Bitcoin (BTC) continued its slide into the new month, trading around $58,500–$59,100 as of early UTC trading on July 1, having broken decisively below the psychologically important $60,000 level in late June.

Ethereum (ETH) lagged further, hovering near $1,580–$1,590. The broader cryptocurrency market capitalization stood at approximately $2.04 trillion, with Bitcoin dominance holding a 57.7% range.

This marks a sharp correction from earlier 2026 highs, with BTC now more than 50% off its all-time peak near $126,000. Total crypto trading volumes remained elevated amid the volatility, while sentiment indicators flashed “Extreme Fear.”

Macro Headwinds Intensify: AI Trade Cracks, Higher-for-Longer Rates

The selloff in digital assets has been tightly correlated with traditional risk markets, particularly the unwinding of the long-running AI trade. On June 29 and into early July, Nasdaq fell sharply (down around 4.5% in one session referenced in recent updates), marking multiple consecutive losing days. Semiconductor stocks were hammered, with the SMH ETF down as much as 7% in a single day and Korea’s chip-heavy KOSPI triggering circuit breakers.

Even strong corporate results failed to stem the tide. Micron Technology beat earnings expectations and raised guidance yet saw its stock sell off, a classic sign that lofty valuations had priced in perfection. Broader rotation was evident as the Russell 2000 held relatively firm while large-cap tech bled.Inflation data added fuel to the fire. The May PCE reading came in at 4.1%, the highest since 2023, reinforcing expectations for “higher for longer” interest rates.

Markets began pricing in a potential rate hike as early as September. The U.S. dollar strengthened toward one-year highs near 101, acting as a headwind for risk assets, while oil prices eased (Brent down significantly on the week), offering some relief on the energy front.

Crypto Caught in the Crossfire: ETF Outflows and Liquidity Concerns

Digital assets did not decouple from the risk-off mood. According to Wintermute, a leading crypto market maker and OTC desk, BTC fell 5.9% on the referenced session, tagging a low near $59,300 before stabilizing around the $60k handle (subsequent trading pushed it lower into early July). ETH underperformed with a 7.9% drop, trading near $1,580.

Spot Bitcoin and Ethereum ETFs saw substantial outflows, with Wintermute estimating roughly $1.8 billion exiting in the week leading into the update, among the largest weekly redemptions since the products launched.

This comes as crypto’s role as the “highest-beta macro asset” appears to have diminished. Marginal liquidity now finds more attractive homes in AI-related equities, Wintermute noted, meaning even an eventual macro easing may not immediately flow into crypto.

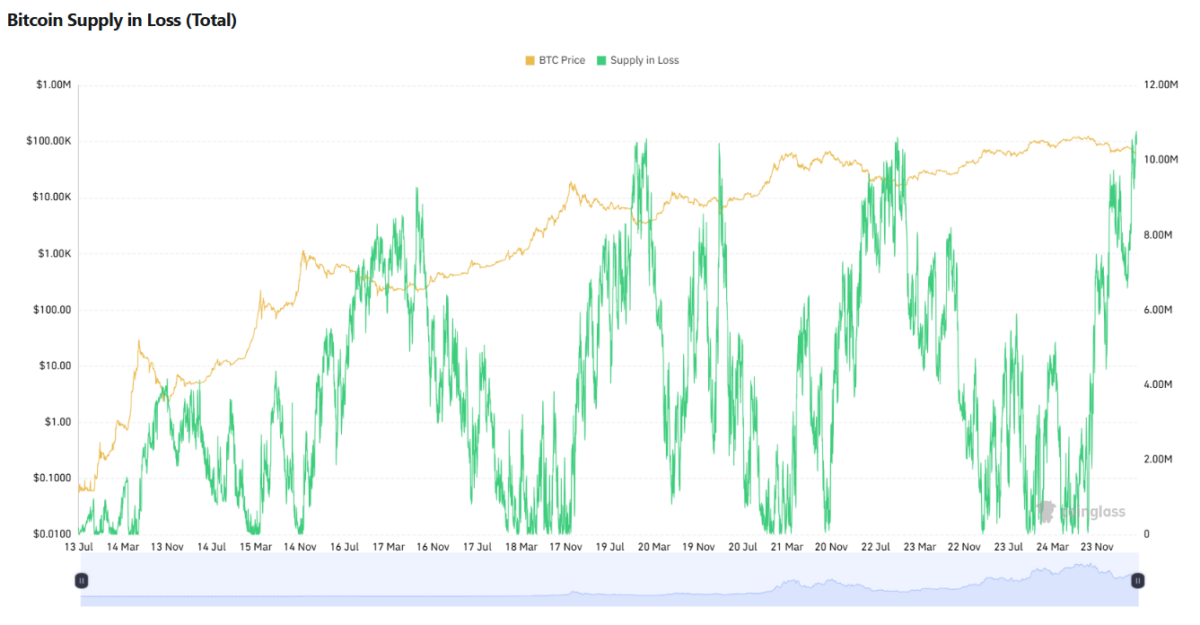

On-chain metrics painted a picture of mounting capitulation. The share of Bitcoin supply held at a loss was pushing toward the 50% mark (nearly 10.77 million BTC), a level historically associated with cycle lows, though Wintermute cautioned that prior cycles often saw this crossover closer to 60%, suggesting potential for more pain.

The Fear & Greed Index lingered in Extreme Fear territory (around 17–24), a zone it has largely occupied since the October 2025 top.

Strategy’s Bold Move: Buybacks, Higher Dividends, and Conditional BTC Sales

One bright spot in the storm was the response from Bitcoin treasury heavyweight Strategy (closely tied to MicroStrategy/MSTR dynamics). The firm unveiled a new “Digital Credit Capital Framework” designed to stabilize its capital structure. Key elements included:

- Raising the STRC dividend to 12% to push it back toward par.

- Authorizing $1 billion in preferred and $1 billion in common stock buybacks.

- Building a substantial USD reserve covering over 17 months of dividends and interest.

- For the first time, formally authorizing up to ~$1.25 billion in BTC sales (roughly 2.5% of holdings) to fund obligations and buybacks.

Markets initially reacted positively, with MSTR and STRC shares rallying and BTC briefly reclaiming the $60k level. Wintermute viewed the move as pragmatic, noting, “the Strategy framework is the right call for the company and takes the disorderly-blowup tail risk off the table.”

However, the firm highlighted the broader implication: a major Bitcoin treasury entity now reserving the right to sell BTC to cover dividends signals a shift from an unconditional “permanent bid” to a more conditional one.

Wintermute’s Assessment: “Advanced in the Bear, But Likely Not the Bottom”

In its detailed June 29 analysis, Wintermute concluded that the market has entered an advanced stage of the bear phase, with capitulation underway but the true cycle bottom still ahead. Key supporting factors for further downside risk include persistent ETF outflows and unchanged liquidity metrics, the structural preference for AI equities over crypto as liquidity returns, weak summer seasonality, and BTC testing the 200-week moving average.

At the time of publishing, Bitcoin is trading around $58,657, consolidating near recent lows after a steep multi-week decline. The price remains firmly below its key moving averages (50, 100, and 200-period), which are sloping downward and acting as dynamic resistance.

BTC has tested the lower $58,000 zone multiple times, with the 200-week moving average (visible on higher timeframes) providing psychological support. Momentum indicators show oversold conditions but lack strong bullish divergence yet, suggesting the near-term bias remains cautious unless the price can reclaim the $59,500–$60,000 area with conviction. Volume has been elevated during selloffs, reflecting ongoing distribution pressure.

Moreover, Bitcoin has closed below its 200-week moving average for the first time since 2023, according to market data provider Barchart. Historically, such breaches have marked notable long-term buying opportunities, though current macro pressures and ETF outflows add layers of caution to the signal.

Wintermute anticipates the true low may not arrive before September to October 2026, contingent on macroeconomic developments, capital flows, and whether the AI trade continues to cool. Near-term catalysts include U.S. payrolls data (brought forward ahead of the July 4 holiday), Bitcoin’s ability to defend the $58k–$60k zone, and how Strategy-related assets trade under the new framework.

“Sentiment is definitely washed out… Capitulation is happening. The nuance is that in prior cycles the cross [of supply in profit/loss] happened closer to 60%, so there may be more pain left,” the firm observed.

Broader Market Snapshot and Outlook

As of the latest data, the total crypto market remains under pressure but shows signs of consolidation rather than outright capitulation. Altcoins have generally underperformed Bitcoin, with many majors posting deeper percentage losses. Stablecoin volumes and on-chain activity provide some underlying resilience, but derivatives liquidations and funding rates reflect cautious positioning.

Looking ahead, the interplay between traditional macro (rates, inflation, equity rotations) and crypto-specific dynamics (ETF flows, treasury company strategies, on-chain capitulation) will be decisive.

A cooling in the AI trade could eventually unlock capital for crypto, but Wintermute stresses that confirmation via renewed buying pressure, rather than just washed-out sentiment, is still missing.

Also read: Trump Earned $635M From His Memecoin—Far More Than His Bitcoin