In March 2023, the digital asset industry faced a reckoning that had nothing to do with blockchain technology and everything to do with the archaic plumbing of traditional banking. Circle, the issuer of the second-largest stablecoin USD Coin (USDC), revealed that $3.3 billion of its reserves were trapped in Silicon Valley Bank (SVB) as the institution collapsed.

For years, the promise of stablecoins was simple: a digital token worth exactly $1.00, backed by cash in a bank. But when the bank doors closed for the weekend, that promise faltered. USDC temporarily lost its peg, trading below $0.90. The crisis exposed a fatal flaw in “Generation 2” stablecoins: while they move at the speed of the internet (24/7), their collateral is stuck in the 9-to-5 banking world. Furthermore, in a high-interest-rate environment, leaving billions in zero-yield bank deposits became not just risky, but economically inefficient.

We are now witnessing the rise of Generation 3 Stablecoins: instruments backed not by idle cash, but by Tokenized U.S. Treasuries Real-World Assets (RWAs) brought on-chain. This shift is fundamentally rewiring the financial ecosystem, merging the “risk-free” stability of U.S. government debt with the programmable speed of DeFi. It represents the end of “lazy money” and the beginning of a new era where the dollar in your digital wallet doesn’t just sit there it works.

The Evolution of Trust: From “Trust Me” to “Verify Me”

To understand where we are going, we must look at how trust has evolved in the stablecoin market, which now sits at $300 billion in valuation, as per DeFillama data.

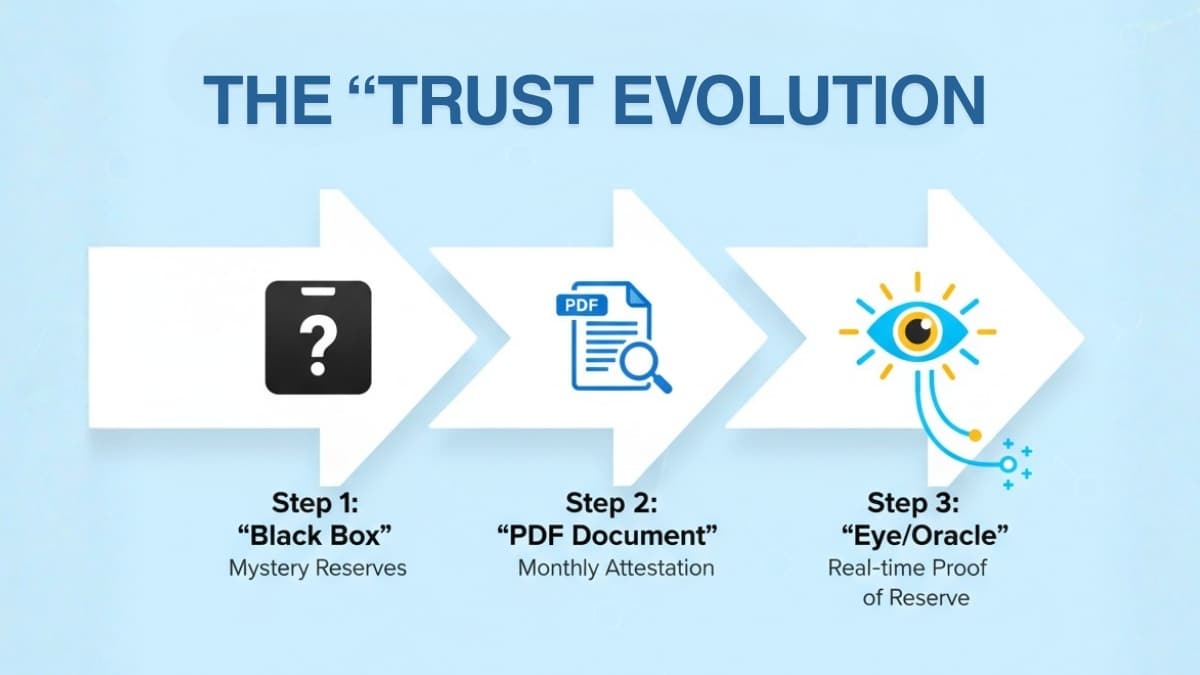

Gen 1 & 2: The Black Box and the PDF

The first generation of stablecoins, epitomized by early Tether (USDT), operated as a black box. Users had to trust that the issuer held sufficient assets, which ranged from cash to commercial paper and secured loans.

The second generation, led by Circle’s USDC, introduced the “Attestation Model.” They promised transparency by hiring major accounting firms to verify their bank accounts once a month. While an improvement, this method suffers from a critical “trust gap.” An attestation is a PDF report that captures a snapshot in time. It tells you what money was in the bank on the last day of the month, but it cannot tell you what is there today. As the SVB crisis proved, a lot can happen between snapshots.

Gen 3: The RWA Revolution and Proof of Reserve

The third generation solves this by moving the asset itself on-chain. Tokenized Treasuries are digital representations of U.S. government debt (T-Bills) recorded on a blockchain.

This technological leap replaces the monthly PDF with Proof of Reserve (PoR). Using decentralized “Oracles”—middleware provided by networks like Chainlink or Chronicle—protocols can now verify off-chain collateral in real-time.

Here is how the new architecture works:

- Custody: A regulated custodian (like BNY Mellon) holds the physical T-Bills.

- Verification: An Oracle network queries the custodian’s API to verify the balance.

- Enforcement: The Oracle publishes this data on the blockchain. If the value of the collateral drops below the value of the tokens issued, the smart contract can automatically trigger a “circuit breaker,” pausing minting or redemptions to prevent a bank run.

This shifts the paradigm from “Trust, then verify” to “Verify, then trust.”

The Yield Dilemma: A Tale of Two Jurisdictions

If Tokenized Treasuries are safer and more transparent, why doesn’t every stablecoin pay you interest? The technology exists, but the regulations create a massive divide.

The Economic Problem

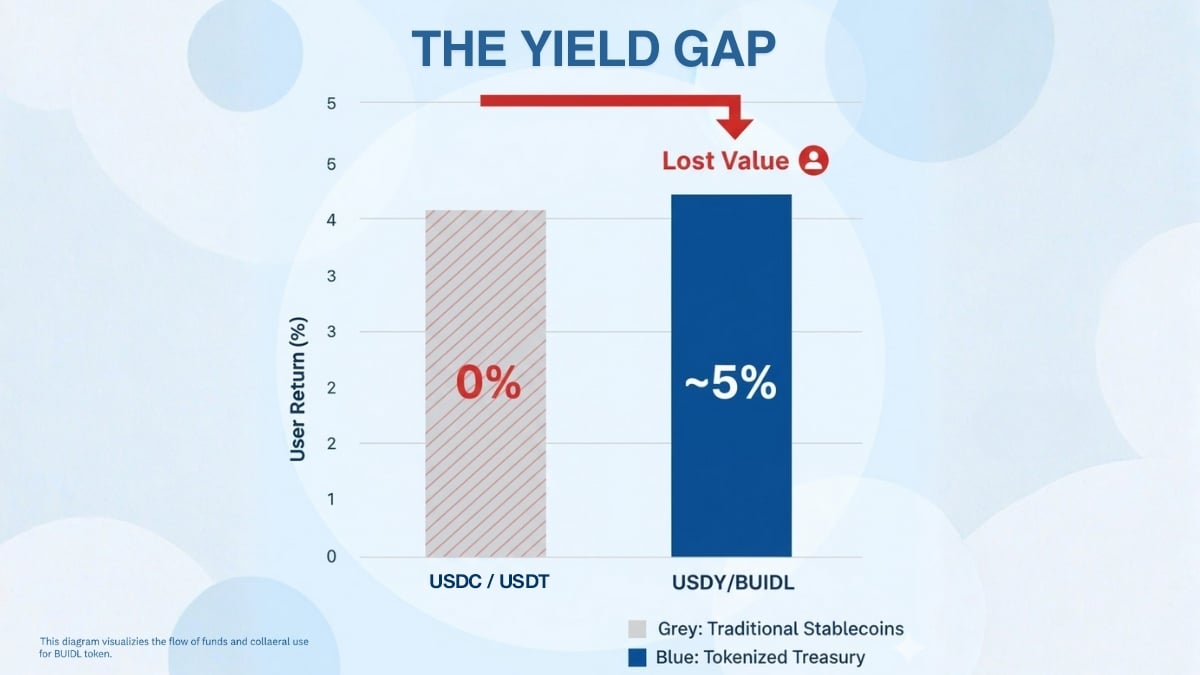

In the current economic climate, U.S. Treasury bills yield approximately 5% annually. Traditional stablecoin issuers like Tether and Circle essentially run a business model where they take your dollars, invest them in T-Bills, and keep 100% of the interest. For the user, holding a non-yielding stablecoin is akin to giving an interest-free loan to a corporation.

The Regulatory Moat: The GENIUS Act and MiCA

Governments are acutely aware of this dynamic. In the United States, the GENIUS Act (Guiding and Establishing National Innovation for U.S. Stablecoins) established a framework for “payment stablecoins.” Crucially, it explicitly prohibits issuers of payment stablecoins from paying interest or yield to holders. The logic is to protect the banking sector; if a digital dollar paid 5% interest and was as liquid as cash, users might pull their deposits from traditional banks, destabilizing the system.

Europe has taken a similar stance with MiCA (Markets in Crypto-Assets). The regulation bans “e-money tokens” (fiat-backed stablecoins) from granting interest. This regulatory pressure has forced Coinbase to delist non-compliant stablecoins in the EU.

The Offshore Solution

This regulatory blockade has created a bifurcated market. While U.S. and EU users are pushed toward 0% yield “payment” coins, innovative protocols are launching offshore to offer yield-bearing products to the rest of the world.

- Mountain Protocol (USDM): Regulated by the Bermuda Monetary Authority, Mountain Protocol issues USDM, a stablecoin backed by U.S. Treasuries. It uses a “rebasing” mechanism where the token balance in your wallet increases daily to reflect the accrued interest (currently ~5%). It effectively passes the risk-free rate directly to the user, democratizing access to U.S. debt yields for non-U.S. residents.

- Ondo Finance (USDY): Ondo offers a tokenized note secured by U.S. Treasuries. Unlike a rebasing token, USDY is an accumulation token—its value appreciates over time rather than increasing the number of tokens you hold.

Anatomy of the New Market: Key Players and Architectures

The market for tokenized Treasuries has exploded, growing over 500% in 2024 alone to reach nearly $9 billion. This growth is driven by three distinct categories of players: Institutional Titans, DeFi Integrators, and Federated Protocols.

1. The Institutional Titan: BlackRock’s BUIDL

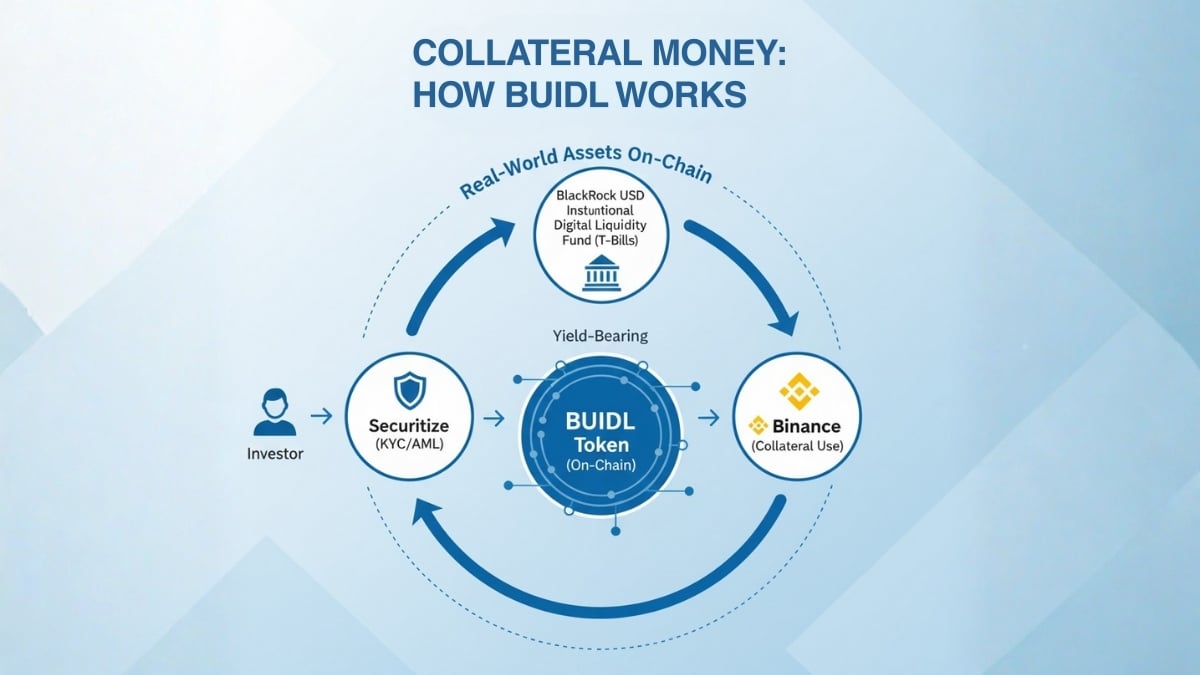

The entry of BlackRock, the world’s largest asset manager, legitimized the industry overnight. Their BlackRock USD Institutional Digital Liquidity Fund (BUIDL) is the heavyweight champion of this sector, capturing over 40% of the market share within months of launch.

- The Structure: BUIDL is a tokenized money market fund built on Ethereum. It maintains a $1.00 peg and pays daily accrued yield monthly.

- The Innovation: The true breakthrough is its integration with the “crypto plumbing.” In late 2025, Binance, the world’s largest crypto exchange, listed BUIDL as acceptable off-exchange collateral. This allows institutional traders to keep their capital in a yield-bearing, bankruptcy-remote asset (BUIDL) while using it to trade derivatives. Previously, traders had to sit in 0% USDT or USDC. This shift maximizes capital efficiency on a scale previously impossible in crypto.

- The Gatekeeper: Unlike permissionless stablecoins, BUIDL uses “whitelisted” wallets managed by Securitize, ensuring strict compliance with KYC/AML laws and preventing unauthorized transfers.

2. The DeFi Integrators: Ondo Finance & Ethena

While BlackRock caters to institutions, DeFi protocols are wrapping these assets for the broader market.

- Ondo Finance (OUSG/USDY): Ondo acts as a bridge. Its OUSG token invests directly in BlackRock’s BUIDL fund but packages it for on-chain use. By doing so, it allows DeFi users to access institutional-grade assets that would otherwise require a $5 million minimum investment.

- Ethena (USDe) – The “Synthetic” Alternative: It is vital to distinguish Tokenized Treasuries from “Synthetic Dollars” like Ethena’s USDe. Ethena does not primarily rely on holding T-bills. Instead, it generates yield through a “delta-neutral basis trade”—shorting crypto futures while holding the spot asset to capture funding rates. While Ethena has begun integrating BlackRock’s BUIDL to add stability, its core model carries different risks (derivative counterparty risk) compared to the pure government debt backing of a standard RWA stablecoin.

3. The “Singleness of Money” Solution: M^0 Protocol

A new entrant, M^0, is attempting to solve the fragmentation of the stablecoin market. Currently, stablecoins are silos; USDC is issued by Circle, USDT by Tether.

M^0 introduces a “Federated Minting” model. It allows multiple institutions to mint a single, fungible token ($M) backed by U.S. Treasuries.

- How it works: An institution locks T-bills in a custodian. The Chronicle Oracle verifies this collateral on-chain. The protocol then allows that institution to mint $M.

- The Goal: This recreates the “correspondent banking” network on the blockchain. Just as a dollar at Chase is treated the same as a dollar at Wells Fargo, M^0 aims to make a digital dollar minted by Institution A fungible with one minted by Institution B, all verified by independent, decentralized oracles.

The New Risk Matrix: It’s Not Risk-Free

While Tokenized Treasuries solve the “uninsured bank deposit” risk that toppled SVB, they introduce a new, complex set of vulnerabilities. Investors must understand that “on-chain” does not mean “risk-free.”

Custodial Centralization: The Physical Link

The most persistent myth in RWA tokenization is decentralization. In reality, the T-Bill must live somewhere physical. It is held by a custodian like BNY Mellon or State Street.

If the custodian freezes the assets due to a court order, or if the legal Special Purpose Vehicle (SPV) holding the assets is mismanaged, the on-chain token becomes a “paper claim” with no value. As industry guides note, “if the gold vault burns down, the token doesn’t mean much”. You are not trusting code alone; you are trusting a chain of legal contracts and human custodians.

Smart Contract & Oracle Risk

RWA stablecoins rely on complex code to manage minting, rebasing, and yield distribution. A bug in the smart contract could prevent users from redeeming their tokens or allow hackers to mint unbacked tokens. Furthermore, if the Oracle (the data feed) is manipulated to report false collateral data, the system could become insolvent before human intervention is possible.

The Liquidity Mismatch (T+1 vs. T+0)

Blockchains operate 24/7/365 (T+0 settlement). The U.S. Treasury market operates Monday to Friday and settles in T+1 (one business day).

This creates a dangerous mismatch. If a panic occurs on a Saturday night, token holders may rush to redeem their RWA stablecoins. The issuer cannot instantly sell the T-bills to honor these redemptions until the markets open on Monday. To mitigate this, issuers must maintain a “liquidity buffer” of cash, which reintroduces the very banking risk they sought to avoid.

Regulatory Classification

The regulatory ground is shifting beneath our feet. While the GENIUS Act attempts to clarify the landscape, there is still a constant risk that yield-bearing tokens could be reclassified as “unregistered securities” by the SEC. If this happens, trading could be halted, and liquidity pools on decentralized exchanges (DEXs) could be forced to delist the assets, trapping user funds.

Conclusion: The Convergence

We are witnessing the inevitable convergence of two financial worlds. The “Generation 3” stablecoin is not just a crypto asset; it is a financial hybrid that colonizes the safety of traditional finance with the efficiency of blockchain technology.

The days of stablecoin issuers keeping 100% of the yield are numbered. The market is waking up to the fact that in a 5% interest world, idle money is losing money. As we move forward, the concept of “digital cash” will likely split into two distinct buckets:

- Transactional Money (e.g., USDC, PayPal USD): Zero-yield, highly liquid, regulatory-compliant instruments used for payments and merchant settlement.

- Collateral Money (e.g., BUIDL, USDY): Yield-bearing, Treasury-backed instruments used for savings, corporate treasury management, and DeFi collateral.

BlackRock’s entry and the rise of protocols like M^0 confirm that the future of finance isn’t about replacing the dollar; it’s about upgrading it. By backing the next generation of stablecoins with transparent, yield-bearing Treasuries, the industry is finally building the “financial plumbing” required for a truly digital global economy.