In the high-stakes arena of corporate Bitcoin strategy, few doctrines have been as ironclad as Michael Saylor’s “never sell.”

For more than five years, Strategy Inc.—the company formerly known as MicroStrategy and now the undisputed king of on-balance-sheet BTC holdings—built its identity, its stock narrative, and its $64 billion-plus Bitcoin treasury on the simple promise: buy, hold, and let the asset appreciate. This vow cracked wide open on May 5, 2026.

During the company’s first-quarter earnings call, Saylor, Strategy’s founder and executive chairman, dropped a line that sent ripples through crypto markets and traditional finance alike: “We will probably sell some Bitcoin to pay a dividend just to inoculate the market and send the message that we did it.”

Saylor framed the move not as surrender but as sophisticated engineering: “You buy Bitcoin with credit, you let it appreciate, and then you sell Bitcoin to pay the dividend.”

The timing was no coincidence. Strategy had just posted a staggering $12.54 billion net loss for Q1—as mentioned in the report—driven almost entirely by a $14.46 billion unrealized fair-value hit on its digital assets as Bitcoin prices softened early in the year.

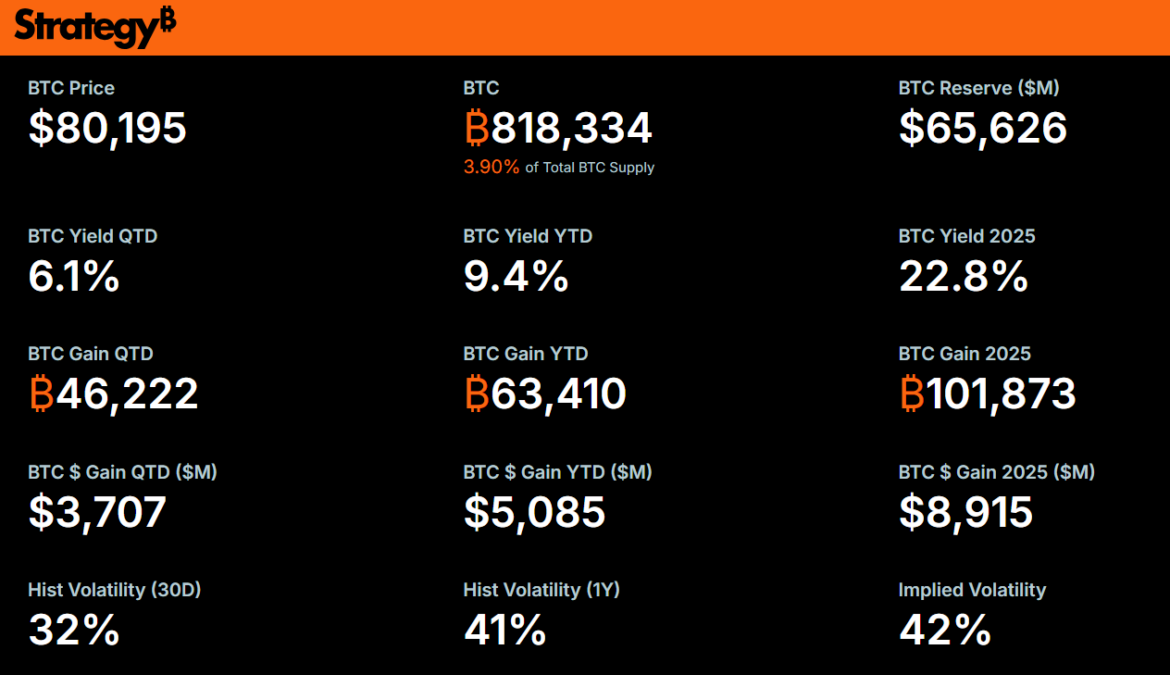

Yet the company’s actual Bitcoin hoard stood at a record 818,334 BTC—roughly 3.9% of all Bitcoin that will ever exist—as of May 8, with a blended acquisition cost of about $75,537 per coin.

The end of the pure HODL era?

Strategy’s Bitcoin journey began in 2020 as a bold hedge against fiat debasement. What started as opportunistic purchases ballooned into a full-blown treasury strategy that turned the business-intelligence software firm into a leveraged Bitcoin proxy.

By late 2025, the company had rebranded to Strategy to reflect its new reality: Bitcoin was no longer a side bet; it was the main event.

Central to the model was the 2025 launch of STRC—“Stretch”—a perpetual preferred stock engineered as high-yield digital credit. Backed by the Bitcoin balance sheet, STRC pays a variable cash dividend, currently fixed at 11.5% annualized. It has scaled explosively to roughly $8.5 billion in notional value, making it the world’s largest preferred stock by market cap in under a year.

The instrument has funded tens of thousands of additional BTC purchases throughout years while delivering steady income to holders ranging from retail investors to DeFi protocols and even other corporate treasuries.

But its success bred obligations. The company’s annual dividend and interest payments on preferred equity and related instruments now run about $1.5 billion. Its cash reserves cover roughly 18 months of those payouts, and the full Bitcoin stack—valued near $64 billion at the time of the call—would theoretically provide 43 years of coverage even if the price never budged.

Still, the growing dividend load created a structural tension: how do you keep raising capital, servicing credit-like instruments, and avoiding excessive dilution of common shares without touching the crown jewel?

A new playbook: net aggregator, not passive holder

Saylor and CEO Phong Le spent much of the earnings call sketching a more active balance-sheet philosophy. The goal, they stressed, remains “net aggregation” of Bitcoin—growing the total stack while, more importantly, increasing Bitcoin per share (BPS), a metric the company has long promoted to equity investors.

Sales, if they occur, would be surgical: likely higher-cost-basis coins to harvest tax losses (the firm sits on roughly $2.2 billion in realizable tax credits from unrealized impairments) or to fund obligations in a way that proves accretive rather than dilutive.

Le was blunt: “We’re not going to sit back and just say, ‘We’ll never sell the bitcoin.’ We want to be net aggregators of bitcoin—increasing our total bitcoin, but more importantly, increasing our bitcoin per share.” Saylor likened the company to a real-estate developer who occasionally sells a parcel to unlock value elsewhere.

In one illustrative scenario, the firm could hold a modest USD reserve and service all obligations purely through modest Bitcoin sales—driving an even higher BTC yield for shareholders without tapping equity markets at all.

The “inoculation” comment was classic Saylor theater—acknowledging that the mere idea of a sale would rattle purists and short sellers, so why not get the first small transaction on the record and demonstrate that the sky does not fall?

A hypothetical $100 million Bitcoin sale, he noted, would represent a negligible fraction of the treasury and might even be net positive for the broader Bitcoin network by adding liquidity and proving institutional flexibility.

Market reaction: jitters, the reflection

Following the announcement, Strategy shares (MSTR) dropped more than 4% in after-hours trading on May 5, while Bitcoin briefly dipped below $81,000. The move fueled a brief wave of commentary: some hailed it as pragmatic maturity; others saw it as the first crack in the armor that had made Strategy the poster child for corporate Bitcoin adoption.

However, the shift does not alter the core thesis—Strategy remains overwhelmingly long Bitcoin and continues to outpace spot ETFs in net accumulation via its capital-structure alchemy. Yet it reframes the company less as a pure “Bitcoin ETF with software attached” and more as a dynamic Bitcoin development firm that can flex between issuance, appreciation, and selective realization.

Short sellers who bet on inevitable dilution to fund dividends now face a counter-narrative: the firm can service its credit without flooding the market with new MSTR shares.

At the time of publishing, MSTR was priced at $179.84, giving the company a market cap of $63.114 billion. While BTC was trading near $80,255—putting Strategy’s Bitcoin reserve valued at $65.67 billion.

What it means for the corporate Bitcoin playbook

The announcement arrives at a pivotal moment as Strategy’s success has inspired dozens of smaller firms and even pushed some sovereign entities to explore Bitcoin reserves. Its pivot signals that even the most committed treasury strategy must eventually confront real-world cash-flow mechanics once preferred obligations scale into the billions.

The math still favors the bulls: at current BTC appreciation rates, the treasury grows faster than the dividend drain. But the rhetorical bridge from “never sell” to “strategic offloading” forces every Bitcoin treasury manager to ask the same question: when does disciplined management become compromise?

Saylor himself has not wavered on the long-term conviction. As shown on the company’s official website, its KPIs—BTC Yield (9.4% year-to-date), BTC Gain (63,410 coins added), and BPS growth—remain the scoreboard.

No sales have been executed as of this writing, and the press release itself stayed silent on the topic, focusing instead on capital raised ($11.68 billion year-to-date) and the proposal to shift STRC dividends to semi-monthly payments for better liquidity and price stability.

Yet the message is unmistakable. Strategy is no longer content to be a static vault. It wants to be an active steward—buying aggressively when markets allow, engineering yield-bearing instruments like STRC, and, when accretive, trimming the smallest slice necessary to keep the machine humming. In Saylor’s words, it creates “more optionality and second- and third-order effects” for equity holders.

This evolution’s impact on Strategy’s Bitcoin-maximalist roots will face its first real tests in the coming months. The shareholder vote on dividend frequency looms as an early indicator, followed closely by any announcement of the company’s inaugural modest sale.

For now, the world’s largest corporate Bitcoin holder has signaled it is ready to evolve. The era of absolute HODL is over. The age of calculated, dividend-aware offloading has begun.