The law firm that spent the past year suing Pump.fun and celebrity-memecoin promoters has a new and far larger target: Magic Eden, one of crypto’s best-funded marketplaces, in a proposed class action alleging its $ME token was sold on promises it failed to keep.

From memecoins to a major marketplace

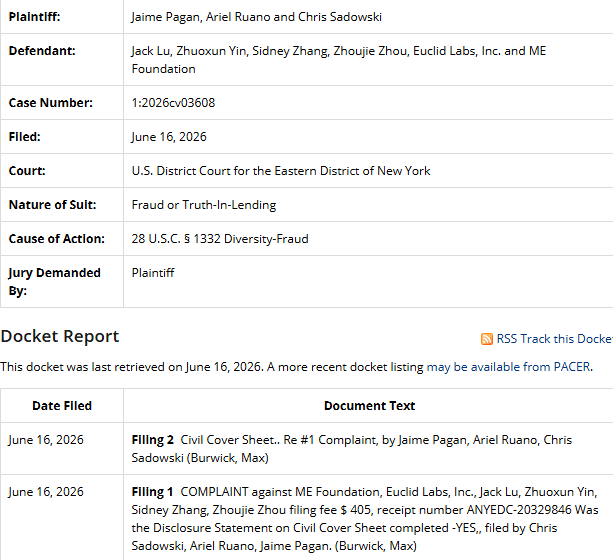

The complaint was filed on June 16 in the U.S. District Court for the Eastern District of New York by plaintiffs Jaime Pagan, Ariel Ruano, and Chris Sadowski. It names Magic Eden’s corporate entity, Euclid Labs Inc., the ME Foundation, and the marketplace’s four co-founders — chief executive Jack Lu, Zhuoxun Yin, Sidney Zhang, and Zhoujie Zhou — and is brought by Burwick Law, the firm whose managing partner Max Burwick has become the most recognizable plaintiff’s litigator in crypto.

That lineage is what makes the filing notable. Burwick Law, often alongside Wolf Popper, has spent 2025 and 2026 pursuing a string of token cases: a sprawling class action against the Solana memecoin launchpad Pump.fun that later expanded into racketeering claims and suits over celebrity tokens, including Haliey Welch’s HAWK and Caitlyn Jenner’s JENNER.

Those targets were, by and large, fly-by-night coins and influencer cash-grabs. Magic Eden is a different category of defendant: a leading multi-chain NFT marketplace founded in 2021, with roughly $157 million raised from investors including Paradigm, Sequoia, and Greylock, and a valuation around $1.6 billion. The case is an early test of whether the consumer-protection playbook refined on memecoins can reach the token of an established venture-backed platform.

The promises the suit says went unkept

At the center of the complaint is the gap between what $ME was marketed to do and what it allegedly delivered. When the token launched on December 10, 2024, Magic Eden promoted it as the utility and governance backbone of its ecosystem—a token holders could use to pay trading fees across multiple blockchains, that would confer voting power through an “ME DAO” governance system, and that would reward users for trading or staking.

The plaintiffs argue those features arrived late, changed materially, or never launched as promoted, and that buyers paid more for $ME than they otherwise would have because it was presented as having practical utility inside a larger Magic Eden ecosystem.

The launch itself was rocky in ways the suit leans on. $ME debuted near $6.70, spiked toward $13, then crashed roughly 67% the same day, as a buggy mobile app and a convoluted claim process drew widespread complaints, with some users reporting difficulty claiming at all. For buyers who acquired the token on its promoted utility and then watched its value fall, the complaint frames the loss not as ordinary market volatility but as the foreseeable result of marketing claims that outran the product.

Why it’s a consumer case, not a securities case

The most strategically important feature of the lawsuit is what it does not allege. It pleads no securities law claims. Instead, it relies on New York consumer-protection statutes—General Business Law sections 349 and 350, which cover deceptive business practices and false advertising—together with negligent misrepresentation and unjust enrichment, and reaches federal court through diversity jurisdiction rather than any federal securities hook.

That framing is deliberate, and it reflects where token litigation has migrated. After the Securities and Exchange Commission’s February 2025 staff statement indicating that many memecoins are not securities under federal law, the securities route became harder to travel for this class of token.

Consumer-protection and false-advertising law offers plaintiffs an alternative that sidesteps the question of whether $ME was an unregistered investment contract entirely, keeping the focus on consumer-facing marketing—what buyers were told and whether it was true. It is the same alternative-remedy theory being tested in the celebrity-token and Pump.fun cases, now aimed at a platform token rather than a meme.

What the case tests

For all its significance, the suit is at its earliest stage. It is a proposed class action; no class has been certified, the allegations are unproven, and Magic Eden has not issued a public response to the claims. The docket so far shows only the initial complaint and a civil cover sheet; there is no ruling, and the founders have been neither found liable nor cleared of anything.

What the case will test, if it advances, is broader than one token. A win or even a survivable complaint would suggest that token issuers — including well-capitalized, reputable platforms, not just anonymous memecoin deployers — can be held to their marketing under ordinary consumer-protection law, regardless of whether their tokens are deemed securities.

That is a materially different exposure than the securities fights that have dominated crypto’s legal landscape, and it lands on a company that built its brand on being a legitimate, institutional alternative to the market’s wilder corners. Whether $ME’s promoted utilities count as actionable misrepresentations or merely a roadmap that slipped is the question a court will now, eventually, have to weigh.