Key Highlights

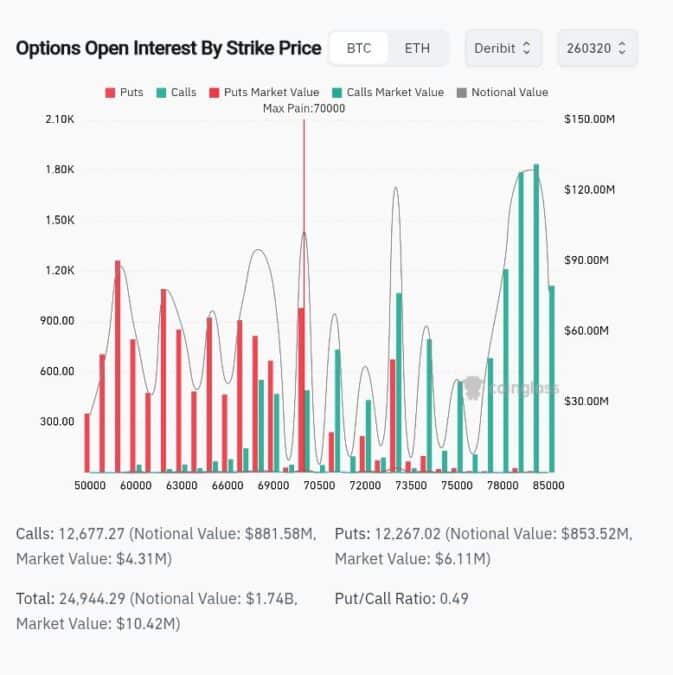

- Bitcoin dropped to $70,000, landing exactly at the max pain strike for the March 20 Deribit options expiry the level where option sellers inflict maximum loss on buyers.

- Over $541 million in crypto futures were liquidated in 24 hours across 141,810 traders, with longs making up 82% ($443.84M) of the total wipeout.

- Put options carry higher market value ($5.80M) than calls ($4.50M) despite a 0.49 put/call ratio, while funding rates for BTC, ETH, SOL, and BNB have all turned negative — confirming broad defensive positioning.

Bitcoin dropped to around $70,000 on Thursday, down 1.6% since midnight UTC, and landed directly at the max pain level for Deribit’s March 20 options expiry.

Max pain is the price at which the combined value of all outstanding puts and calls expires worthless, inflicting maximum loss on option buyers. With BTC now sitting right at that $70,000 strike, the options market is effectively acting as a gravitational pin on price, and is likely to keep BTC range-bound between $69,000–$71,000 until the contracts settle.

Total open interest across the expiry stands at 24,838 contracts worth $1.72 billion in notional value — a significant enough size to influence short-term price behavior.

Puts Cost More Than Calls

While the put/call ratio by contract count sits at 0.49, meaning roughly twice as many calls as puts the market value tells a different story. Puts carry $5.80 million in market value versus $4.50 million for calls, indicating traders are paying a premium for downside protection.

Heavy call open interest clusters at the $76,000–$80,000 strikes, but these are far out-of-the-money and function more as a resistance ceiling than a realistic near-term target. On the put side, significant positioning stretches all the way down to $50,000, reflecting hedges against a deeper correction.

On Deribit, put skews have strengthened for both BTC and ETH, while block flows show outsized demand for ether straddles and BTC put spreads and risk reversals — all classic defensive plays.

Volmex’s BVIV, measuring bitcoin’s 30-day implied volatility, has jumped over 5% to 58.36%, reversing a week-long decline. Rising implied vol alongside falling spot price is a bearish combination.

$541M Liquidation Wipeout — Longs Destroyed

CoinGlass data confirms the damage. Over the past 24 hours, 141,810 traders were liquidated for a combined $541.62 million. Longs accounted for $443.84 million i.e 82%, while shorts made up just $97.78 million.

Bitcoin led at $191 million in liquidations, followed by Ether at $165.39 million. The largest single liquidation was a $17.97 million ETHUSDT position on the Aster exchange.

The time-window breakdown reveals how the pain escalated: Liquidations in the one-hour window were relatively balanced at $18.49 million, suggesting the most aggressive forced selling had already passed. But the four-hour and 12-hour windows were heavily long-biased, at $126.50 million and $300.74 million respectively, showing leveraged bulls were caught offside as the market moved lower.

Industry-wide, futures open interest has fallen 5.6% to $106.90 billion. Ether futures OI dropped 9% alongside a 6% spot price decline — a combination that signals active capital outflows, not just price depreciation.

Funding rates for BTC, ETH, BNB, and SOL have all turned negative, confirming that bearish short positioning is back in demand.

Altcoins Bleed on Thin Liquidity

Altcoins underperformed sharply. Bittensor (TAO) and Hyperliquid (HYPE) dropped 8.8% and 6.5%, respectively, while the CoinGlass heatmap showed red across SUI, ZEC, WLD, and others.

The altcoin weakness is structural—thin liquidity persists in a market still recovering from a $19 billion leverage wipeout in October. A handful of tokens bucked the trend: NEO rose 4.2%, and restaking token ETHFI added 1.5% to $0.55.

What Happens After Expiry?

With BTC pinned at max pain, price is likely to remain compressed through Friday’s settlement. The real question is what happens after the pin releases.

The macro backdrop remains hostile — soaring oil prices from Iran-Gulf escalation and a hawkish Fed that held rates at 3.50%–3.75% on Wednesday are keeping risk appetite suppressed. But the derivatives picture is what matters most right now: negative funding, falling OI, rising implied vol, and put-heavy options flow all tilt risk to the downside once the expiry gravitational pull fades.

Traders are watching $69,000 as immediate support. A break below could open the door toward $65,000. A reclaim of $73,000–$74,000 would be needed to shift sentiment.

Santiment data showed wallets holding between 10 and 10,000 BTC shifted from net selling to net buying over the previous two weeks, even as U.S. spot Bitcoin ETFs posted $129.62 million in net outflows on March 18 following a seven-session inflow streak of nearly $967 million.

Also Read: Bitcoin Rainbow Chart Flashes ‘Fire Sale’: Analysts Eye $150K–$440K Rally