Crypto cards have transformed digital assets from static investments into spendable money. By bridging the gap between blockchain wallets and traditional payment networks like Visa and Mastercard, these cards allow you to use Bitcoin (BTC), Ethereum (ETH), or stablecoins for everyday purchases—from buying groceries to booking flights.

This guide provides a detailed walkthrough of the crypto card landscape. We will explore how the technology works, the differences between regulated (KYC) and private (non-KYC) options, and specific risks associated with crypto card providers in the current market.

What is KYC — and why does it matter for crypto cards?

Before diving into the cards themselves, it helps to understand what KYC actually means and why it exists.

Definition

KYC stands for Know Your Customer. It is a regulatory requirement that obliges financial institutions — including crypto card issuers — to verify the identity of their customers before providing financial services. Typical KYC asks for a government-issued ID (passport, driving licence), a selfie, and proof of address.

KYC is mandated under AML (Anti-Money Laundering) legislation in most jurisdictions. The international framework that governs crypto specifically is the FATF Travel Rule — a Financial Action Task Force (FATF) standard requiring Virtual Asset Service Providers (VASPs) to share sender and receiver information for transactions above a threshold (typically $1,000 USD). This is why your crypto card issuer needs to know who you are: if you move money at scale, regulators require a paper trail.

For crypto cards, KYC determines everything from your spending limit to whether your card will still work next month. Non-KYC cards exist by operating in regulatory grey zones — but those grey zones can close overnight.

What are crypto cards?

At first glance, a crypto card looks exactly like the Visa or Mastercard provided payment card in your wallet. It has a chip, a magnetic stripe, and a CVV code. However, the “plumbing” behind the scenes is entirely different.

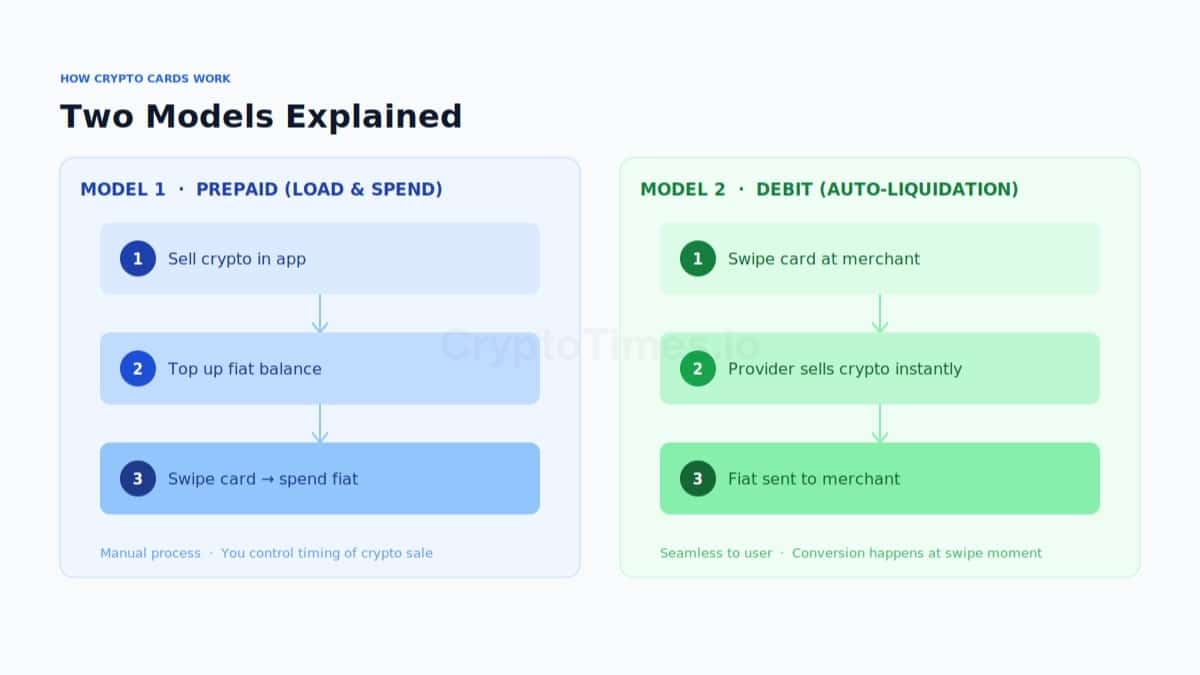

How Do Crypto Cards Work?

When you swipe a crypto card to buy a $5 latte, you aren’t actually sending Bitcoin to the coffee shop. The Visa/Mastercard network generally does not process crypto directly. Instead, one of two things happens:

- The prepaid (load-and-spend) model: You manually sell your crypto inside the card’s app to top up a fiat balance. When you swipe, you spend that fiat cash.

- The debit (auto-liquidation) model: The card is linked directly to your wallet. At the moment you swipe, the provider instantly sells the necessary crypto and sends fiat to the merchant. This feels seamless to the user.

Virtual vs physical cards — what is the difference?

A key decision point that many users miss is the format of the card itself.

- Physical cards (chip and PIN): Work at ATMs, in-store terminals, and online. They are shipped to your address — which means even “no-KYC” physical card issuers have your delivery address on file. ATM withdrawals are possible but usually carry a 1–3% withdrawal fee.

- Virtual cards (online only): Issued instantly, no shipping. Work for online purchases, subscriptions, and some digital wallets. Cannot be used at physical terminals or ATMs. Generally cheaper and faster to obtain.

Key takeaway

If you need to spend crypto in-store or at an ATM, you need a physical card. If you only shop online or want a fast setup, a virtual card is sufficient — and often safer, because there is no delivery address to expose.

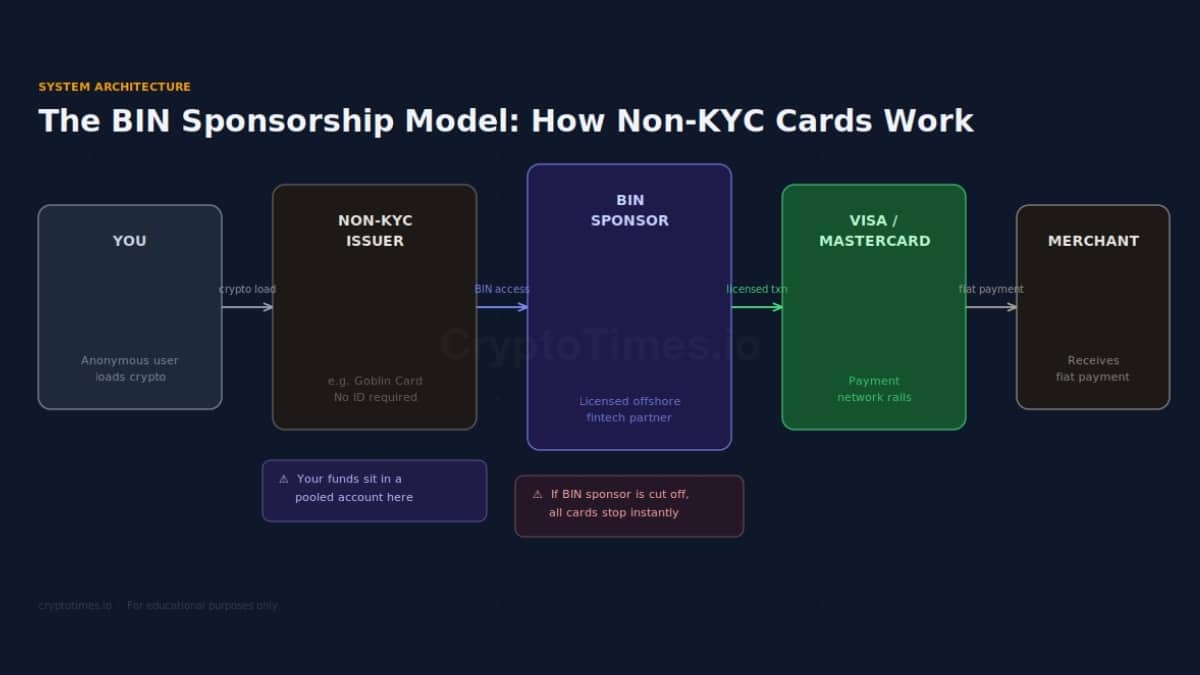

How non-KYC cards actually work

This is the concept most crypto card articles skip — and it explains almost everything about why non-KYC cards exist, why they are risky, and why they sometimes disappear.

Every Visa or Mastercard transaction flows through a BIN (Bank Identification Number). A BIN is a 6–8 digit code assigned to a licensed bank or financial institution. To issue a card, you must either be a licensed bank yourself or find a bank willing to sponsor your BIN — i.e., act as the regulatory front for your card programme.

Non-KYC card providers like Goblin Card are not banks. They are not licensed card issuers. What they do is operate as an “authorized user” or reseller on top of a BIN sponsor’s program — usually an offshore fintech. To the Visa network, the card belongs to the BIN sponsor. You are just an anonymous user on their corporate account.

This matters for three reasons:

- The BIN sponsor’s compliance failures are your problem. If the sponsor’s banking partner cuts them off (because of AML violations, chargebacks, or regulatory pressure), your card stops working — often with zero notice.

- Your money is not yours until you spend it. Funds loaded onto a non-KYC card sit in the BIN sponsor’s pooled account, not a segregated account in your name. If they go insolvent, your funds are unsecured creditor claims.

- The “no KYC” claim is partially true. The issuer does not know who you are — but the BIN sponsor’s banking partner does collect some data (the shipping address, the crypto wallet that funded the load). True anonymity is limited.

Warning

The 2018 WaveCrest shutdown is the canonical example of BIN risk. When Visa terminated WaveCrest's membership, hundreds of thousands of crypto cards across dozens of providers (including Cryptopay, Wirex, and others) stopped working overnight. Users lost immediate access to their loaded funds. The same risk exists today.

KYC crypto cards

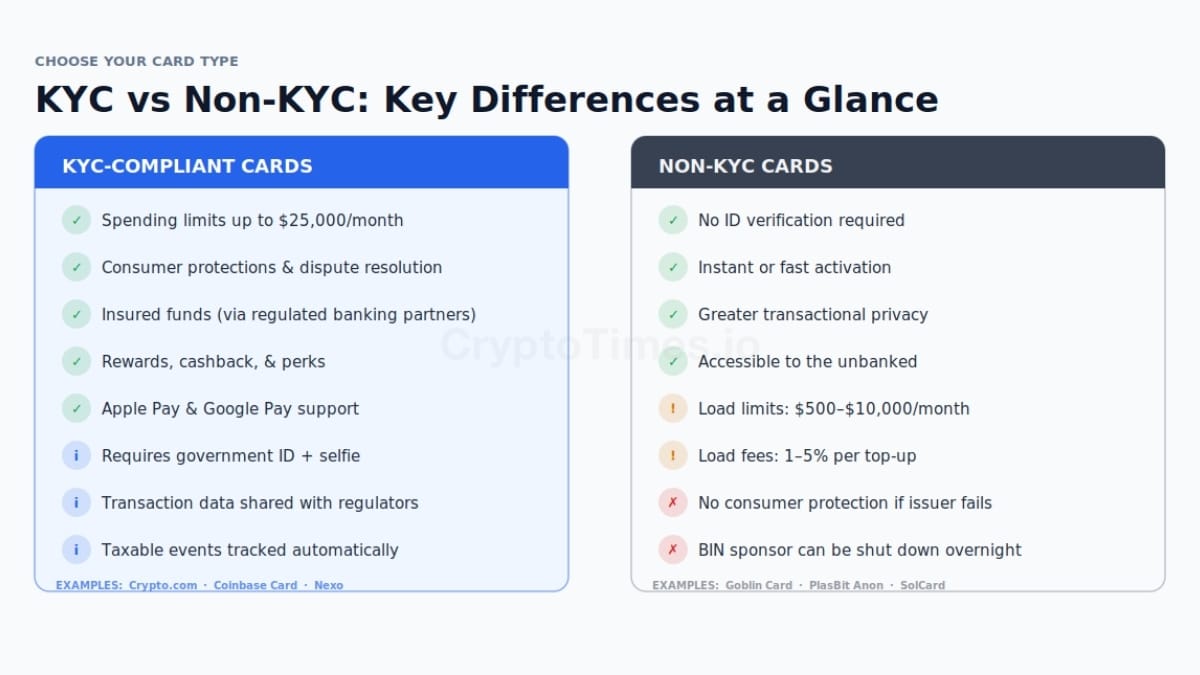

The vast majority of reliable crypto cards are KYC (Know Your Customer) compliant. This means you must upload a photo of your ID and a selfie to get one. Because these providers play by the rules, they can offer high spending limits and robust security.

1. Crypto.com Visa Card

Perhaps the most recognizable card in the industry, known for its heavy metal design.

- How it works: Crypto.com’s card is a prepaid card and you must have to top it up.

- The Hook: It offers tiered rewards based on how much of their native token CRO you stake (lock up). The higher the staking tiers, better the perks—such as free Spotify, Netflix, and airport lounge access.

- Risk: To get the best rewards, you must lock your tokens and invest significant capital (from $400 to $400,000) in the token. If token price crashes, your “free” Netflix subscription could cost you thousands in lost investment value.

- Apple Pay / Google Pay: Supported on all tiers.

2. Coinbase Card

- How it works: It is a debit card linked directly to your Coinbase balances.

- The Hook: It’s flexible as you don’t have to hold a specific token to use it. You can earn rewards (like 1% in Bitcoin or 4% in Stellar) on every purchase.

- Risk: While spending stablecoins (like USDC) comes free, spending volatile crypto (like BTC) usually incurs a “liquidation fee” or spread of around 2.49%

- Apple Pay / Google Pay: Supported.

3. Nexo Card

- The Innovation: Nexo’s crypto card is unique because it offers a “Credit Mode.” Instead of selling your crypto to pay for the coffee, Nexo uses your crypto as collateral and gives you a micro-loan for the purchase.

- Why it matters: Since you aren’t selling your crypto, you don’t trigger a taxable event (capital gains tax) at the moment of purchase.

- Spending limit: Up to $2 million credit line for high-collateral users.

- Apple Pay / Google Pay: Supported.

Non-KYC crypto cards

For users who want to keep their spending private, a niche market of Non-KYC (No Know Your Customer) cards has emerged. These cards do not require ID verification, and usual operate under regulatory loopholes or in offshore jurisdictions.

Warning

This sector is highly volatile. "No KYC" often means "No Consumer Protection."

1. Goblin Card — in-depth review

The Goblin Card is the most searched non-KYC crypto card in 2025–2026, having built a loyal following in “degen” (high-risk crypto trading) communities.

- How it works: Goblin Card operates as a corporate prepaid Visa via the BIN sponsorship model described above. To the banking network, the customer is Goblin’s corporate entity — not you. You are an authorized user on their program. The card is shipped physically to your address.

- Fees (2026): A one-time setup fee is charged in crypto (typically $15–$30 equivalent). Load fees range from 1% to 3% depending on the cryptocurrency used. FX markup on the exchange rate adds approximately 0.5–1% on top of the stated rate.

- Spending and load limits: Goblin Card’s advertised limits are approximately $5,000–$10,000 per month, though users report limits can be lower in practice for new accounts. There is no published lifetime load cap.

- Supported cryptocurrencies: Bitcoin (BTC), Ethereum (ETH), Tether (USDT), USDC, and several other major tokens. Loading via Lightning Network is supported for BTC, reducing confirmation times.

- Wallet compatibility: Google Pay support has been confirmed by users. Apple Pay compatibility is region-dependent — verify at signup for your country.

- Shipping: Ships to most countries globally. Delivery typically takes one to three weeks. Note that providing a delivery address means the issuer has your location on file, which partially negates the anonymity benefit.

- Regional availability: Available globally, with some exceptions for OFAC-sanctioned countries. Users in India have reported successful delivery, though local banking restrictions may affect some merchants.

Goblin Card risk summary

The primary risk is BIN sponsor instability. If Goblin's banking partner ends the program, all loaded funds are frozen and potentially inaccessible. Never keep more than your intended near-term spend on the card. As a rule of thumb: treat loaded funds as cash you are about to spend, not savings.

2. PlasBit (Anonymous Tier)

PlasBit markets itself as a privacy-first exchange and card provider with tiered KYC options.

- The Anonymous tier: Requires only an email address to activate. This tier is primarily a virtual card. The lifetime load cap on the Anonymous tier is approximately $500–$1,000 total (not monthly — lifetime). Once you have loaded this amount, you cannot load more without upgrading to a verified tier.

- Does PlasBit require KYC? The short answer is: yes, eventually. The Anonymous tier is best understood as a trial or low-volume option. To unlock meaningful spending, you must submit a government ID — at which point PlasBit becomes a standard KYC card with better privacy marketing than actual privacy.

- Verified tier limits: After submitting ID, monthly load limits increase to approximately $5,000–$10,000 depending on your verification level. A physical card is available at this tier.

- Fees: Monthly card fee of approximately $5 at the Anonymous tier. Load fees of 0.5–1%. There is a reported inactivity fee of approximately $3/month if the card is unused for 90 days.

- Best use case: Small, one-off private purchases where the lifetime $1,000 cap is sufficient. Unsuitable for recurring large spend.

3. Bitrefill (The gift card workaround)

Technically not a general-purpose payment card, Bitrefill allows you to live on crypto without KYC by selling closed-loop gift cards and virtual prepaid cards.

- Gift cards: Amazon, Uber, Airbnb, grocery stores, and hundreds of retailers. Purchase using Bitcoin, Lightning Network, Ethereum, or USDC. No account required, no KYC.

- Virtual Visa/Mastercard: Single-use, non-reloadable prepaid cards. These work for online shopping but carry strict region locks — a US Virtual Visa typically only works at US online merchants.

- Lifetime limits (2026): Bitrefill does not publish account-level limits, but individual virtual Visa cards are typically capped at $100–$500 per card. You can purchase multiple cards, but large-volume purchases may trigger verification.

- Safety: Generally safer than offshore debit cards because you self-custody your crypto until the exact moment you buy a specific card. There is no pooled account risk.

- Best use case: Online shopping at major retailers, particularly where a gift card directly serves the purpose. Poor substitute for a general debit card.

4. SolCard

A newer entrant focused on the Solana ecosystem, SolCard allows users to spend SOL and USDC directly.

- KYC status: No KYC at Tier 1. Higher tiers require ID verification and unlock higher limits.

- Load fee: 5% on all top-ups — the highest load fee of any card reviewed here.

- Spending limit: Approximately $1,000–$5,000 per month at the no-KYC tier.

- Physical or virtual: Physical card. Ships to select regions.

- Google / Apple Pay: Compatibility unconfirmed at time of writing — verify directly with SolCard.

- Risk: As a newer provider, the longevity of their banking partner is the main uncertainty. The 5% load fee means you start every transaction at a loss relative to spot price.

SolCard alternatives: Users searching for alternatives typically consider Goblin Card (lower fees, wider crypto support) or the Bitrefill method for online-only spending.

Full comparison: KYC vs non-KYC crypto cards

The table below summarizes all covered cards across key dimensions:

| Card | Network | Spend Limit | Key Fee | KYC Level |

|---|---|---|---|---|

| Crypto.com Visa | Visa | Up to $25,000/mo | 0–2.49% | Full KYC |

| Coinbase Card | Visa | Up to $25,000/mo | 2.49% liq | Full KYC |

| Nexo Card | Mastercard | Up to $2M credit | 0% (loan) | Full KYC |

| Goblin Card | Visa | ~$5,000–$10,000 | 1–3% | None |

| PlasBit (Anon) | Visa/MC | $500–$1,000 life. | 1–2% | Email only |

| SolCard | Visa | ~$1,000–$5,000 | 5% load | None (Tier 1) |

| Bitrefill VCC | Visa/MC | Per card (~$500) | 0–2% | None |

Non-KYC cards: virtual vs physical, Apple Pay, and load limits at a glance

| Card | Load Limit | Physical/Virtual | Apple/Google Pay | Shipping |

|---|---|---|---|---|

| Goblin Card | ~$5K–$10K/mo | Both | Google Pay ✓ | Worldwide |

| PlasBit (Anon) | $500–$1K lifetime | Virtual only | Limited | N/A (virtual) |

| SolCard | ~$1K–$5K/mo | Physical | Unconfirmed | Select regions |

| Bitrefill VCC | Per card (~$500) | Virtual only | ✗ | N/A (virtual) |

How to buy crypto with a debit or credit card without KYC

A large number of users arrive at this page wanting to know how to fund a no-KYC card in the first place — i.e., how to buy crypto without completing identity verification. Here is a practical overview of the main routes.

Important note

The availability and reliability of non-KYC purchasing methods changes frequently as regulators tighten requirements. Always verify the current status of any platform before sending funds.

Option 1: Peer-to-peer (P2P) exchanges

P2P platforms match buyers and sellers directly, with the exchange acting as escrow. Some platforms allow trading without full KYC up to certain limits.

- Examples: Bisq (fully decentralized, no KYC at all), LocalCoinSwap, Paxful.

- Method: Post a buy offer specifying payment by bank transfer or card. A seller accepts and you complete the trade via escrow.

- Risk: Counterparty risk — always use established sellers with high trade volume and positive reviews. Bisq requires Bitcoin for trading fees.

Option 2: Decentralised exchanges (DEXs) with on-ramps

DEXs like Uniswap and Jupiter do not hold custody and require no KYC. However, you need crypto to trade crypto — the challenge is the initial fiat-to-crypto conversion.

- Some DEX aggregators integrate with no-KYC fiat on-ramps (e.g., Transak, Ramp Network) for small amounts, often up to $150–$250 without ID.

- Method: Connect your wallet to a DEX, use an integrated fiat on-ramp for a small initial purchase, then expand from there.

Option 3: Bitcoin ATMs

Bitcoin ATMs allow cash-to-crypto conversion, often with no KYC for transactions below a threshold (commonly $200–$1,000 depending on the machine and local regulations).

- Higher fees than online options — typically 8–15% above spot price.

- Some machines now require a phone number (for OTP) even for small amounts, which partially identifies you.

- Use ATMMap or CoinATMRadar to find machines that allow cash purchases without ID.

Option 4: Pre-existing crypto holdings

If you already hold crypto in a self-custody wallet, you can load directly onto any of the cards covered in this guide without additional KYC. The “buying” step was already KYC-required whenever you first acquired the crypto.

- For Goblin Card: Send BTC, ETH, or USDT from any wallet to the card’s deposit address.

- For SolCard: Send SOL or USDC from a Solana wallet.

- For Bitrefill: Send from any compatible wallet directly at purchase.

The risks you must know

Before you move your funds to any crypto card, you need to understand three critical categories of risk.

1. The “Rug Pull” and regulatory shutdown risk

The banking system generally dislikes “no-KYC” crypto programs. If Visa or Mastercard detects that a provider is issuing cards to anonymous users in high-risk jurisdictions, they can (and do) shut the program down overnight.

- Historical example: In 2018, a major card issuer WaveCrest was shut down by Visa. Hundreds of thousands of crypto cards instantly stopped working, and users were left scrambling to get their funds back.

- Recent example (2024): The collapse of Synapse (a banking middleware provider) froze funds for thousands of users across various fintech apps. If your card provider uses a middleman that goes bankrupt, your money can be frozen for months, even if the crypto company itself is healthy.

- Mitigation: Never treat a crypto card as a savings account. Load only what you intend to spend in the immediate term.

2. The tax trap: “Spending is selling”

A common misconception is that using a crypto card helps avoid taxes. In the UK, the US, and most other jurisdictions, spending crypto is a taxable disposal event. When you buy a coffee with Bitcoin, you are legally selling that Bitcoin at the current price.

- Capital gains tax consequence: If BTC has appreciated since you acquired it, you owe capital gains tax on that coffee. Daily use of a crypto card can generate thousands of taxable micro-transactions per year.

- Stablecoin exception (partial): In some jurisdictions, spending USDC or USDT may not trigger a gain if the stablecoin maintained parity and you acquired it at $1.00. However, this varies by jurisdiction — users are advised to confirm with a tax professional.

- Nexo exception: Because Nexo’s Credit Mode does not involve selling, it avoids triggering a disposal event at the time of purchase. Interest payments are a different (and taxable) matter.

- Tax software: Tools such as Koinly, CoinTracker, and Crypto.com Tax can automatically import card transaction data and calculate your liability. Without this, manual reconciliation of thousands of transactions is extremely time-consuming.

3. The fee squeeze

Non-KYC cards are expensive. Because they operate in a legal gray area, they charge a premium.

- Load fees: You might pay 1% to 5% just to load crypto onto the card.

- FX spreads: The provider might claim “0% fees” but give you a Bitcoin exchange rate that is 2% worse than the market rate.

- Inactivity fees: Many of these cards charge monthly maintenance fees if you don’t use them regularly.

- ATM fees: Physical card withdrawals typically cost 1–3% plus any local ATM operator fees.

Regional availability

Crypto card availability varies significantly by country. Here is a summary of known restrictions for the major cards:

- India: Goblin Card ships to India and cards generally work at Visa-accepting merchants. However, international card spending is subject to India’s LRS (Liberalised Remittance Scheme) reporting rules — this applies even to crypto-funded cards.

- United Kingdom: Crypto.com, Coinbase Card, and Nexo all operate in the UK and are registered with the FCA. Non-KYC cards like Goblin Card technically ship to the UK, but financial promotions targeting UK residents without FCA registration are regulated under the Financial Promotion regime.

- United States: Coinbase Card is fully available. Crypto.com operates in most US states. Nexo is not available to US residents. Non-KYC cards like Goblin Card are in a legal grey area — the cards are issued offshore and may not be legal to use for US persons depending on interpretation.

- European Union: Post-MiCA (Markets in Crypto-Assets regulation, effective 2024), most EU-facing crypto card providers must be registered VASPs in at least one EU member state. Non-KYC cards from offshore issuers may violate MiCA’s AML provisions.

Also read: How to Analyze a Project’s Tokenomics: A Beginner’s Guide

Conclusion: Which card is right for you?

The best card depends entirely on what you value more: security and spending power, or privacy.

Choose a KYC-compliant card if you:

- Want to spend large amounts (over £1,000 or $1,000 per month).

- Want your funds protected by regulated entities or deposit insurance.

- Want rewards — cashback in crypto, subscriptions, or airport lounge access.

- Want to avoid the operational risks of BIN sponsor instability.

- Do not need to keep your identity private from your card provider.

Choose a non-KYC card if you:

- Are making small, private purchases and understand the risks.

- Are unbanked or unable to pass ID verification with mainstream providers.

- Already hold crypto in self-custody and want to spend it directly.

- Accept that funds on the card could be frozen at any time and are loading only “disposable” amounts.

Final advice

Never treat a crypto card as a savings account. The banking partners that power these cards — particularly non-KYC cards — are the weak link in the chain. Always keep your main holdings in a self-custody wallet (cold storage) and load only what you intend to spend in the near term. For non-KYC cards specifically, assume the card could stop working at any time and plan accordingly.

Frequently Asked Questions (FAQs)

Is the Goblin Crypto Card really no-KYC?

Yes, the Goblin Card currently operates without requiring users to submit identity verification (KYC). However, because it requires a shipping address for physical delivery, your anonymity is only partial. Furthermore, the card operates via a “BIN sponsorship” model, meaning its banking partner could enforce KYC or shut down the program if pressured by regulators.

Does PlasBit actually require KYC?

PlasBit markets an “Anonymous Tier” that only requires an email address, but it is heavily restricted. This tier acts as a virtual card with a strict lifetime load limit of $500–$1,000. To unlock meaningful monthly spending limits or get a physical card, PlasBit does require you to submit a government ID, making it a standard KYC card for high-volume users.

How can I buy crypto with a debit or prepaid card without KYC?

Buying crypto with a traditional debit or prepaid card without KYC is increasingly difficult due to global anti-money laundering (AML) laws. However, some decentralized exchange (DEX) aggregators integrate with fiat on-ramps (like Transak or Ramp) that allow small purchases (typically $150–$250) without full ID verification. Peer-to-peer (P2P) platforms like Bisq are another option, though you trade directly with other users rather than using a standard card gateway.

Are virtual non-KYC crypto cards safer than physical ones?

From a privacy standpoint, virtual cards are generally safer. Physical cards require a shipping address, which means the issuer has your physical location on file. Virtual cards can often be generated instantly with just an email address and a crypto deposit. However, virtual cards cannot be used at physical ATMs or in-store terminals that do not accept Apple Pay or Google Pay.

Do I still have to pay taxes if I use a non-KYC crypto card?

Yes. A common misconception is that “no KYC” means “tax-free.” In most jurisdictions (like the US and the UK), spending cryptocurrency is considered a taxable disposal event. Even if the card provider doesn’t know your identity, the legal obligation to report capital gains remains on you. Blockchain forensics can also link non-KYC wallet funding back to regulated exchanges.

What happens to my funds if a non-KYC card provider gets shut down?

If the card issuer’s banking partner terminates the program due to compliance failures, your card will stop working instantly. Because non-KYC funds are usually held in a pooled corporate account rather than in your name, you become an unsecured creditor and could lose access to your loaded funds. You should only load what you intend to spend immediately.

How do new global regulations affect no-KYC crypto cards?

Regulatory frameworks like the EU’s Markets in Crypto-Assets (MiCA) and the FATF Travel Rule are aggressively closing the loopholes that allow non-KYC cards to exist. As these regulations take effect globally, the offshore banking partners that power non-KYC cards face immense pressure to either enforce identity verification or shut down entirely.

Disclaimer: All information provided is for educational purposes only and should not be considered financial or investment advice. The cryptocurrency market is high-risk, and we strongly encourage you to conduct your own research (DYOR) before making any decisions. We do not endorse specific assets or strategies and are not liable for any losses incurred.