Key Highlights

- DeFi smart contracts rely on oracle data, limiting true autonomy and concentrating control at the data layer.

- Chainlink’s success has made it a critical dependency across DeFi, turning a security solution into a source of systemic risk.

- LINK operates mainly as a payment token for oracle services, with usage driving distribution rather than value capture.

Decentralized finance (DeFi) has always promoted itself as a complete alternative to the trust-based system of traditional banks. Its main idea is simple but ambitious: replace human judgment with automated code, replace banks and institutions with smart contracts, and make decision-making transparent and unchangeable.

In theory, once a smart contract is on the blockchain, it runs automatically and fairly, without favoritism, censorship, or human intervention. This promise has proven powerful. Over successive market cycles, more than $100 billion in capital has flowed into on-chain lending markets, decentralized exchanges (DEXs), derivatives protocols, and synthetic asset platforms.

For many participants, DeFi represents not merely a new asset class, but an alternative financial system—one that claims to be resilient precisely because it eliminates trust.

The Oracle reality: Where autonomy breaks down

This framing collapses under closer examination, because smart contracts are not autonomous in any meaningful real-world sense. A blockchain is a closed computational environment. It cannot observe the price of Ether, the exchange rate between the dollar and the euro, the solvency of a custodian, or the outcome of a real-world event.

A lending protocol does not inherently “know” when collateral has lost value. A derivatives contract cannot independently calculate profit and loss. Every such function depends on external information being injected into the system. That injection point is the oracle layer.

Chainlink and the consolidation of reality

Centralized perception of the reality of decentralized finance was achieved with Chainlink as the primary tool for how decentralization would be defined, therefore creating a monopoly on the technology that allows people to interact with and view the reality of their transactions.

In most instances, when people transact in decentralized finance, they are doing so through smart contracts. When they do this, they are utilizing or “executing” the functions of the smart contracts without any sort of third-party title (intermediary). In turn, the perception of what is real for decentralized finance has been consolidated within one singular central authority.

This creates a deeply asymmetric architecture. Execution may be distributed, but observation is not. And because financial systems are only as robust as their weakest assumptions, the normalization of a single source of truth represents a form of systemic risk that would be considered unacceptable in traditional finance, yet remains largely unexamined in crypto discourse.

From emergency solution to structural dependency

Chainlink’s rise was neither accidental nor malicious. It emerged during a period when decentralized finance was failing under the weight of its own naivety.

Between 2019 and 2020, early DeFi protocols routinely relied on single-source price feeds, often pulling data directly from centralized exchanges or public APIs. These designs proved catastrophically fragile. Flash loan attacks took advantage of low liquidity and easily manipulated prices, draining protocols by briefly changing prices just enough to cause wrongly priced liquidations.

Chainlink’s practical solution

Chainlink solved this problem not by being perfectly decentralized, but by setting a practical standard for what “secure enough” looks like in the real world. It aggregated prices from multiple sources, processed them through a network of independent node operators, and published a single reference price on-chain. This did not eliminate manipulation, but it raised the cost of attack beyond what most adversaries could sustain.

For developers trying to keep their protocols alive, Chainlink was not an ideological choice. It was a survival mechanism.

As more value flowed into protocols secured by Chainlink feeds, the network effect became self-reinforcing. Liquidity gravitated toward applications that used Chainlink because they were perceived as safer. Auditors started to take for granted the use of Chainlink as a baseline for their operations.

The risk models, liquidation engines, and emergency procedures across the ecosystem were fine-tuned to Chainlink’s update cadence and aggregation logic. Eventually, this process solidified the structure of the system.

By the mid-2020s, Chainlink was no longer a component that could be easily replaced. It had become a structural dependency, deeply embedded in the financial nervous system of DeFi.

The dependency trap: When there is no redundancy left

In spite of DeFi’s insistence on decentralization, the design of its oracles has evolved into a single point of failure that closely resembles a centralized system. Most major protocols rely on Chainlink feeds as their sole source of reference.

While fallback mechanisms often exist on paper, switching to alternative feeds in a live production environment is operationally difficult, risky, and rarely tested under real stress conditions. This creates a monoculture.

When a large number of protocols depend on the same ETH/USD feed, they inherit the same assumptions around latency, aggregation, and market structure. If that feed is delayed, manipulated, or paused, the impact is not isolated. It propagates immediately across the entire ecosystem.

When infrastructure risk turns into market risk

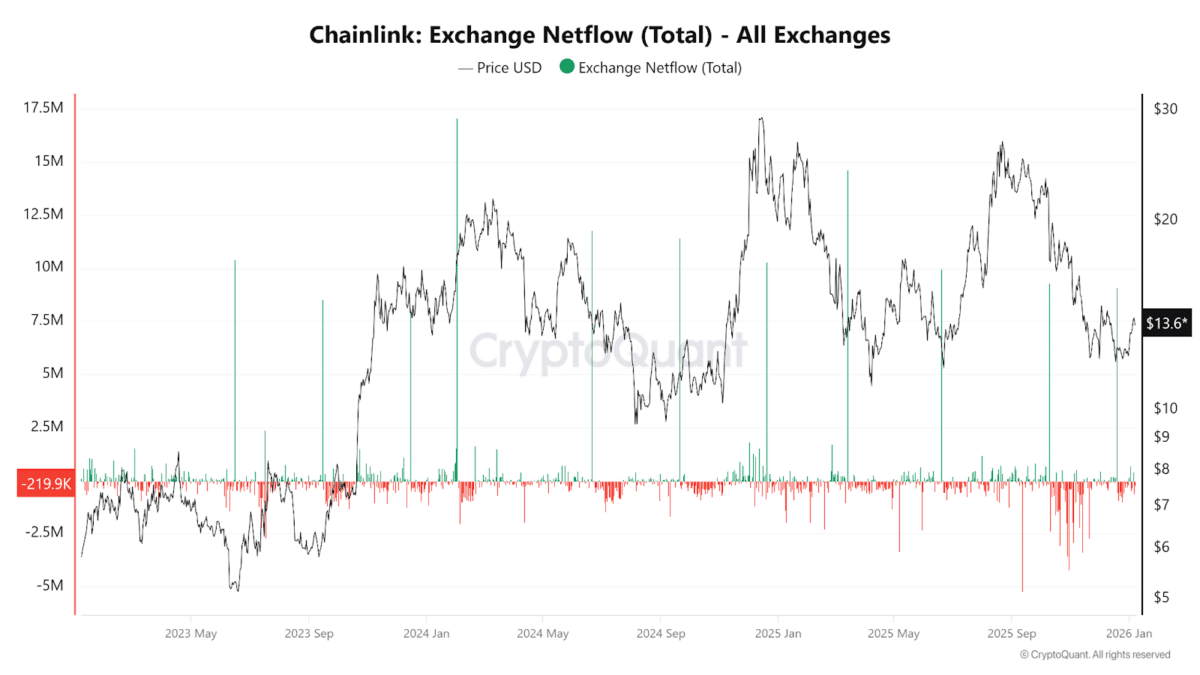

The financial consequences of this dependence are reinforced by CryptoQuant data. During major market downturns, LINK exchange netflows rise sharply, indicating defensive positioning by large holders. The asset securing DeFi’s oracle layer behaves like a high-volatility risk token precisely when the system requires maximum stability.

In effect, DeFi’s core data infrastructure is tied to an asset that is itself highly sensitive to market stress.

Where does Chainlink (DeFi) even get prices from?

Most people using DeFi never think about where prices actually come from. A lending app does not magically know the price of Bitcoin or Ethereum. A smart contract cannot check a chart or open an exchange.

Chainlink exists because DeFi needs someone to tell it what the market price is.

Chainlink collects price data from large centralized exchanges, major decentralized exchanges, and established market data providers where real trading volume exists. These are the same places where billions of dollars are traded every day and where prices are actually formed.

Multiple Chainlink node operators collect this price data independently. Each node submits its data on-chain, and a smart contract combines all the values and publishes a final price, usually based on the middle value. That final number is what DeFi protocols treat as reality.

At its peak, Chainlink secured more than $76 billion across DeFi and has processed over $27 trillion in total transaction value. That means a very large part of DeFi depends on Chainlink prices every single minute.

Has Chainlink ever gone down or faced outages?

Chainlink has never fully shut down, but there have been moments during extreme market chaos when its systems were under heavy pressure. In those situations, even small delays or pauses became important, because a lot of money across DeFi depends on price updates happening on time.

In March 2020, during the COVID market crash, Ethereum prices dropped rapidly while network congestion pushed gas fees above $200 per transaction. Because posting updates became extremely expensive, some Chainlink price feeds stopped updating for nearly six hours.

No wrong prices were published, but DeFi lending platforms could not liquidate risky loans in time, which increased losses once prices were finally updated.

In May 2022, during the Terra collapse, the LUNA token crashed by over 90%, and prices fell from above $80 to almost $0 in a very short period. During the Terra crash, Chainlink stopped updating its LUNA price feeds to avoid showing inaccurate data from a market that had basically collapsed.

Even so, many DeFi platforms kept using the last price that had been published, which was much higher than LUNA’s real value at the time. This led to people borrowing against worthless collateral, ultimately causing about $11 million in losses on platforms like Venus.

In both of these cases, the problem was fixed within a few hours, and no one tampered with the data. Still, the losses happened because these automated systems rely on constant, up-to-date prices to work correctly.

Oracle dependence and the illusion of backup

People often defend Chainlink’s dominance by saying it’s already redundant since many nodes provide data. But this misses the real risk.

Even though several operators supply data, they usually get it from the same sources, have similar financial limits, and react to the same market conditions. Aggregation smooths individual errors, but it does not create an independent truth. It produces consensus around a shared dataset.

Logical versus real redundancy

In traditional finance, redundancy comes from genuinely independent systems: competing pricing vendors, separate clearinghouses, and parallel settlement rails. In DeFi, redundancy is often simulated rather than real.

Multiple protocols reference the same oracle contracts, the same aggregation logic, and frequently the same exchanges. This results in logical redundancy without physical independence.

The core risk is not occasional oracle failure, but synchronized behavior. When stress hits, every dependent system reacts in the same way, at the same time, using the same information. This is how localized issues escalate into systemic crises.

Centralization hiding in the open

Chainlink is often described as decentralized because it relies on many node operators. Decentralization isn’t just about having many participants; it’s about who actually makes the decisions.

At the core of Chainlink’s system is a multi-signature wallet that controls things like contract updates, feed settings, and emergency actions. Because this wallet has historically been managed by only a few people, it gives a lot of power to a small group, which doesn’t match the idea of a fully decentralized network.

Operational participation is also limited. High-value feeds are serviced by whitelisted operators chosen by the core team. These operators are typically large, professional infrastructure firms, which improves reliability but introduces identifiable choke points.

From a regulatory standpoint, this structure is critical. Applying pressure to a small set of known entities is far more effective than regulating a diffuse, anonymous network. DeFi’s oracle layer—far from being censorship-resistant—may be one of the most easily regulated parts of the entire ecosystem.

Chainlink and the re-creation of financial gatekeepers

Decentralized finance was born out of a distrust of intermediaries, yet the oracle layer has quietly recreated a familiar hierarchy.

Chainlink does not merely provide data; it determines which data sources are legitimate, which node operators are trusted, and which feeds are considered canonical. This mirrors the role of credit rating agencies in traditional finance, whose judgments are technically advisory but functionally authoritative.

Just as a downgrade from a major rating agency can cascade through bond markets, an oracle update can ripple through DeFi. Liquidations trigger, collateral values shift, and solvency assumptions change instantly. The power to define reality confers power over outcomes, even if exercised indirectly.

This concentration is especially concerning because Oracle decisions are not subject to the same scrutiny as protocol governance. There is no transparent voting process for feed inclusion, weighting, or depreciation. Decisions are framed as technical necessities rather than policy choices, even though their consequences are economic and systemic.

When accurate data produces wrong outcomes

One of the most misunderstood risks in oracle design is that failure does not require malfunction.

Chainlink nodes don’t just make up prices; they grab them from exchanges and aggregators. The problem is that in markets where not a lot is being traded, someone can mess with things pretty easily through normal trading. A person could briefly mess up prices in those markets where there’s not good liquidity and get the oracle to report a price that’s technically correct but still misleading.

The oracle does its job as it should, but things still go wrong badly. Liquidations happen, collateral gets taken, and value disappears—even though there’s no actual bug or exploit in the oracle.

This kind of thing has led to billions of dollars in losses in DeFi. It shows a key problem with how oracles gather data: they can’t tell the difference between real price changes and when someone’s messing with the market.

The danger of failures that happen as designed

One of the worst parts about Oracle problems is that they often happen even when everything seems to be working the way it’s supposed to.

When price manipulation, stale updates, or source-level distortions occur, Chainlink frequently behaves exactly as specified. Nodes fetch data, aggregation executes correctly, and the result is published on-chain. From a technical standpoint, nothing is broken. Yet the economic outcome can still be disastrous.

When correct data still breaks the system

This reveals a gap between getting the numbers right and keeping the system safe. DeFi protocols often assume that if the data is technically accurate, the outcome will automatically be fair. But real markets don’t work that way. In adversarial conditions, accuracy and fairness are not the same thing.

A price can be “correct” for a brief moment, reflecting real trades in a thin or manipulated market and still cause serious damage when it is used to trigger liquidations or other irreversible actions.

Traditional financial systems recognize this risk. That’s why they rely on circuit breakers, manual overrides, and human judgment to slow things down when markets behave irrationally or are clearly being gamed.

DeFi, by contrast, treats oracle outputs as final, because there is no institutional layer empowered to intervene once execution begins.

Gas costs, stale prices, and cascading insolvency

Under extreme market conditions, Ethereum gas fees can spike dramatically, sometimes even exceeding 500 gwei. Oracle updates become expensive. Node operators face a rational decision: publish updates at a loss or delay.

When updates are delayed, prices become stale. Positions that should be liquidated remain open, accumulating hidden insolvency. When the oracle eventually updates, the correction is sudden and violent, triggering liquidation cascades that overwhelm liquidity and leave protocols with bad debt.

This phenomenon is not theoretical. It is an emergent property of oracle-based systems operating on fee-constrained blockchains.

Liquidity problems and oracle feedback

One overlooked risk is how oracle pricing and on-chain liquidity affect each other.

When oracles report lower prices during market craziness, automated market makers change pool balances. This makes slippage bigger, and liquidity seems to disappear. Then, the price changes get bigger on the same exchanges that feed info to the oracle network.

So, it’s like a loop: oracle updates mess up liquidity, which makes price signals worse, which messes with the oracle aggregation. When things get really wild, oracle prices can go out of whack, even without anyone trying to cheat.

LINK exchange balances fluctuate during volatile periods, showing shifting liquidity even without major price moves.

CryptoQuant’s data from times of high volatility shows LINK exchange activity jumping without the prices really changing much. This suggests liquidity is all over the place instead of orderly markets. And this happens when Oracle reliability is needed most, but it’s also hardest to guarantee.

Tokenomics weirdness: Usage without value

One thing that doesn’t make sense in crypto is that Chainlink is being used a lot, but the LINK token isn’t doing so great.

As of January 2026, LINK is trading around $13.92, which is way down from the $23.65 it was trading at a year ago. That’s a 41% drop while Chainlink’s usage in the real world has blown up. The network has handled over $27.3 trillion in transactions, and it secures over $76 billion. That’s as much as some big financial companies.

This isn’t just because of bad market feelings or short-term hype. It’s a built-in thing.

Chainlink’s oracle network isn’t really paid for by steady fees. Instead, it’s like a subsidized system. Node operators get paid in LINK tokens from reserves the protocol controls. About 70 million LINK per year, or around 7% of the total supply, gets released to keep things running.

But node operators have real costs that they can’t pay in LINK. They have to pay for infrastructure, compliance, servers, and Ethereum gas fees in regular money or ETH. So, they usually sell LINK tokens to cover these costs, which puts constant pressure on the price.

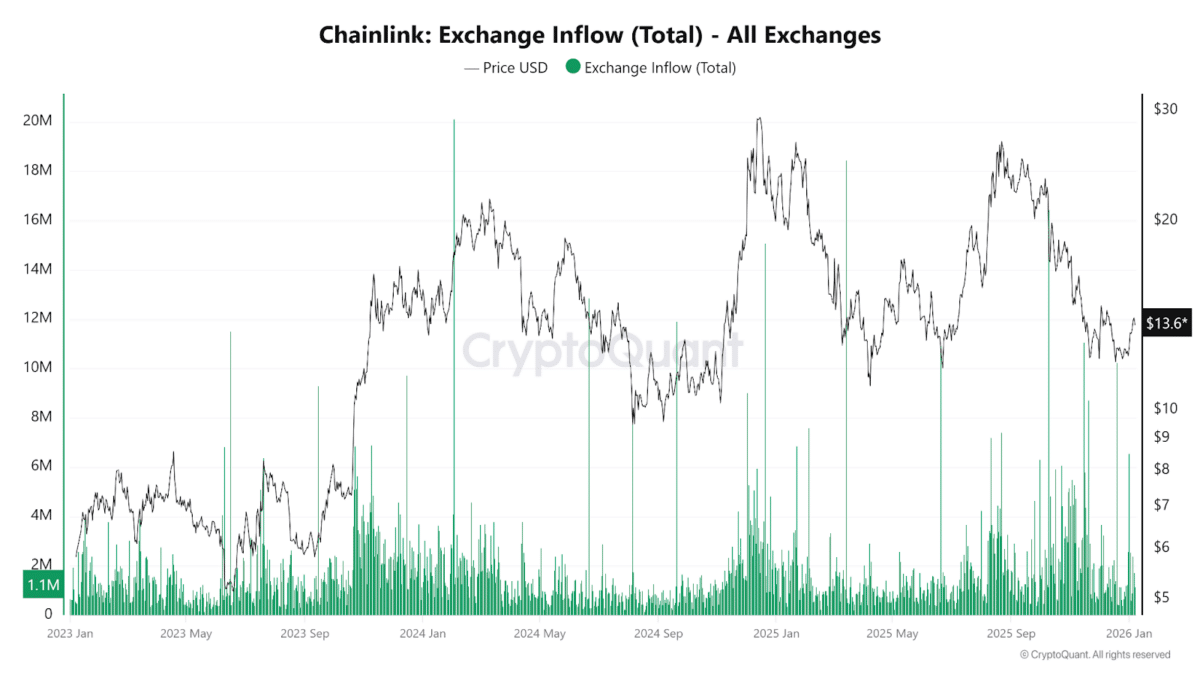

CryptoQuant’s exchange data shows this too. When the price goes up, LINK flows into centralized exchanges more. This means people are selling off their LINK rather than holding onto it. LINK is less of a store of value and more of a token used to keep the infrastructure running.

This creates a paradox at the heart of the network. The more Chainlink is used, the more LINK must be sold to sustain that usage. Adoption does not drive scarcity; it drives distribution.

LINK as a labor token, not a value token

Many people assume that LINK works like ETH or BTC, where more usage should lead to long-term value. In reality, that isn’t how LINK is used. LINK is mainly paid to oracle operators for the data they provide, rather than functioning as an asset that reflects the network’s growth.

LINK’s incentive structure under stress

This shows up clearly in on-chain data from CryptoQuant. LINK activity rises during periods of high oracle demand or market stress, not during phases of steady accumulation. Exchange inflows often increase at these times, suggesting that node operators and other participants are selling rewards to fund operations or reduce exposure, instead of holding LINK as a long-term value asset.

This places LINK in a structurally different category from assets whose supply dynamics are directly tied to demand. Increased oracle usage does not reduce circulating supply; it accelerates distribution.

As Chainlink grows and more data is used, more LINK needs to be paid out to keep the system running. That means a steady amount of LINK is constantly being sold to cover real operating costs.

This also helps explain why LINK often fails to hold rallies even when the fundamentals look strong. When the price goes up, the rewards paid to operators become worth more in fiat terms, which gives them more reason to sell quickly. The result is a feedback loop where higher prices lead to more selling, making it hard for LINK to stay scarce even as the network succeeds.

Why DeFi has not stress-tested its backbone

Despite its scale, DeFi has not conducted systemic stress testing of its oracle layer in the way traditional financial systems test clearinghouses and payment rails.

There are no industry-wide simulations of oracle outages, delayed updates, or coordinated feed manipulation. There are no standardized fallback drills. Each protocol assumes that its own safeguards are sufficient, ignoring the shared dependencies beneath them.

The lack of any shared approach to risk points to a deeper problem: no one is responsible for how the system holds up as a whole. Chainlink focuses on securing data feeds, protocols focus on smart contracts, and users are expected to manage their own risk. But there is no single party accountable for whether everything still works when markets come under stress.

What this creates is a coordination problem. Each participant is acting logically within their own role, yet the combined outcome is a system that becomes fragile when it is tested.

The regulatory pressure vector no one prices in

As regulatory attention increases, oracle providers are being pushed into an uncomfortable position. They are not just neutral software tools; they actively supply data that directly affects financial transactions and asset movements.

If regulators begin to treat oracle operators as part of the financial infrastructure, they could be forced to follow compliance rules that clash with DeFi’s assumptions of neutrality. Obligations to block certain addresses, assets, or regions would effectively introduce censorship at the data level, changing how “permissionless” these systems really are.

Because Chainlink’s node set is permissioned and professionally operated, it is uniquely exposed to this pressure. Oracle operators, unlike anonymous miners, are known and can be held legally responsible. This creates a one-sided weakness that code alone can’t fix.

From regulatory exposure to institutional lock-in

As Chainlink grows into institutional infrastructure with CCIP and its Runtime Environment, it gets even more dominant. When banks and settlement networks integrate with it, it becomes the go-to oracle layer.

But this success makes the system more fragile. It becomes harder to switch, and dependency gets stronger. What started as a practical choice turns into something that can’t be avoided.

Strangely, there’s not much talk about having various oracle options in DeFi.

For real strength, several independent oracle networks should run side by side. Protocols should be designed to handle conflicting information instead of relying on just one source. This would make things more complicated, slower, and less clear, but it would also lower the risk of big disasters.

The industry hasn’t gone this way because it values speed over strength. If Chainlink keeps working well enough, there’s little reason to change. But history shows that we usually only see infrastructure risks after something fails, not before.

This is super important now because Chainlink is moving into cross-chain messaging, institutional settlement, and real-world asset infrastructure. It’s not just for DeFi anymore; it’s becoming a general tool for coordinating digital finance.

This raises the stakes considerably. A failure, compromise, or regulatory capture at this layer would not merely disrupt DeFi protocols; it could ripple into tokenized securities, on-chain settlement systems, and hybrid TradFi-DeFi architectures.

The invisible monolith is growing taller, not narrower.

What happens if one Oracle is used everywhere?

Most major DeFi protocols rely on the same Chainlink price feeds. This means when something goes wrong, it does not affect just one app.

If a major ETH/USD or BTC/USD feed slows down, pauses, or reacts sharply to market stress, lending platforms, derivatives protocols, and stablecoin systems all respond at the same time. Liquidations trigger together, liquidity disappears together, and losses spread across the ecosystem almost instantly.

Backup systems often exist on paper, but switching oracles during live market chaos is risky and rarely tested. In practice, DeFi relies on one shared version of reality, even though execution happens on many different platforms.

What if Chainlink ever stops working properly?

This is hypothetical, but it shows how fragile the system can become.

If a major Chainlink price feed stopped updating and did not recover for several hours, DeFi lending platforms would not be able to liquidate risky loans. Bad debt would quietly build across multiple protocols. When the feed finally resumed, liquidations would happen all at once, potentially wiping out billions of dollars.

Another possible situation is when prices briefly move in strange ways because trading volume dries up. For example, Bitcoin could trade close to $20,000 on a few low-liquidity markets for a short period, even though the current price is much higher, above $90,000.

If that price is picked up by the oracle during that window, it will be treated as real. One update like that is enough to trigger mass liquidations across DeFi, even if the price recovers within minutes and returns to normal levels.

The same kind of risk exists with stablecoins. During periods of panic, USDT has traded around $0.95 on some markets. When that happens, DeFi protocols do not wait to see whether the price recovers. DeFi protocols see that price as the real one and react right away. Loans are automatically liquidated, trading positions are closed, and users end up losing money, even if USDT goes back to $1 later the same day.

In all these cases, the oracle works exactly as designed. The damage comes from the assumption that fast, automated reactions always produce fair outcomes.

Why nobody really talk about this risk

Chainlink works well most of the time, and that reliability makes its risks easy to ignore. Because major failures are rare, the oracle layer becomes invisible, even as more money depends on it.

Traditional finance expects markets to behave irrationally during stress, which is why it uses delays, manual intervention, and multiple independent price sources. DeFi prioritizes speed and automation, even during chaos.

Until DeFi treats oracle diversity and disagreement as necessary protections rather than inefficiencies, this dependency will remain one of the most underpriced risks in the entire system.

Conclusion: The cost of an invisible backbone

Chainlink is not failing. It is succeeding too well.

By becoming indispensable, it has transformed from a security solution into a single point of systemic risk. The problem is not malicious intent or technical incompetence. It is concentration—of trust, control, and dependency—in a system that claims to eliminate all three.

DeFi has built extraordinary applications. But beneath them lies an oracle layer whose success has quietly recreated the very fragilities the movement sought to escape. Until oracle redundancy is treated as a foundational requirement rather than an optional upgrade, the invisible monolith at the center of decentralized finance will remain its greatest unpriced risk.