Tens of billions of dollars flow through cryptocurrency exchanges every single day. Giants like Binance, Coinbase, and Kraken process a volume of transactions that rivals the stock exchanges of small countries. But how do these digital marketplaces actually make their money? It’s easy to assume it’s all from that small fee on your trade, but the reality is far more complex and fascinating.

Cryptocurrency exchanges are not just simple platforms; they are sophisticated financial technology companies. Their business models have evolved to include a diverse, and sometimes hidden, array of revenue streams that go far beyond basic trading.

This article dissects the machinery of these crypto powerhouses. We will explore the primary engine of trading fees, uncover other direct charges, delve into advanced financial services, and reveal the crucial differences between how centralized and decentralized exchanges turn a profit.

The Primary Engine: Trading Fees

At the heart of every exchange’s business model lies the trading fee. This is the most consistent, reliable, and significant source of income for the vast majority of platforms.

Every time a user buys or sells a cryptocurrency, the exchange takes a small percentage of the transaction’s value. While this fee may seem minuscule on a single trade, multiplying it by millions of trades and billions of dollars in daily volume results in a staggering revenue stream. To manage this process and incentivize market activity, most exchanges use a “Maker-Taker” model.

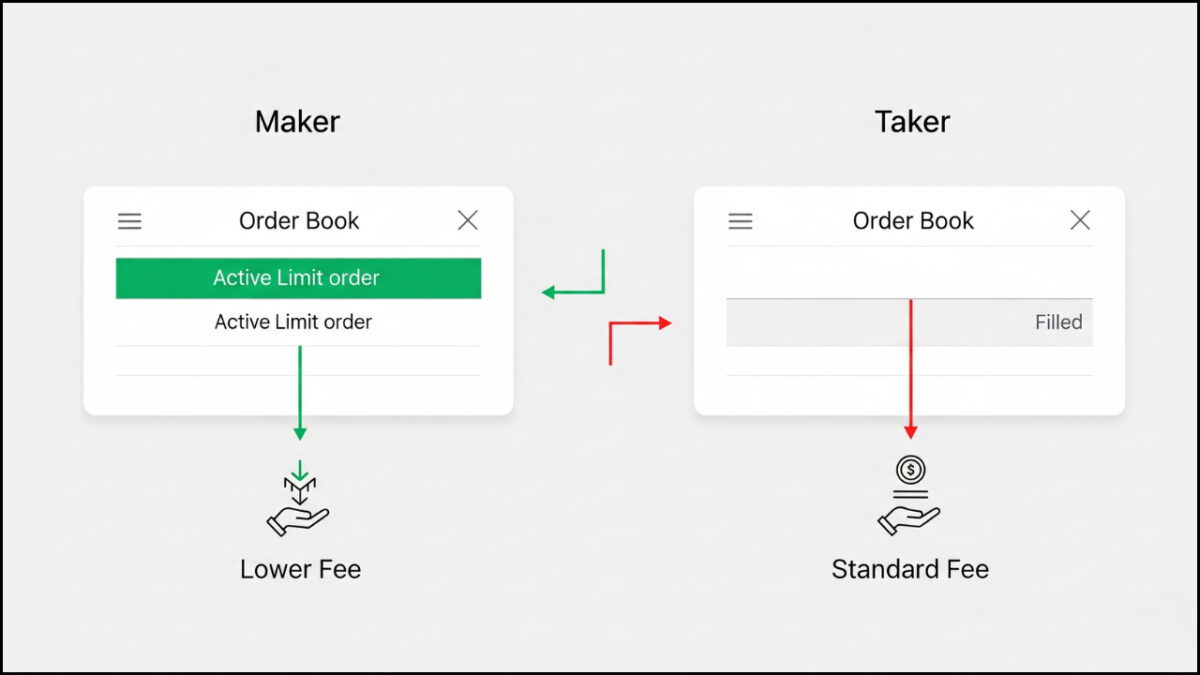

The Maker-Taker Model

This model is designed to create liquidity: the ease with which an asset can be bought or sold without affecting its price. It works by charging different fees to two types of traders:

- The “Maker”: A maker is a trader who adds liquidity to the market by placing an order (e.g., a limit order) that doesn’t get filled instantly. This order sits on the exchange’s “order book,” waiting for another trader to match it. Because they provide the liquidity that others need, exchanges reward them with lower fees.

- The “Taker”: A taker is a trader who removes liquidity from the market by placing an order (e.g., a market order) that is filled immediately. They are “taking” the liquidity that the maker provided. Because they consume this valuable liquidity, they are typically charged a slightly higher fee.

Tiered Fee Structures

To further encourage trading activity, exchanges implement tiered fee structures that reward high-volume traders. The more you trade, the lower your fees become. Additionally, many exchanges offer extra discounts to users who hold and use the exchange’s native utility token. For example, Binance offers a 25% discount on trading fees to users who pay their fees using BNB.

Here’s a look at the standard fee structures for some of the top exchanges:

(Note: These are standard fees and can be lower with higher trading volumes and native token holdings.)

Beyond the Trade: Other Direct User Fees

While trading fees are the main course, exchanges serve up a variety of other fees that add up to a significant portion of their revenue.

- Withdrawal Fees: When you move your cryptocurrency from an exchange to an external wallet, the exchange charges a withdrawal fee. This fee covers the network transaction fee (or “gas fee”) and includes a small premium for the exchange.

- Fiat On-Ramp & Off-Ramp Fees: The process of converting traditional money into crypto (on-ramp) and vice-versa (off-ramp) is a key revenue source. While bank transfers can be cheap or free, using a credit or debit card to buy crypto often comes with fees in the 3-5% range to cover processing costs and fraud protection.

The Gatekeepers: Listing Fees & IEOs

- For a new cryptocurrency project, getting listed on a major exchange is a make-or-break moment. Exchanges leverage this by charging significant listing fees, which can range from tens of thousands to over a million dollars.

- Another lucrative model is the Initial Exchange Offering (IEO). In an IEO, an exchange acts as a launchpad for a new project’s token sale. The exchange vets the project, lends its reputation, and provides access to its user base. In return, the exchange takes a percentage of the funds raised and often receives an allocation of the new tokens.

The “Crypto Bank”: Financial Services & Yield Generation

Modern exchanges have expanded into a suite of financial products, generating revenue from users’ idle assets.

- Staking Services: Exchanges offer “Staking-as-a-Service,” simplifying the process of earning rewards on Proof-of-Stake (PoS) cryptocurrencies. For this convenience, they take a commission, typically between 10% and 25%, of the staking rewards.

- Lending & Borrowing: Exchanges operate as crypto banks, paying users interest on their deposited assets and then lending those assets to other users at a higher rate. The exchange’s profit is the spread between these two rates.

- Derivatives, Futures, and Leveraged Trading: This is one of the most profitable areas for major exchanges. The trading volume in the crypto derivatives market often dwarfs the spot market. Exchanges collect fees on these trades and also profit from liquidations, where they seize a trader’s collateral when a leveraged position goes against them.

The Hidden & Institutional Game

Beyond the retail-facing services, exchanges have several other revenue streams:

- The Bid-Ask Spread: The small difference between the buying (“bid”) and selling (“ask”) price of a crypto asset is the bid-ask spread. Exchanges can capture this spread as a near risk-free profit on market orders.

- Custody Solutions: For institutional investors, exchanges offer secure, insured storage for their crypto holdings. Services like Coinbase Custody charge a management fee for this.

- Venture Capital (VC) Arms: Major exchanges have their own VC divisions, like Binance Labs and Coinbase Ventures, which invest in promising blockchain startups, creating a revenue stream completely separate from their platform operations.

Emerging Revenue Streams: The Future of Exchange Profitability

The most forward-thinking exchanges are already diversifying their revenue streams further:

- Layer-2 Solutions and BaaS: Exchanges are building their own blockchain ecosystems, like the BNB Smart Chain and Coinbase’s Base. They earn transaction fees from the activity on these networks.

- Maximal Extractable Value (MEV): A more complex revenue stream, MEV involves capitalizing on the ability to reorder or insert transactions in a block to capture arbitrage opportunities.

- Crypto-Backed Cards: By offering debit and credit cards, exchanges are tapping into the traditional payments industry, earning interchange fees on every transaction.

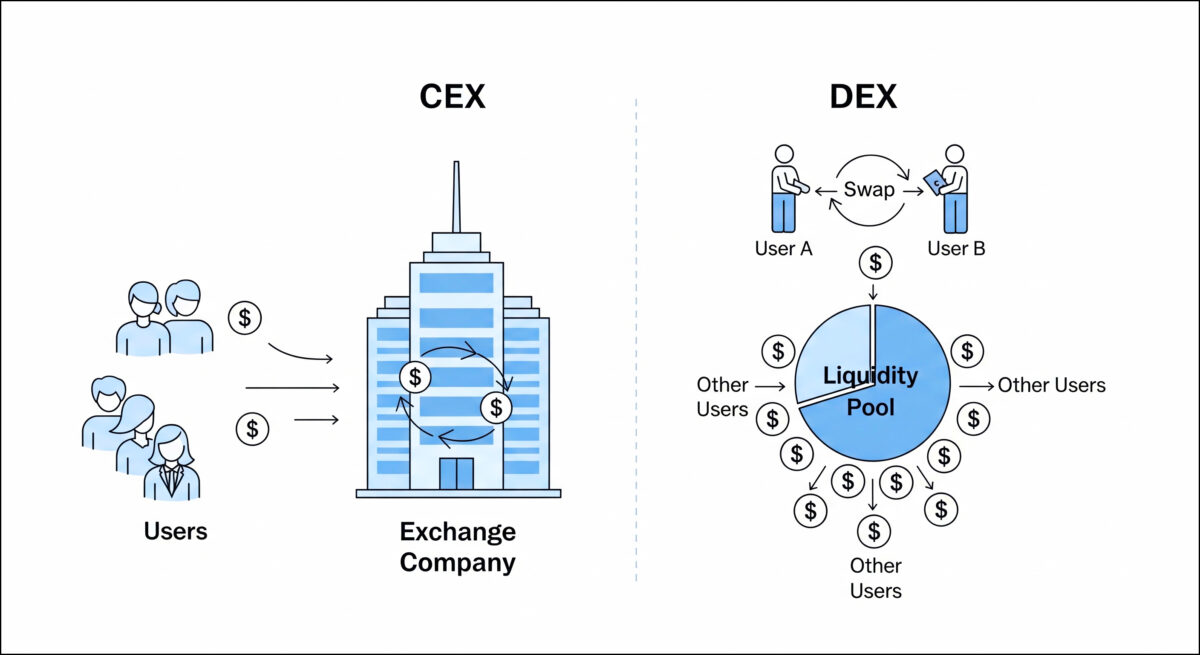

A Tale of Two Models: CEX vs. DEX Revenue

It’s crucial to distinguish between the two main types of exchanges, as their business models are fundamentally different.

- Centralized Exchanges (CEX): These are the platforms we’ve primarily discussed, like Binance, Coinbase, and Kraken. They are private companies that operate the platform, hold customer funds, and run the order book. All the revenue streams mentioned above, such as trading fees, listing fees, lending spreads, etc., flow directly to the corporation as profit.

- Decentralized Exchanges (DEX): Platforms like Uniswap, Sushiswap, and Curve operate without a central authority. They are protocols built on smart contracts that allow users to trade directly from their own wallets using “liquidity pools.” Their revenue model is different. A DEX typically charges a small, fixed fee on every swap (e.g., Uniswap’s standard 0.3% fee). However, this fee does not go to a company. Instead, it is paid out directly to the liquidity providers, the users who deposited their own tokens into the liquidity pool to enable the trades. The “profit” for the DEX protocol itself is indirect, often coming from the value appreciation and utility of its native governance token, which gives holders a say in the protocol’s future.

Also Read: CEX vs. DEX: How DeFi Trading is Beating Binance, Coinbase?

How to Minimize Your Crypto Trading Fees

As a trader, you can use your understanding of these revenue models to your advantage:

- Be a Maker, Not a Taker: Use limit orders instead of market orders to get lower fees.

- Leverage Native Tokens: If you trade frequently on a particular exchange, consider using their native token to pay for fees.

- Monitor Withdrawal Fees: Before making a withdrawal, check the current network fees to avoid overpaying.

- Avoid Credit/Debit Card Purchases: If possible, use bank transfers to on-ramp your fiat currency.

While traders can take steps to minimize explicit fees, it’s also crucial to be aware of the more opaque ways that exchanges can profit.

Conflicts of Interest: The Less-Transparent Ways Exchanges Profit

Beyond the publicly listed fees and services, a significant and controversial portion of an exchange’s revenue can be generated through methods that are opaque and sometimes predatory. These practices often stem from a fundamental conflict of interest: the entity running the market is also an active participant in it. For users, understanding these risks is just as important as understanding the fee schedule.

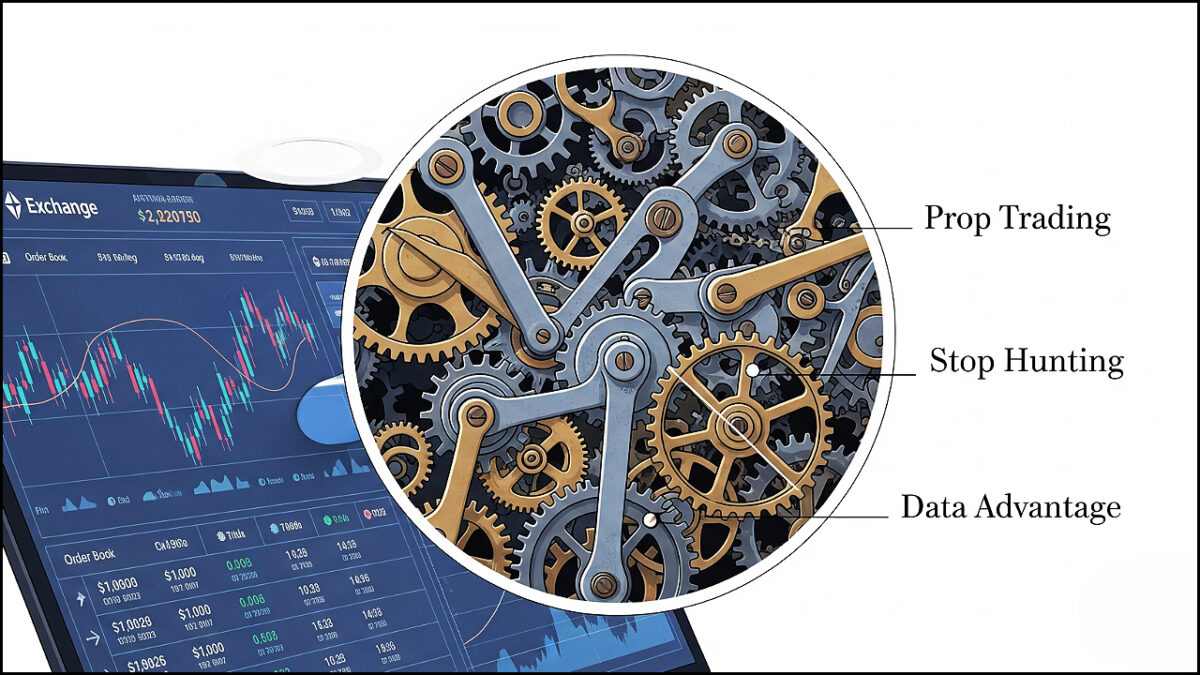

The Exchange as an Active Market Participant

Many exchanges operate their own proprietary trading desks, moving beyond the neutral role of a simple platform and creating an almost unbeatable advantage.

- Proprietary Trading: The exchange trades for its own direct profit using its own capital. With access to unparalleled data on user positions and order flows, this desk has a significant edge over every other trader on the platform.

- Market Making for Profit: While essential for liquidity, an exchange’s own market-making desk can strategically set wide bid-ask spreads, especially on volatile assets, to maximize its own profit from the difference between the buying and selling price.

Leveraging a “God’s View” of Market Data

Exchanges have a complete, real-time view of every trade, order, stop-loss, and liquidation level on their platform. This “God’s view” can be monetized in several ways.

- Trading Against Customers: This is a serious allegation where an exchange’s prop desk may trade against the aggregate sentiment of its users. If they see an overwhelming number of leveraged long positions, they can take a massive short position, knowing exactly where the clusters of liquidation prices are. A small, engineered price dip can then trigger a cascade of liquidations, transferring wealth directly from users to the exchange.

- Front-Running: An exchange can see a large order coming into the order book and have its own desk place a trade moments before to capitalize on the price movement, securing a risk-free profit.

- “Stop Hunting”: Knowing exactly where users have placed their stop-loss orders, an exchange’s desk can potentially execute trades designed to push the price just enough to trigger these stops, creating volatility and liquidity from which they can profit. The infamous and sudden “scam wicks” on price charts are often attributed to this practice.

Outright Market Manipulation

In a largely unregulated global market, some platforms may engage in activities that would be illegal in traditional finance to create a misleading appearance of activity.

- Wash Trading: This is where an exchange creates fake volume by simultaneously buying and selling the same asset through accounts it controls. This makes an asset appear to have high liquidity, luring in real traders and helping the exchange climb rankings on data aggregator sites.

- Spoofing and Layering: This involves placing large orders on the books with no intention of executing them. These “spoof” orders trick other participants into reacting to false market pressure. The manipulator then cancels their large orders and trades against the reaction they created.

The Lucrative and Controversial Listing Game

While listing fees are a known revenue stream, the ecosystem around them creates further conflicts of interest.

- Exorbitant Fees & Token Allocations: Projects often pay massive fees or provide the exchange with a large allocation of their tokens (e.g., 1-5% of the total supply). This creates an incentive for the exchange to list any project that can pay, regardless of its quality, and then promote it to its user base to maximize profit from its own token holdings.

Other Hidden Revenue Streams

- Profit from Liquidations: On derivatives platforms, when a user’s position is liquidated, there are often substantial fees. Furthermore, the exchange’s liquidation engine takes over the user’s position, and the process of unwinding it is often a black box designed to be highly profitable for the exchange.

- Yield on Customer Funds: Exchanges hold billions in user assets. They can stake or lend these assets out to earn yield, often passing on only a fraction of these earnings (if any) to the actual owners of the funds, similar to how a traditional bank operates.

Conclusion

Cryptocurrency exchanges are far more than simple digital brokers. They have evolved from basic trading platforms into multifaceted fintech giants with highly diversified and incredibly lucrative business models.

While trading fees remain their core engine, their profits are bolstered by a sophisticated array of services, including fiat gateways, high-stakes listing deals, banking-style lending and staking, and massive-scale derivatives markets. They also play the long game through institutional custody and venture capital investments.

Understanding these intricate revenue streams is not just a matter of curiosity; it is essential to grasping the power dynamics and financial infrastructure that underpin the entire cryptocurrency market.

Sources & Citations Links

1. On Proprietary Trading & Conflicts of Interest

- Source: “How Sam Bankman-Fried’s Crypto Empire Collapsed” – The New York Times

- Source: “Crypto exchanges’ ‘conflict of interest’ in the spotlight after FTX’s collapse” – CNBC

2. On Leveraging Market Data (Trading Against Customers, Front-Running, Stop Hunting)

- Source: “Exclusive: FTX’s Bankman-Fried secretly moved 10 bln in customer funds to Alameda” – Reuters

- Source: “What Is Front-Running in Crypto and How to Avoid It” – CoinDesk

3. On Outright Market Manipulation (Wash Trading, Spoofing)

- Source: “Crypto Wash Trading” (Working Paper) – National Bureau of Economic Research (NBER)

- Source: “More Than Half Of All Bitcoin Trades Are Fake” – Forbes

4. On the “Pay-to-Play” Listing Ecosystem

- Source: “The Real Cost of Listing a Token on a Crypto Exchange” – CoinDesk

- Source: “Crypto’s ‘Pay-to-Play’ Listing Fees” – The Defiant

5. On Other Hidden Revenue Streams (Liquidations, Yield on Customer Funds)

- Source: “How Do Liquidations Work in Crypto?” – Bybit Learn

- Source: “How Crypto Lenders and Exchanges Are Using Your Deposits” – Bloomberg

Disclaimer: Some elements of this content may have been enhanced with the help of our artificial intelligence (AI) assistants for purposes such as basic refinement, review, image generation, and translation to deliver high-quality content in a shorter time frame. However, all AI-assisted content is reviewed and approved by our team to ensure accuracy, fairness, clarity, and editorial integrity.