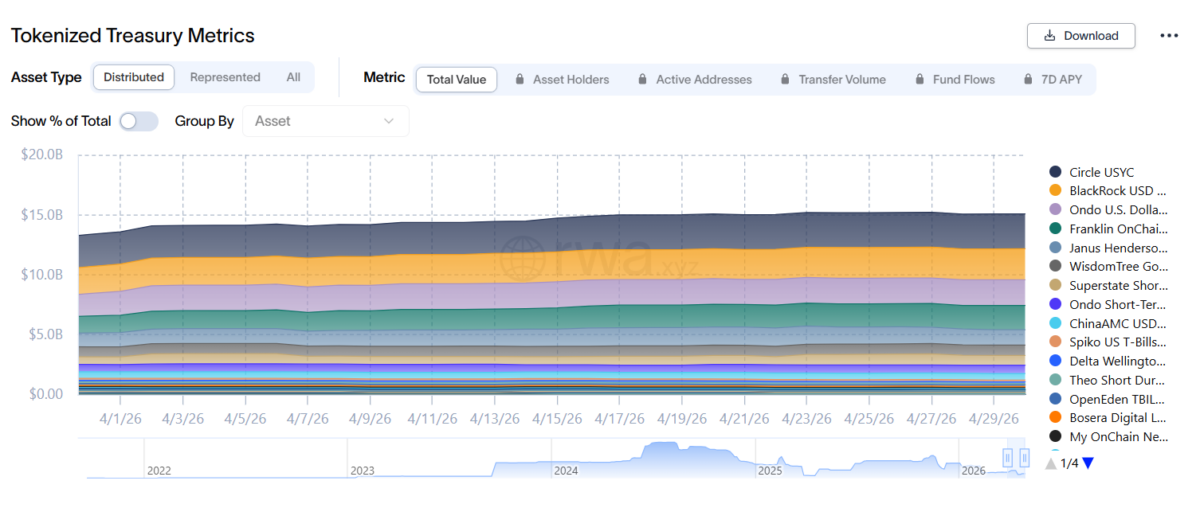

The tokenization story is no longer just about potential. It is now about scale. By late April 2026, tokenized US Treasuries had climbed to $15.07 billion, according to RWA.xyz, a level that shows how quickly blockchain-based versions of traditional safe assets are gaining traction. A few years ago, the idea of investors holding Treasury exposure through blockchain tokens still sounded experimental. Today, it looks much more like the early buildout of a new financial rail.

At the center of this shift are two products that have emerged as the market’s defining benchmarks: Circle’s USYC and BlackRock’s BUIDL. As of late April 2026, USYC leads the tokenized Treasury market with approximately $2.9 billion in assets, while BlackRock’s USD Institutional Digital Liquidity Fund (BUIDL) sits in second place at around $2.58 billion, reinforcing both firms’ positions as the main institutional drivers of the RWA narrative.

This matters because tokenized Treasuries have become something very different from a niche crypto theme. They now sit at the crossroads of traditional finance, stablecoin infrastructure, and on-chain capital markets. Investors are not just looking at them as an interesting use case. They are beginning to treat them as a practical way to earn yield, move collateral faster, and connect conservative fixed-income assets with digital trading systems.

The appeal is easy to understand. US Treasuries are among the most trusted and liquid financial instruments in the world. Once tokenized, they can be settled more quickly, moved more easily across platforms, and in some cases integrated into DeFi or digital asset workflows in ways that traditional wrappers cannot match. In simple terms, tokenization gives an old asset a new form without changing what makes the asset useful in the first place.

The growth this year has been sharp. RWA.xyz showed the total tokenized Treasury market at $13.53 billion on April 12, 2026, climbing to around $14 billion by April 22, and reaching $15.07 billion by April 29. The direction of travel has been clear throughout April, and the pace has not let up.

The April 2026 leaderboard

For the first time, the market has a clear leader that is not BlackRock. Circle’s USYC, acquired via Circle’s January 2025 purchase of Hashnote, surpassed BUIDL in mid-March 2026 and has maintained its lead since. By late April, the top five tokenized Treasury products looked like this:

The top five products together account for roughly 68% of the entire $15B+ sector. The top 20 issuers collectively manage approximately $13.5 billion in assets, confirming that while competition is intensifying, the market is not yet fragmented; it remains concentrated among a handful of regulated, institutional-grade issuers.

Why this market is growing so fast

Tokenized Treasuries are growing because they solve a real problem. In crypto, investors often have to choose between idle stablecoins that earn nothing and riskier DeFi strategies that can offer high returns but come with far more uncertainty. Tokenized Treasury products offer a middle path. They give investors exposure to short-duration government debt, which means they can earn yield from a relatively conservative underlying asset while staying closer to on-chain markets.

This is especially important in the current market environment. Tokenized Treasuries are starting to act as a core on-chain yield and reserve layer, competing both with inactive stablecoin balances and with riskier forms of crypto collateral. This puts them in a strong position. They are not trying to replace speculative crypto trades. They are offering a safer place for capital that still wants to remain inside digital finance.

There is also a strong institutional case. Treasuries already play a key role in traditional cash management, liquidity planning, and collateral systems. Once tokenized, these same functions can begin to move on-chain. This creates a powerful bridge between traditional asset managers and crypto-native infrastructure. For institutions, the value is not only yield. It is operational efficiency, programmable settlement, and the ability to use familiar assets inside newer digital systems.

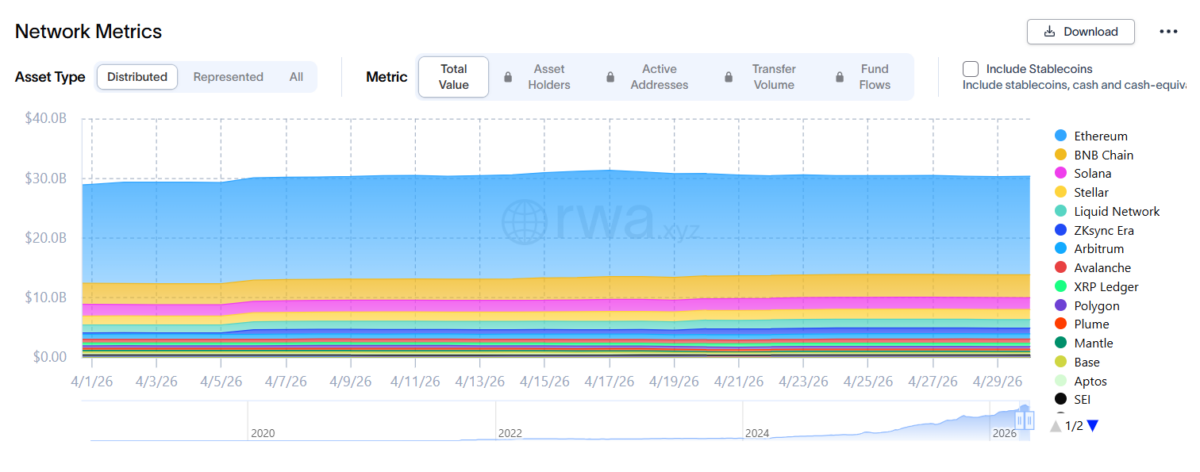

The market’s multi-chain expansion has helped as well. Ethereum and BNB Chain are the two largest networks for tokenized Treasuries, while products including BUIDL (available on Ethereum, Solana, Avalanche, Aptos, Optimism, Polygon, Arbitrum, and BNB Chain), USYC, USDY, and others have expanded their presence across several chains.

This matters because institutions and crypto users do not all operate in the same ecosystem. A product that can move across chains is easier to adopt and easier to plug into multiple platforms.

BlackRock’s BUIDL: Institutional benchmark, second-place product

BlackRock’s role in this market is bigger than the raw asset number suggests. Yes, BUIDL’s roughly $2.58 billion in late-April value is large on its own. But the real importance of BUIDL is symbolic as well as financial. When the world’s largest asset manager launches and scales a tokenized Treasury product, it changes how the rest of the market thinks about tokenization.

Before BUIDL, tokenization often looked like a promising but still fragmented trend. Crypto-native teams were building, and some traditional firms were experimenting, but the category lacked a defining institutional benchmark. BUIDL helped provide that benchmark. It told the market that tokenization was not only for startups or crypto funds. It could also fit into the operating model of a global asset-management giant.

The product itself is built to look familiar to institutional users. BUIDL holds US Treasury bills, cash, and repo-related exposure while distributing yield in an on-chain format. Securitize handles issuance and investor onboarding, giving the product a compliance-friendly structure that has made it a reference point for the broader sector. The $5 million USDC minimum entry means it targets US Qualified Purchasers specifically, not a retail product, but precisely the audience that needs credible institutional validation.

In December 2025, Securitize announced that BUIDL had crossed $100 million in cumulative dividend payouts since its March 2024 launch, the first tokenized Treasury product to hit this mark, demonstrating that the structure was not just theoretical but actively delivering income to holders at scale.

By February 2026, BUIDL was managing more than $2.2 billion, and by late April, it had grown to approximately $2.58 billion. That trajectory helps explain why so many institutional notes, dashboards, and research pieces now treat BUIDL as a foundational reference, even as Circle’s USYC has taken the top spot by AUM.

It is also worth noting that BUIDL’s market share has compressed significantly. At its peak in May 2024, BUIDL commanded approximately 46% of the entire tokenized Treasury market. By late April 2026, that share has fallen to the high teens as the category has grown and competitors have scaled. This is not a sign of weakness; it is a sign that BlackRock’s early entry helped legitimize a market that has since attracted serious competition.

Circle’s USYC: A new kind of leader

The story of Circle’s USYC is a useful counterpoint to BUIDL’s institutional model. Circle entered the tokenized Treasury space in January 2025 through its acquisition of Hashnote, the original issuer of USYC. The product caters primarily to non-US investors and is structured around 24/7 create-and-redeem functionality using USDC, Circle’s stablecoin, which already moves billions across blockchain rails daily.

A key driver of USYC’s growth has been its role as off-exchange collateral on BNB Chain through a partnership with Binance, which introduced USYC for institutional derivatives trading. This single relationship drove $1.84 billion of USYC’s supply onto BNB Chain and is largely responsible for USYC’s overtaking of BUIDL in March 2026. Circle CEO Jeremy Allaire described the use of tokenized Treasuries as collateral as ‘a major emerging use case,’ and the data backs him up.

USYC’s rise shows how a tokenized Treasury product does not need to be solely a yield vehicle. When it can also serve as productive collateral in derivatives markets, earning yield while backing trades, its utility to institutional users multiplies significantly.

This is bigger than two funds

Even though Circle and BlackRock are getting most of the attention, this story is much larger than USYC and BUIDL alone. Data from RWA.xyz highlighted the role of Centrifuge’s JTRSY (jointly managed with Janus Henderson and carrying an S&P AA+ credit rating), Franklin Templeton’s BENJI (notable for its $20 minimum investment, making it the most accessible product in the top five), and Ondo Finance’s USDY in pushing the total market higher.

This competition is healthy for the category. It creates more product variety, more liquidity pools, and more ways for institutions and platforms to experiment with tokenized fixed-income exposure. It also makes the market more durable. If the category were driven only by one issuer, it could still be dismissed as a one-off institutional showcase. Instead, April data shows an increasingly layered ecosystem where multiple regulated issuers are competing for a piece of the same opportunity.

Another important point is that tokenized Treasuries are helping define what the next stage of RWA growth could look like. Real estate, private credit, commodities, and other assets all matter to the broader tokenization story, but Treasuries have become the easiest on-ramp because they combine trust, clarity, and utility. In that sense, Treasury products are doing for RWAs what stablecoins once did for crypto payments: they are becoming the product that makes the broader theme easier to understand.

According to CoinGecko’s RWA Report 2026, the overall tokenized RWA market capitalization grew 256.7% across fifteen months, reaching $19.32 billion by the end of Q1 2026. Tokenized Treasuries accounted for more than half of that growth, adding $9 billion in value during the period.

Why on-chain treasuries matter for crypto

For crypto markets, the growth of tokenized Treasuries could be a structural shift. Traditionally, large pools of on-chain capital either sat in stablecoins or chased volatile yields across DeFi protocols. Tokenized Treasury products offer another option: conservative, yield-bearing exposure that can remain close to the digital asset ecosystem.

This changes the way capital can move. An investor no longer needs to fully exit on-chain markets to rotate into a safer yield product. Instead, they may be able to stay in a tokenized format while lowering risk. This creates a more mature capital stack. In simple terms, crypto stops looking like a market that only offers speculation and starts looking more like a financial system with layers of risk, liquidity, and capital efficiency.

Tokenized Treasuries are increasingly described as a growing reserve layer for on-chain finance, and that may be the most useful way to think about them. They are not only an investment product. They are also becoming infrastructure. If a tokenized Treasury can be used as collateral, as a store of value, or as a low-risk yield source, then its role in crypto becomes much more important than its headline market value alone would suggest.

This is also why the multi-chain trend matters. Products that live only on one chain have a more limited reach. Products that can move across Ethereum, BNB Chain, Solana, Avalanche, Polygon, Arbitrum, and other networks are better positioned to become foundational tools rather than niche wrappers. Both BUIDL and USYC have pursued broad chain expansion aggressively, and it is showing in their AUM figures.

What comes next

The next stage of the market will depend on whether tokenized Treasury products remain mostly yield tools or expand into a deeper collateral layer for digital finance. If they are increasingly used in lending, settlement, fund management, and cross-platform liquidity operations, as USYC’s BNB Chain integration already demonstrates, then this market could grow much larger than it looks today.

BlackRock will remain central to this story because BUIDL helped legitimize the category. But Circle’s USYC has shown that institutional pedigree is not the only path to scale; the right product structure and distribution partnerships can move the needle just as fast. The long-term winner may not be one issuer. It may be the model itself: using blockchain to wrap conservative, high-quality assets in a form that moves faster and works more flexibly than old financial plumbing.

This is the real significance of the April 2026 data. The numbers are not just larger. They show that the market has moved into a new stage. Tokenized Treasuries are no longer a test case. They are becoming one of the clearest examples of how blockchain can fit into mainstream finance, without needing to reinvent the underlying asset.

Also Read: RWA Tokenization Surges to $19.3B as Institutional Adoption Accelerates