The Hyperliquid Policy Center (HPC) and Phantom Technologies filed a joint comment letter with the Commodity Futures Trading Commission (CFTC) on Thursday, urging the regulator to formally recognize that publishing onchain protocol software does not trigger registration, that non-custodial wallets do not act as financial intermediaries, and that existing CFTC registrants should be given a clear path to run regulated functions on onchain infrastructure.

The letter, addressed to CFTC Secretary Christopher Kirkpatrick, responds to the Commission’s Request for Information (RIN 3038-ZA24), published in the Federal Register on June 18, 2026. The RFI was issued under Executive Order 14405 and seeks to identify regulations that unduly impede fintech firms from partnering with CFTC-regulated markets and intermediaries. The filing was announced by HPC on X.

The Three Demands

The joint letter lays out a three-pronged roadmap for the Commission.

First, HPC and Phantom want the CFTC to confirm that developing or contributing to onchain protocol software, standing alone and without ongoing control over its use, does not trigger registration as a designated contract market (DCM), swap execution facility (SEF), derivatives clearing organization (DCO), futures commission merchant (FCM), introducing broker (IB), or swap dealer under the Commodity Exchange Act.

The filing argues that software running on a public blockchain has no legal personality, cannot enter into contracts, and presents none of the risks registration was designed to address, such as mishandling of customer orders or misuse of customer funds.

The letter notes that under prior CFTC leadership, developers were left guessing whether they could be treated as operating an unregistered exchange or clearinghouse, pushing many to build offshore. The filing credits current Chairman Selig’s leadership with working to reverse that trend.

Second, the two firms are asking for guidance allowing existing CFTC registrants to perform their regulated functions using onchain infrastructure. The letter argues that the Phantom and Hyperliquid stack demonstrates that execution, access intermediation, and clearing and settlement can all be performed onchain in ways that satisfy, and in some cases exceed, the CEA’s core principles.

Specific asks include confirmation that a DCM can use an onchain protocol as its matching and execution layer, that a DCO can use onchain protocols for margining, settlement, and default management, and that an FCM can accept customer orders and funds onchain.

The filing flags three problem areas where legacy rules assume custodial, proprietary systems: system safeguards, segregation rules, and recordkeeping requirements. On recordkeeping, the letter cites the President’s Working Group’s July 2025 recommendation that the CFTC allow blockchain technology to satisfy obligations under Regulation 1.31, arguing public blockchains natively deliver the immutability and verifiability the old WORM standard was designed for.

Third, the firms want the CFTC to codify the March 17, 2026 Phantom no-action letter (CFTC Letter No. 26-09) into a formal rulemaking. That letter relieved Phantom from IB registration because its role is limited to providing technical means of access. A rulemaking would extend that treatment to every similarly situated firm, giving the industry durable certainty instead of forcing companies to seek relief one at a time. The filing also asks that codification allow fintech firms to partner with the full range of CFTC registrant categories, including co-marketing and revenue-sharing arrangements that help subsidize software costs for users.

Structural Divide at the Heart of the Filing

The core argument of the comment letter is structural. The CFTC’s rulebook was built for a layered, custodial market where a broker takes the order, an exchange matches it, and a clearinghouse settles it, with intermediaries controlling customer funds at every step.

Onchain markets flip that model, letting users hold their own funds and trade peer-to-peer under rules written in code. The letter frames self-custody as a feature, not a bug, arguing that intermediation itself introduces risks like front-running and lost or stolen funds.

The filing draws a parallel to the offchain world, where software developers routinely build matching engines, order routing algorithms, and risk engines for regulated firms without themselves triggering registration. HPC and Phantom argue the same distinction should carry over to onchain markets, with registration touching persons who use onchain protocols to perform regulated functions rather than the protocols themselves.

The filing discloses that Phantom already integrates Hyperliquid on its interface, though that functionality remains unavailable to U.S. users today. A favorable CFTC response could open the door for American retail traders to access onchain derivatives markets like Hyperliquid through regulated channels for the first time.

HYPE Price Action

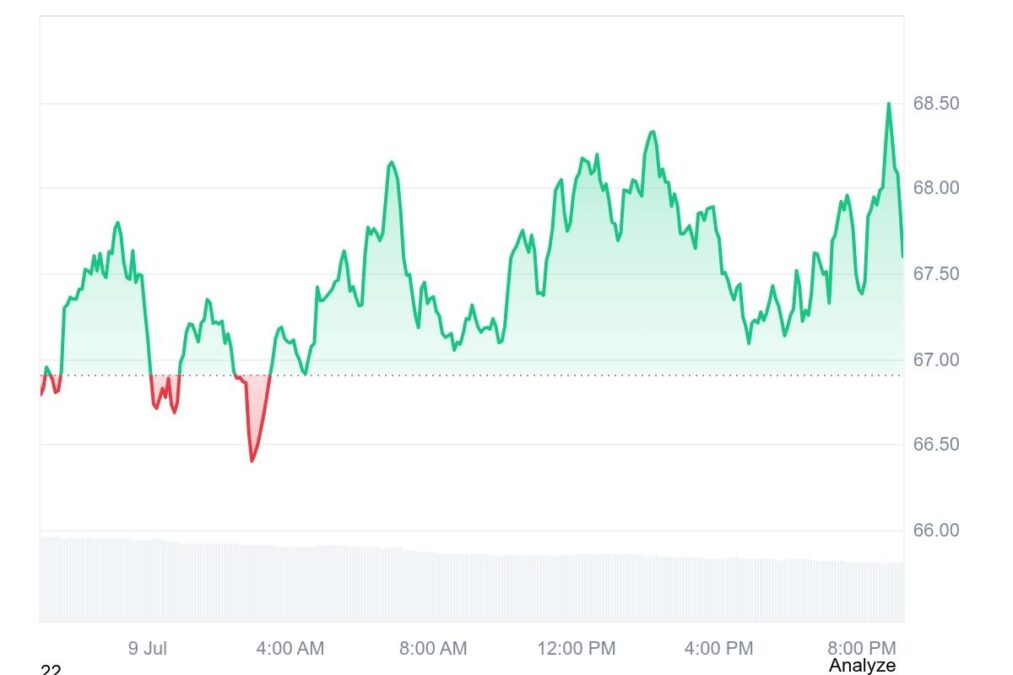

HYPE showed a muted immediate reaction to the news. The token is trading around $67.50, up roughly 0.9% over the past 24 hours, with 24-hour trading volume near $355 million and a market cap of about $17 billion, ranking ninth by market capitalization.

HYPE remains up about 6% over the past seven days, outperforming the broader crypto market, and sits roughly 16% below its all-time high of $76.65 set on June 16, 2026.

Analysts will be watching whether regulatory clarity momentum can push the token back toward price discovery, given that U.S. market access remains the single largest untapped catalyst for the Hyperliquid ecosystem. Hyperliquid recently hit a record 8.3% share of aggregate perpetual futures open interest versus centralized exchanges, and any pathway for U.S. users would directly expand that addressable market.

The CFTC asked which of its rules stand in the way of fintech innovation. HPC and Phantom say this filing is their answer, and they argue everything requested is within the Commission’s own authority to act on.

Also Read: Bitwise 10 Crypto Index ETF (BITW) Adds HYPE, Removes DOT and AVAX