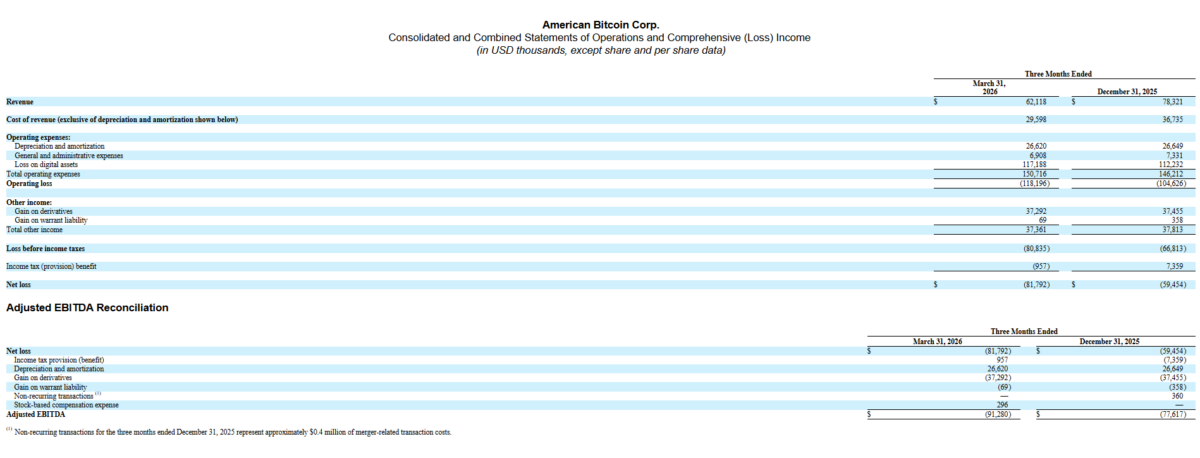

American Bitcoin Corp. (Nasdaq: ABTC) on Wednesday reported a first-quarter net loss of $81.8 million, its widest quarterly deficit since going public last year.

The red ink, detailed in a Form 8-K filing with the U.S. Securities and Exchange Commission (SEC), came despite the miner posting record Bitcoin production and growing its treasury holdings by more than 1,600 coins.

For a company whose brand is inseparable from Eric Trump’s name, the numbers arrived at a delicate moment. Its shares remain down more than 90% from post-listing highs, and fresh scrutiny over dilution, governance and the Trump family’s role continues to shadow its progress.

Operational strength amid accounting losses

The loss itself was no surprise to anyone following Bitcoin’s price action. American Bitcoin booked a $117.2 million non-cash charge on its digital-asset holdings after the cryptocurrency fell roughly 22% during the quarter.

The firm’s revenue from mining slipped to $62.1 million from $78.3 million in the fourth quarter, even though the firm mined a record 817 BTC.

Chief Executive Mike Ho tried to put the best face on it. “Excluding the mark-to-market accounting noise, our core mining business generated positive operating income,” he said in the release.

The firm’s gross mining margin held steady above 50%, and the all-in cost to mine each Bitcoin improved 23% to roughly $36,200.

Operationally, the company is firing on all cylinders. It added another 3.05 exahashes per second of capacity in March, bringing its fleet to 89,242 miners and 28.1 EH/s. It bought 803 BTC for its treasury without selling a single coin.

By March 31 it held 7,021 BTC, making it the 16th-largest public holder of the asset. Eric Trump, the co-founder and chief strategy officer, highlighted the “sats-per-share” metric—up about 20 percent to roughly 663—calling it proof that the company is “compounding Bitcoin at a discount to spot while scaling efficiently.”

Yet those numbers have done little to quiet critics who argue the story is more complicated—and far less flattering to retail shareholders.

Dilution, branding, and growing investor skepticism

A Forbes investigation published in April laid out the case in stark terms. Between the September 2025 Nasdaq debut and early 2026, ABTC’s market value briefly pushed Eric Trump’s paper stake into billionaire territory. The stock then collapsed.

Reports estimate retail investors lost roughly $500 million in market value as the shares cratered from above $9 to around $1.25.

The Forbes piece portrayed the company as something closer to an arbitrage machine: issue shares at lofty valuations fueled by Trump-family branding, use the cash to buy Bitcoin, then watch dilution erode the upside promised to new buyers. Eric Trump’s personal net worth reportedly climbed from about $190 million to $280 million even as the stock cratered.

Expectedly, the company pushed back hard against claims. In statements and social-media posts, executives labeled the Forbes story “Chinese propaganda” and a politically motivated hit job. They pointed to the balance sheet: no Bitcoin sales, growing hash rate, and a treasury that keeps expanding.

“We are not in the business of timing the market; we are in the business of owning more of it,” Eric Trump said in one interview. Still, the dilution was real.

The company issued millions of new shares through private placements and other financings to fund both miner purchases and Bitcoin acquisitions. Existing shareholders watched their ownership stakes shrink.

Accompanying this, a bigger long-term risk has also surfaced: American Bitcoin pledged 3,090 BTC—roughly 44% of its current holdings and far more than the estimated 1,800 BTC it has mined in its entire history—as collateral for a $330 million mining equipment financing deal.

Under the put option structure, the company has until around August 2027 to repay the amount in cash or forfeit the pledged Bitcoin. If Bitcoin does not rally sufficiently by then, critics warn the firm could lose a large portion of its treasury in a single settlement—a scenario some outlets have dubbed a “$330 million time bomb.”

Read: American Bitcoin’s $330M Countdown: How Eric Trump’s Latest Venture Could Lose Every BTC by 2027

Governance questions have compounded the unease. Public filings show ABTC operates with a remarkably lean head count, relying heavily on its former parent, Hut 8 Mining, for infrastructure, executive support, and back-office functions.

Hut 8 retains roughly 80% of the voting power through a special class of shares. Critics describe the setup as an “asset-light” model that looks more like a licensing or branding deal than a traditional operator.

Related-party ties and Eric Trump’s past regulatory history have also drawn attention. Separately, Eric Trump recently slammed a Financial Times report linking him and his brother to a U.S.-backed tungsten mining project in Kazakhstan involving up to $1.6 billion in federal support. He insisted he is only a passive investor with no management role, calling suggestions of active involvement “inaccurate and defamatory.”

Executive overlaps between ABTC and Hut 8, combined with the Trump family’s retained 20 percent economic interest in the spun-out mining assets, have raised eyebrows among governance watchdogs.

A separate Senate inquiry earlier this year examined potential token transfers involving sanctioned entities across the broader crypto sector. While not focused solely on American Bitcoin, the probe added to the political heat surrounding any high-profile Trump-linked venture in digital assets.

To be sure, ABTC is hardly alone in its struggles. Nearly every public Bitcoin miner posted mark-to-market losses in the first quarter. Many have leaned on equity raises to fund expansion in a capital-intensive business.

What sets American Bitcoin apart is the speed of its listing, the intensity of the Trump branding, the aggressive use of pledged collateral, and the sheer velocity of the boom-and-bust cycle that followed. Investors who bought the narrative of a pure-play miner with White House-adjacent leadership have so far been left holding depreciated paper.

The company continues to execute on its stated plan: grow hash rate, hoard Bitcoin, and wait for the next bull cycle. Whether that strategy ultimately rewards patient shareholders—or simply transfers value from late-stage buyers to insiders while exposing the treasury to major 2027 risks—remains the central debate.

As of Thursday morning, ABTC shares were little changed in early trading, hovering near $1.25. Bitcoin itself has stabilized near $81,000, offering some breathing room heading into the second quarter.

But with another round of share unlocks looming, the collateral cliff approaching in 2027, and the political spotlight still bright, American Bitcoin’s next set of numbers will be watched as closely for operational progress as for how the company navigates its growing list of controversies.

Also read: Bitcoin’s $81K Breakout: Why the Vanishing Tail-Risk Premium Feels Different in 2026