Since 2008, the crypto sector has seen extraordinary growth in usage and technology. With the increasing demand for blockchain-based currencies, central governments came up with an idea to introduce their own digital currencies based on blockchain technology. Central Bank Digital Currency (CBDC) is a virtual form of a nation’s fiat money.

Let us understand what CBDC is and how much beneficial is it to us.

What is CBDC?

CBDC is a centralized currency that is issued and regulated by the country’s competent monetary authority. The present concept of CBDC came into existence due to Bitcoin blockchain technology. Governments around the world are experimenting with and are comparatively successful. Governments use CBDC to represent a digital version of their Fiat currencies.

CBDCs further divides into two categories: retail and wholesale. Retail CBDCs are for the general public and have everyday applications. Whereas wholesale CBDCs aim is to enable transactions and payments between financial organisations that store funds in central banks.

The main distinction is that most cryptocurrencies are built on open blockchain networks, allowing anybody to “mine” them.

CBDCs are safe too because they are based on private blockchains that are wholly owned by the central banks.

Central banks all around the world are debating whether or not to establish their own CBDC. While the potential benefits are great, there are several and as yet unsolved problems that must be overcome first.

The Bank of England (BOE) was the pioneer to initiate the CBDC proposal. Other nations, like China’s People’s Bank of China (PBoC) are looking to introduce a central bank-issued digital currency.

How & Why CBDC ?

Cryptocurrencies like Bitcoin, which use distributed ledger technology known as the blockchain network, have grown in popularity over the years. Because of their decentralized and regulation-free character, virtual currencies have exploded in popularity. Few even consider them as a danger to traditional banking such as a central bank. Furthermore, the constant introduction of new cryptocurrencies has prompted concerns about the risk of frauds, thefts, and hacks.

Central banks across the world are working on releasing their own versions of cryptocurrencies to limit the influence of such cryptocurrencies. These controlled cryptocurrencies are known as central bank digital currencies. Central banks of the countries manage them according to their regulations. Thus these CBDC’s won’t be volatile as cryptocurrencies.

Each CBDC unit will be distinctive, just like a paper-based currency note with a unique serial number, to avoid counterfeiting.

CBDC strives to combine the best of both worlds. The ease and security of digital forms like cryptocurrencies, as well as the traditional banking system’s regulated, reserve-backed money circulation. It will work with other regulated money, like coins, because it will be part of the central bank’s fund.

Characteristics of CBDC

Let us take a look at the Characteristics Of CBDC.

- CBDCs are still in their early stages, so it’s unclear what features they’ll have if they’re ever implemented.

- A CBDC resembles a cross between Bitcoin and a government-issued currency in many ways.

- Distributed Ledger Technology (DLT) is an important feature of CBDC. DLT refers to the technological infrastructure and protocols which allow simultaneous access, validation, and record updating across a network.

- Using encryption, DLT provides for the secure and accurate storage of any information. Instead of a single central database of financial information, DLT is made up of several copies of transaction history. Each copy is held and administered by a distinct financial body, with the country’s central bank.

- CBDC is also an example of a permissioned blockchain. A permissioned blockchain is a blockchain where only a selected few entities can access and/or alter the blockchain.

Benefits of CBDC

- Advocates claim the way CBDCs are structured under the hood could lead to lower costs for transferring money.

- Tracking of payments is also a benefit. China is known for its extensive intelligence, potentially wanting to use this financial information to keep tighter tabs on citizens.

- With CBDCs, payments and transfers will be easier to identify and trace the sources and reduce fraud and money laundering.

- Central banks issues the CBDCs, and hence may access and transfer funds without private bank accounts.

Risks of CBDC

- Launching a CBDC would transfer substantial technology risks to the public sector and ultimately taxpayers.

- CBDC would necessitate centralization, which would amplify already rife cyber vulnerabilities and increase the surface area and vectors of attack.

- If, CBDC issued at retail level or by a non-government agency, would potentially increase encroachment on consumer privacy and protections.

- CBDC creates a “flight to quality” problem, which would destabilize the two-tiered banking systems protected by the central banks.

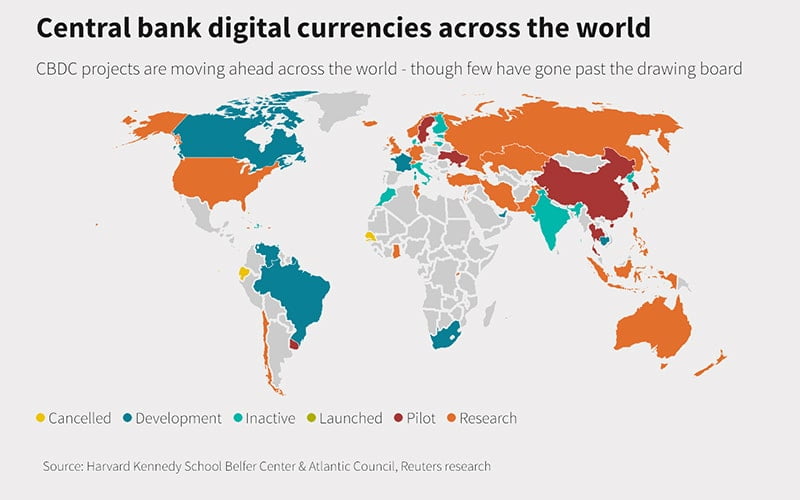

Many Countries Globally are Choosing CBDC

With the growing interest in blockchain technology and cryptocurrencies, many countries around the world have started CBDC projects. However, some countries have progressed a lot more than others.

The interest of countries looking to launch their own CBDCs has doubled during the pandemic year. Only 35 countries were considering having their own CBDC in May 2020. Now 81 counties are considering whether or not to take part, according to the Atlantic Council. These 81 counties represent over 90% of the world’s gross domestic product (GDP).

The road is still debatable for India. According to reports, India falls within the ‘research’ category since the country’s crypto bill is still pending. In January, the Reserve Bank of India proposed its own digital rupee in the Lok Sabha, even if the fate is still uncertain. “They are not money,” T. Rabi Sankar, the deputy governor of the RBI said.

When it comes to CBDCs, China is ahead of the rest of the globe. The Digital yuan of China is currently undergoing various tests around the country for a variety of applications, including medical insurance. In addition to China, 14 other nations, including South Korea and Sweden, are conducting CBDC pilot projects.

Meanwhile, just five countries: the Bahamas, Antigua and Barbuda, Saint Lucia, and two Caribbean nations, have fully implemented a CBDC.

For now, the United States only started to consider the notion seriously in May of this year. The Federal Reserve has indicated that they will release a study paper this summer for the viability of a CBDC.

Conclusion:

Over the last few years, countries have continued to express their ambitions to establish their own digital assets.

Although 86% of central banks globally are considering creating a CBDC, the research is still in the early stages. The major argument is how to allow a growing private sector to thrive in the future of payments and money.

CBDCs that have been fully developed will soon be available in countries all over the world. We have yet to see how each country will make use of the digital landscape, which offers various advantages. On the opposite end, there are concerns about privacy and democracy, which may or may not become a reality.